PTBA: Volume Resilience Supported by Strategic Logistic Expansion

PTBA new railway project, The Tanjung Enim–Keramasan railway (20 Mtpa, 158 km), targeted for operation in 2Q26, alongside port capacity upgrades, is expected to materially improve logistics efficiency and reduce...

Baca Laporan

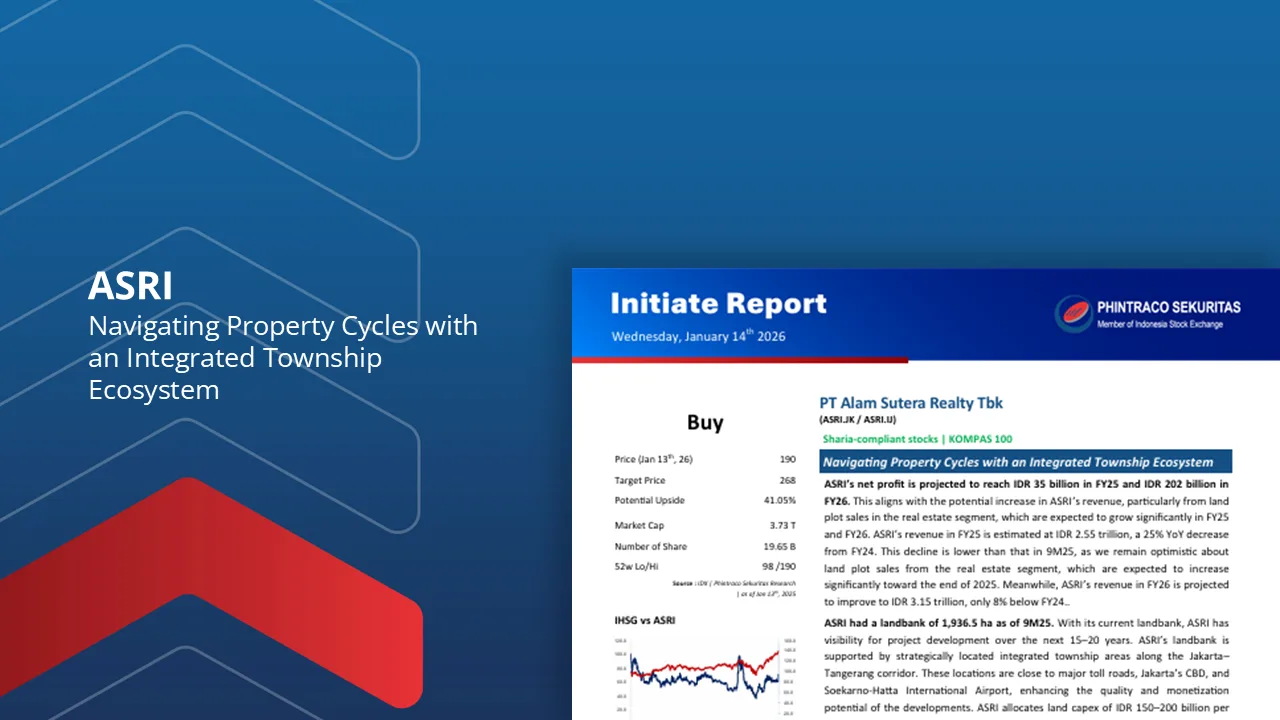

ASRI: Navigating Property Cycles with an Integrated Township Ecosystem

ASRI’s net profit is projected to reach IDR 35 billion in FY25 and IDR 202 billion in FY26. This aligns with the potential increase in ASRI’s revenue, particularly from land...

Baca Laporan

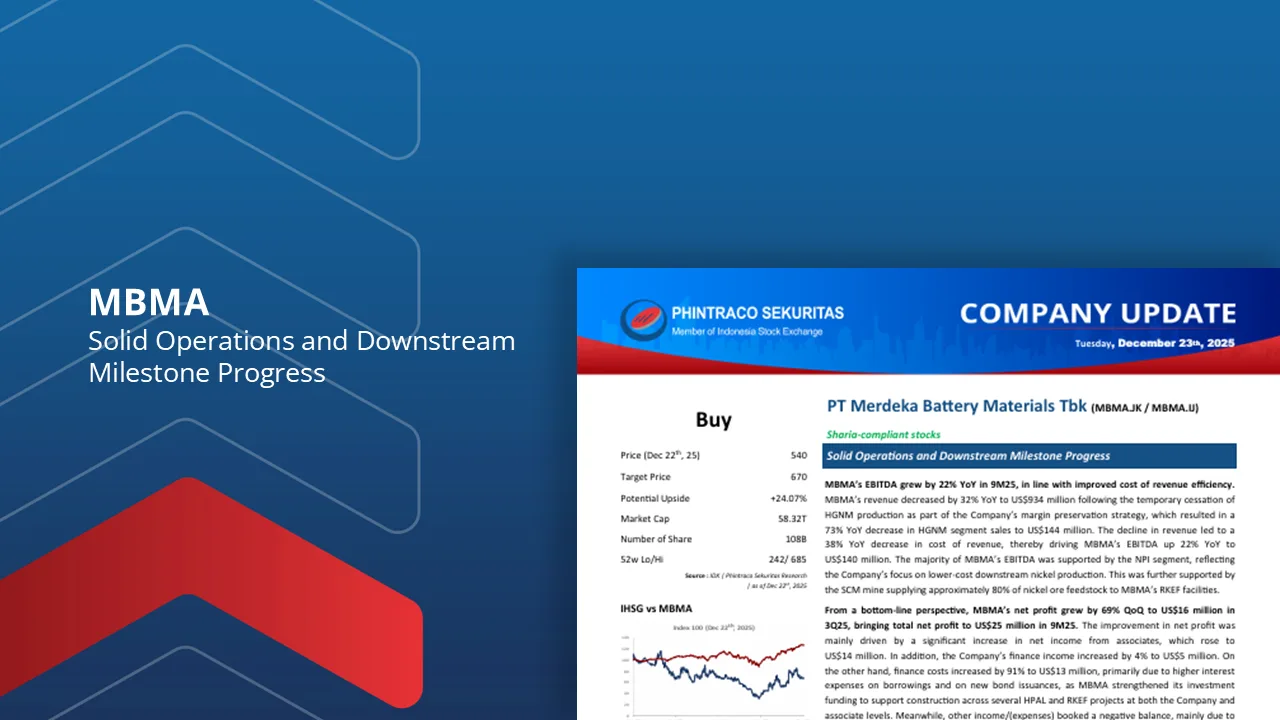

MBMA: Solid Operations and Downstream Milestone Progress

MBMA’s EBITDA grew by 22% YoY in 9M25, in line with improved cost of revenue efficiency. The majority of MBMA’s EBITDA was supported by the NPI segment, reflecting the Company’s...

Baca Laporan

MDKA: Unlocking Value by Optimizing Business Transition and Cost Efficiency

MDKA's revenue declined amidst the transition and optimization of its nickel business. MDKA's revenue decrease 23% YoY to US$1.29 billion in 9M25 from US$1.67 billion in 9M24. MDKA's EBITDA Increase...

Baca Laporan

SMRA : Earnings Under Pressure, Marketing Sales Support SMRA’s Outlook

SMRA’s net profit declined by 41% YoY to Rp549.6 billion in 9M25. This decline was mainly driven by a 15% YoY decrease in revenue to Rp6.41 trillion in 9M25. On...

Baca Laporan

ADRO: Performance Normalization Amid Business Transition Phase

ADRO is undergoing a post-divestment transition marked by weaker financial performance due to lower global coal prices, although higher coal sales volumes and relatively stable margins indicate that profitability pressure...

Baca Laporan

AADI: Remains Resilient Despite Weakening Coal Exports

AADI’s revenue in 9M25 was in line with our expectations. The company recorded revenue of US$1.21 billion in 3Q25 (-2.1% QoQ; -13.2% YoY), resulting in a 10.9% YoY decline in...

Baca Laporan

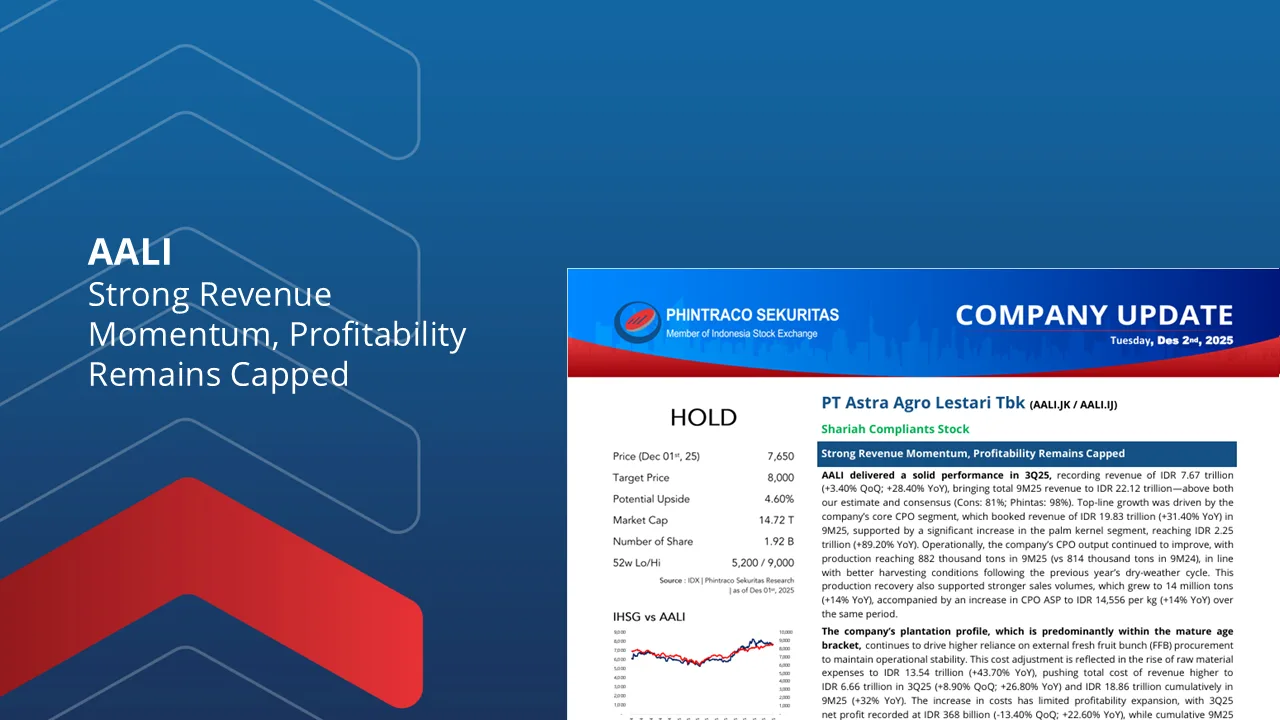

AALI : Strong Revenue Momentum, Profitability Remains Capped

AALI posted a solid 3Q25 performance with revenue of IDR 7.67tn (+3.4% QoQ; +28.4% YoY), bringing 9M25 revenue to IDR 22.12tn, above both our estimate and consensus. Growth was supported...

Baca Laporan

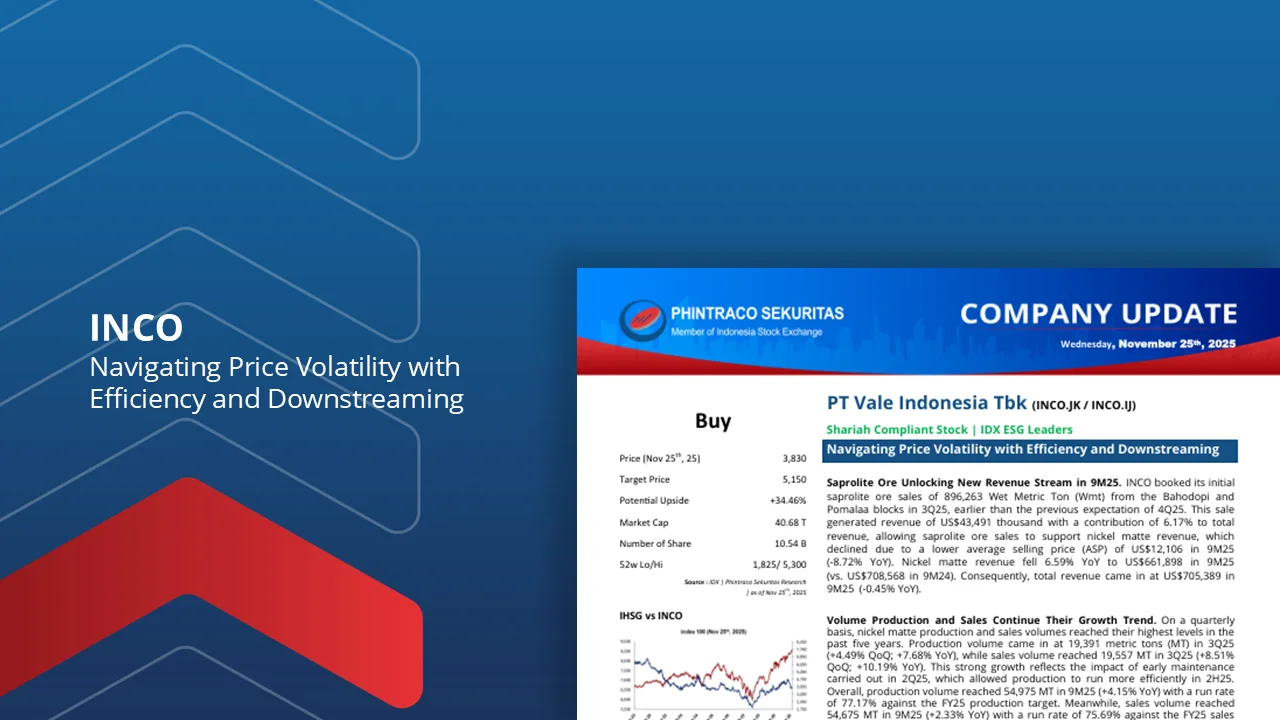

INCO: Navigating Price Volatility with Efficiency and Downstreaming

Saprolite Ore Unlocking New Revenue Stream in 9M25. INCO booked its initial saprolite ore sales of 896,263 Wet Metric Ton (Wmt) from the Bahodopi and Pomalaa blocks in 3Q25, earlier...

Baca Laporan