BMRI: Wholesale business supports loan growth resilience

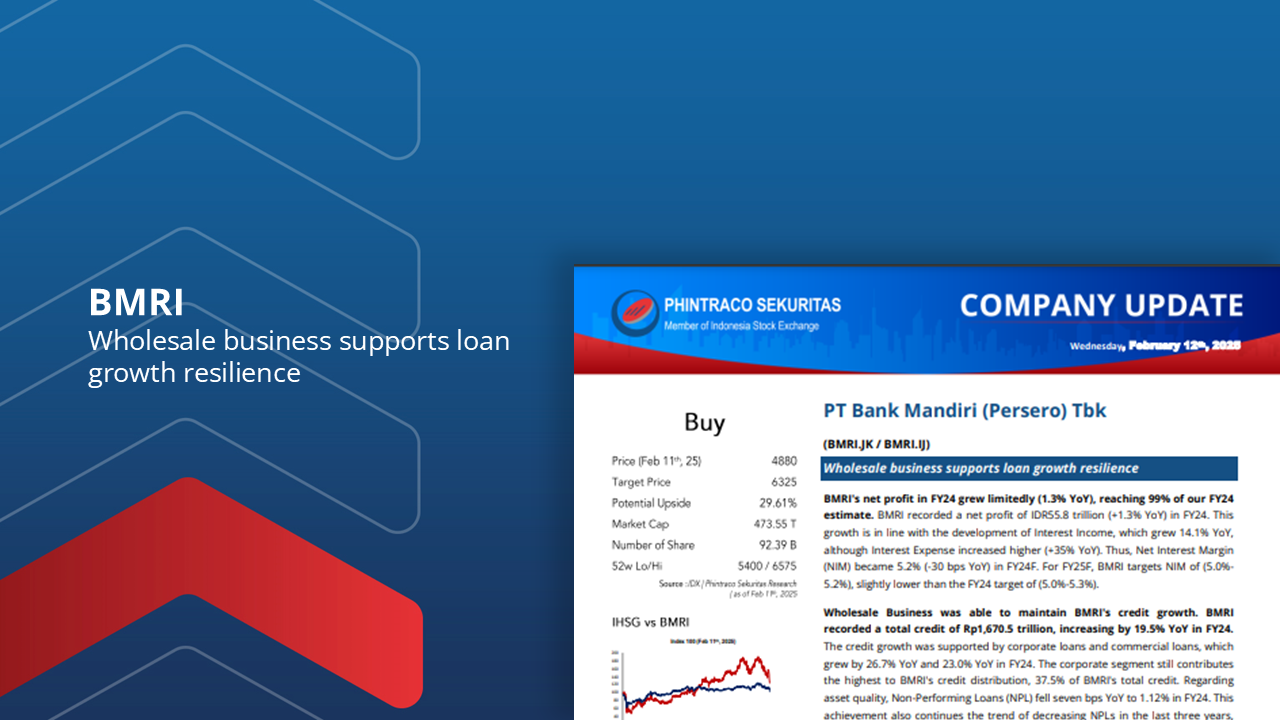

BMRI‘s net profit in FY24 grew limitedly (1.3% YoY), reaching 99% of our FY24 estimate. This growth is in line with the development of Interest Income, which grew 14.1% YoY, although Interest Expense increased higher (+35% YoY).

Wholesale Business was able to maintain BMRI‘s credit growth. BMRI recorded a total credit of Rp1,670.5 trillion, increasing by 19.5% YoY in FY24.

The current Account savings account (CASA) ratio grew 52 bps YoY in FY24. BMRI recorded a CASA of IDR1,271 trillion (+8.49% YoY) in FY24, with a CASA ratio recorded at 74.8% (+52 bps) YoY.

We estimate interest income can grow 7% YoY in FY25F.Another income optimization comes from fee-basedincome, one of which comes from the adaptation of Livin’.

Using the Discounted Cash Flow method with a Required Return of 7.87% and Terminal Growth of 3.39%, we estimate BMRI‘s fair value at 6,325 (9.76x expected P/E). Therefore, we still maintain a buy rating for BMRI with a lower fair value and a potential upside of 29.61%.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –