Plantations : CPO Stays Firm on Supply Tightness

>Global CPO supply is expected to remain broadly flat in FY26F, as Indonesia and Malaysia continue to face structural constraints from aging plantations. Smallholder replanting progress remains slow despite government...

Baca Laporan

Retailers: Online Sales Increase Amid Strong Expansion

Consumer confidence trend weakened in the past year. As of September 2025, the CCI was recorded at level 115.0, a decrease from level 117.2 in August 2025, and became the...

Baca Laporan

F&B and Poultry: Government Stimulus Potentially Maintains People’s Purchasing Power

Consumer confidence trend weakened in the past year. As of September 2025, the CCI was recorded at level 115.0, a decrease from level 117.2 in August 2025, and became the...

Baca Laporan

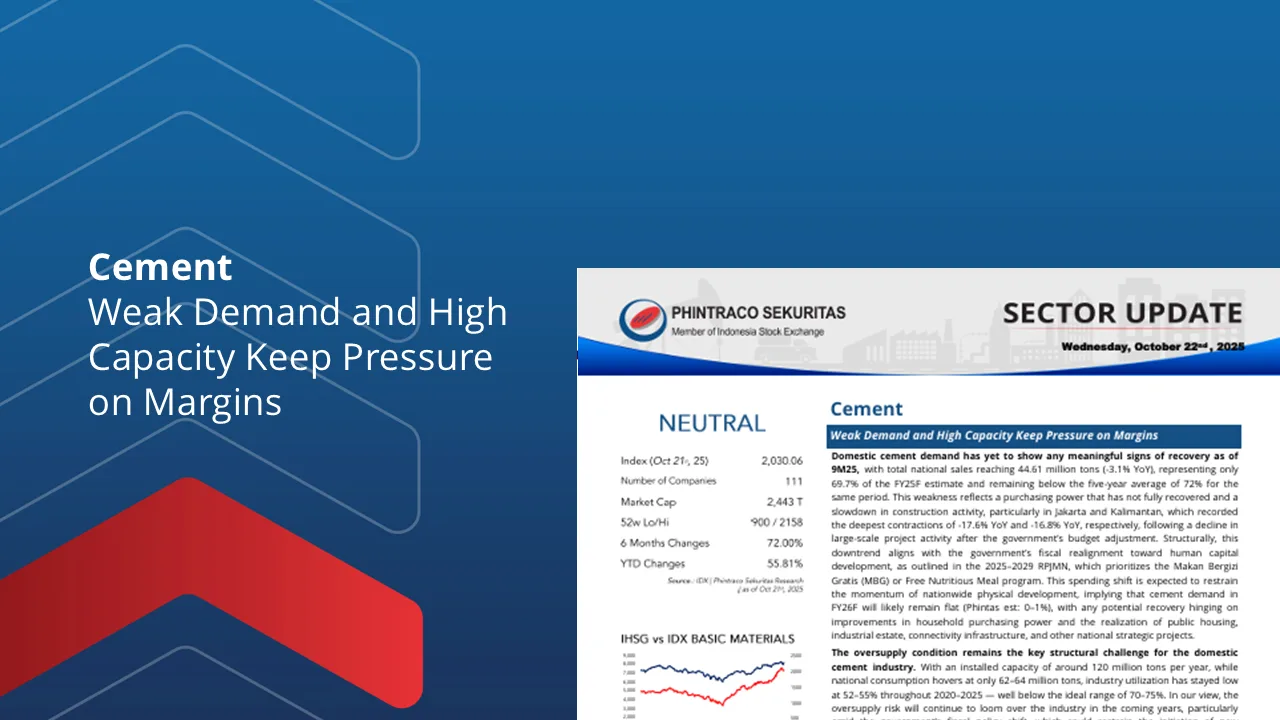

Cement: Weak Demand and High Capacity Keep Pressure on Margins

>Domestic cement demand remains sluggish as of 9M25, with total sales of 44.61 mn tons (-3.1% YoY), reflecting only 69.7% of FY25F estimates — below the five-year average of 72%....

Baca Laporan

Pharmaceuticals: Towards National Health Independence and Resilience

Gross Domestic Product (GDP) of the chemical, pharmaceutical, and traditional medicine industries continues positive trend in 2Q25. This condition showed that this industry still has quite a stable growth potential...

Baca Laporan

Properties & Real Estate: Property Sales Growth Potential in 2H25

BI rate has potential to be lowered again in the remainder of 2025. Bank Indonesia cut BI rate by 25 bps to 4.75%, there is still room for BI rate...

Baca Laporan

Banks: Accelerate through Incentives and Monetary Easing

The increase in deposits and CASA funds drove improvements in banking liquidity in 6M25. The Indonesian banking sector's Loan to Deposit Ratio (LDR) was booked at 86.40% (-176 bps MoM;...

Baca Laporan

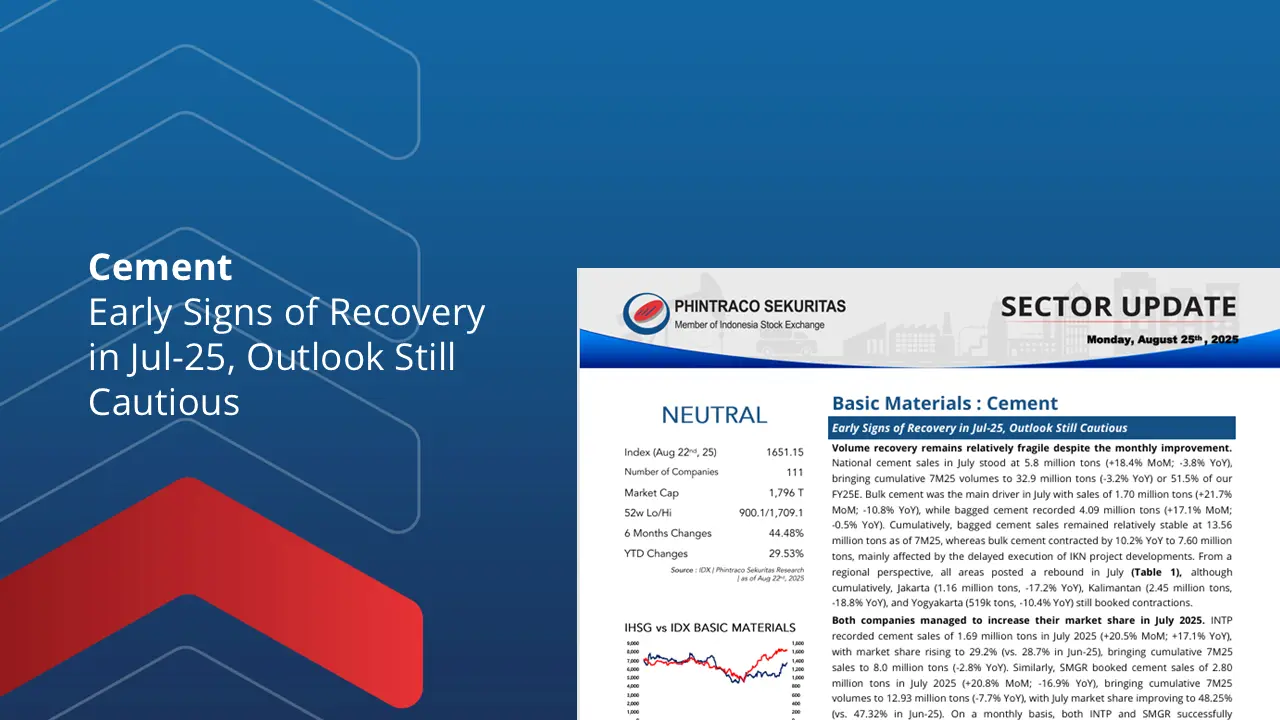

Cement : Early Signs of Recovery in Jul-25, Outlook Still Cautious

Volume recovery remains relatively fragile despite the monthly improvement. National cement sales in Jul-25 stood at 5.8 million tons (+18.4% MoM; -3.8% YoY), bringing cumulative 7M25 volumes to 32.9 million...

Baca Laporan

Plantations : CPO Outlook Brightens Amid Structural Strength

Both plantation names under our coverage delivered solid performance in 1Q25, with AALI posted robust revenue growth of 46.3% YoY, supported by higher sales volumes of CPO and palm kernel...

Baca Laporan