Phintraco Sekuritas Company Update

PT Sumber Tani Agung Resources Tbk – STAA.IJ

Aditya Prayoga

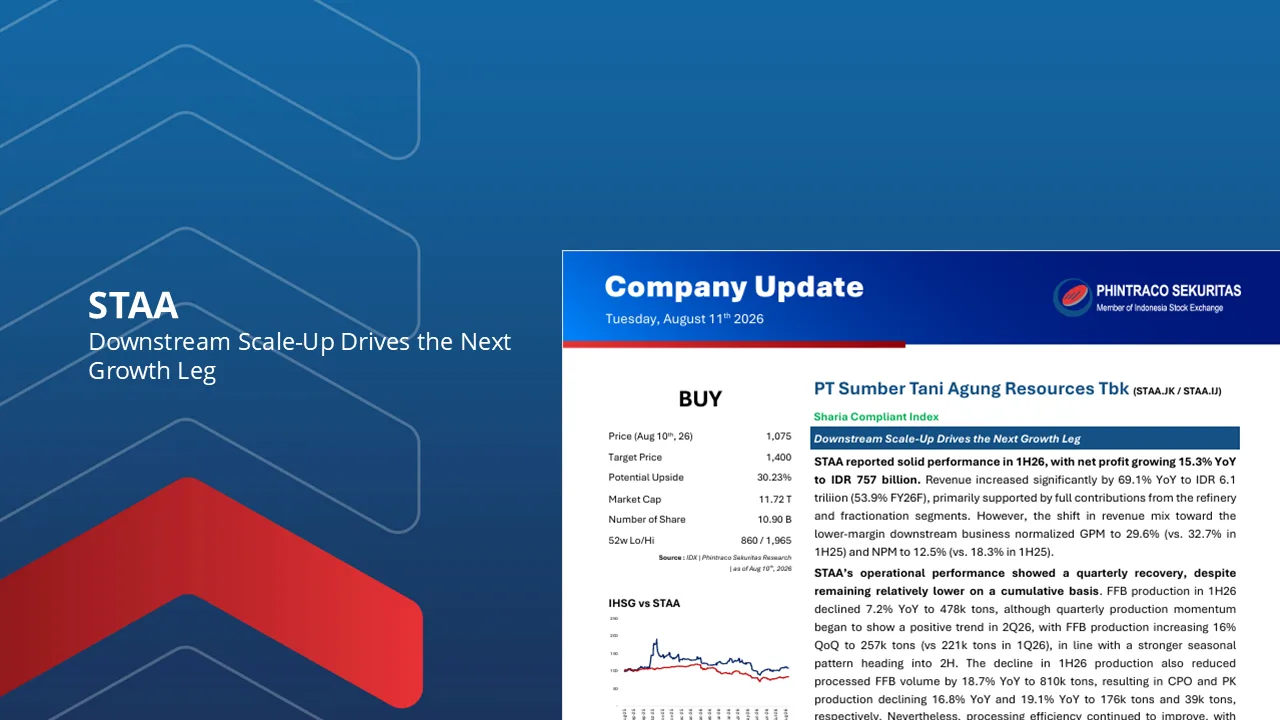

>STAA reported solid performance in 1H26, with net profit increasing 15.3% YoY to IDR 757bn. Revenue surged 69.1% YoY to IDR 6.1tr, reaching 53.9% of our FY26F estimate, primarily driven by full contributions from the refinery and fractionation segments. However, the revenue mix shift toward the lower-margin downstream business normalized GPM to 29.6% (vs 32.7% in 1H25) and NPM to 12.5% (vs 18.3% in 1H25).

>STAA’s operational performance showed a sequential recovery, despite remaining weaker on a cumulative basis. FFB production declined 7.2% YoY to 478k tons in 1H26. Nevertheless, production momentum improved in 2Q26, with FFB output increasing 16.0% QoQ to 257k tons (vs 221k tons in 1Q26), consistent with stronger seasonality heading into 2H.

>Lower FFB production reduced processed FFB volume by 18.7% YoY to 810k tons, resulting in CPO and PK production declining 16.8% and 19.1% YoY to 176k tons and 39k tons, respectively. Nevertheless, processing efficiency improved, with OER rising to 21.8% (vs 21.3% in 1H25). Meanwhile, the refinery ramp-up remained on track, with downstream product sales volume reaching 214k tons.

>We expect STAA’s growth momentum to continue in FY26F, supported by higher production and an increasing downstream contribution. We forecast production growth of 9.8% YoY, supported by its relatively young plantation profile with an average age of c.14 years and an improvement in FFB yield to 24.5 tons/ha (vs. 24.2 tons/ha in FY25).

>Higher upstream volume and increasing refinery and fractionation utilization should drive FY26F revenue growth of 74.8% YoY to IDR 11.25tr. However, the revenue mix shift toward downstream products is expected to normalize GPM to 27.3% (vs 32.7% in FY25). Despite this margin pressure, higher volume and operating scale should lift net profit to IDR 1.5 Trillion, with NPM normalizing to 13.6% (vs 16.6% in FY25).

>Key downside risks include: (1) CPO price volatility, (2) regulatory changes, and (3) higher input costs.

By PHINTRACO SEKURITAS | Research

— Disclaimer On —

Contact Us:

WA: 08119560188

IG: phintracosekuritasofficial

YT: Phintraco Sekuritas Official

TELE: phintasprofits

www.phintracosekuritas.com

www.profits.co.id