Phintraco Sekuritas Company Flash Notes

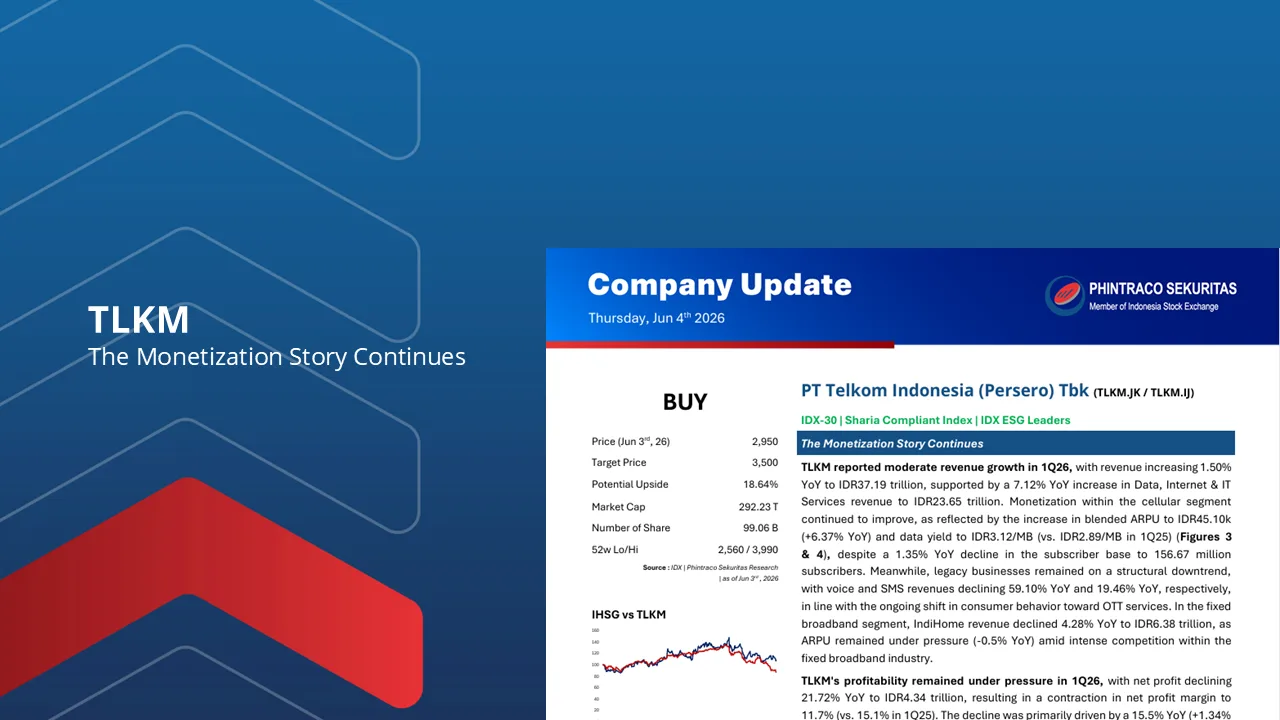

PT Telkom Indonesia Tbk – TLKM.IJ

Aditya Prayoga

>TLKM delivered a relatively resilient 1Q26 performance, with revenue reaching Rp37.19 trillion (+1.50% YoY; +0.17% QoQ), supported by continued strength in the Data, Internet & IT Services segment as the primary growth driver. Revenue from the segment grew 7.12% YoY to Rp23.65 trillion, partially offsetting the ongoing decline in legacy services.

>On the operational side, subscriber trends remained relatively soft, with the mobile subscriber base declining 1.35% YoY to 156.67 million. However, this was more than offset by continued improvement in monetization quality, reflected in blended ARPU of Rp45.10K (+6.37% YoY) and data yield of Rp3.12/MB (vs. Rp2.89/MB in 1Q25). Data traffic also continued to expand (+2.3% YoY), suggesting that revenue growth is increasingly being driven by customer value rather than subscriber additions.

>Meanwhile, legacy services remained under pressure, with voice and SMS revenues declining 59.10% YoY and 19.46% YoY, respectively, in line with the ongoing migration toward OTT platforms. Within the fixed broadband segment, IndiHome revenue declined 4.28% YoY to Rp6.38 trillion amid continued ARPU pressure and intensifying competition across the broadband industry.

>From a profitability perspective, TLKM recorded net profit of Rp4.34 trillion (-21.72% YoY), below our expectations and consensus, with net profit margin contracting to 11.7% (vs. 15.1% in 1Q25). The decline was primarily attributable to higher O&M expenses (+15.5% YoY), driven by increased gaming voucher purchases and higher CPE-related costs, alongside a 3.8% YoY increase in depreciation and amortization expenses following revisions to the estimated useful lives of several network and infrastructure assets.

>Looking ahead, management maintains its FY26 revenue growth guidance of 1–3% YoY. We believe TLKM remains well-positioned to achieve its target, supported by an increasingly rational industry structure, improving customer monetization, and a stronger focus on customer quality. In addition, the ongoing streamlining agenda, with four non-core businesses already divested and a target of 9–10 divestments by 1H26, is expected to enhance management focus on core operations. The planned implementation of ERP Phase 2 in 2H26, with a budget of approximately Rp1.0–1.2 trillion, should further support operational transformation and business simplification efforts.

>Key risks to our view include: (1) weaker consumer purchasing power, (2) a more aggressive competitive environment, (3) higher-than-expected operating cost pressures, and (4) slower-than-expected execution of streamlining initiatives.

Full Report :

By PHINTRACO SEKURITAS | Research

– Disclaimer On –

Contact Us:

WA: 08119560188

IG: phintracosekuritasofficial

YT: Phintraco Sekuritas Official

TELE: phintasprofits

www.phintracosekuritas.com

www.profits.co.id