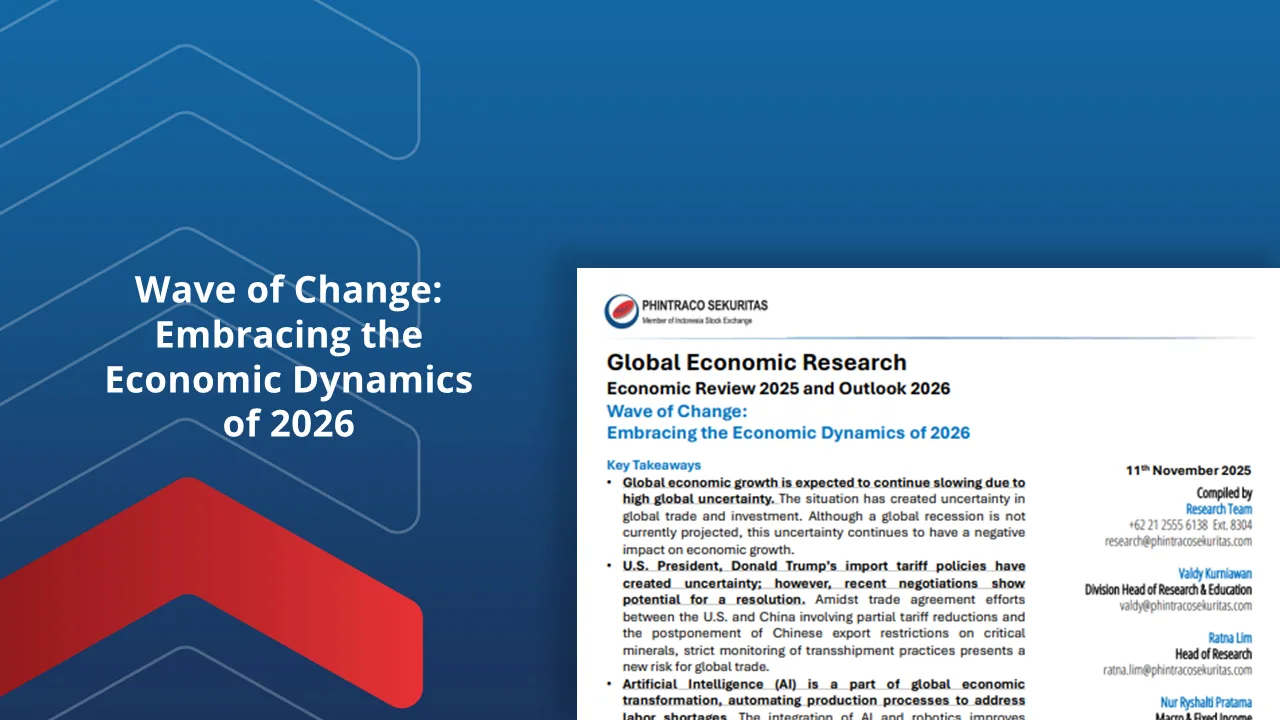

Global Economic Research : Embracing the Economic Dynamics of 2026

Global economic growth is expected to keep slowing amid high global uncertainty. This situation continues to weigh on trade, investment, and overall economic performance. U.S. President Donald Trump’s import tariff...

Baca Laporan

Indonesia Economic Research: Embracing the Economic Dynamics of 2026

Indonesia's economy is projected to grow 5.0%-5.2% YoY in 2026. Indonesia's economic growth is expected to accelerate in 2026, in line with expectations of improving global conditions and increased domestic...

Baca Laporan

Navigating the Potential Shifting of the Global Economic Landscape

At the start of Donald Trump’s second presidency, trade wars re-emerged as a key global issue. President Trump's reciprocal tariff policy took effect on February 1, 2025, introducing a 25%...

Baca Laporan

Domestic Economic Research : Economic Stability and Growth Opportunities 2025

PHINTRACO SEKURITAS (AT) -13 November 2024- Indonesia's economy has shown a solid recovery, with GDP growth observed across spending sectors. This reflects resilience and a balanced approach to economic recovery....

Baca Laporan

Global Economic Research: Cruising The Election and Gepolitical Waves

The majority of countries started to show an increase in economic growth in 2Q24, after experiencing a slowdown at the beginning of the year. Global monetary policy was less-aggressive than...

Baca Laporan

2024 Economic & Market Outlook: Searching for Opportunities in a Political Year

**REVIEW : Global Economic & Capital Market in 2023** >The acceleration of economic activity recovery cannot be matched by an increase in supply. >Russia-Ukraine war worsening supply chain disruption, especially...

Baca Laporan

2023 Economic & Market Outlook : Risiko Resesi Ekonomi Meningkat ditengah Kenaikan Harga dan Agresifitas Sejumlah Bank Sentral

REVIEW : Ekonomi dan Pasar Modal Global 2022 >Pandemi COVID-19 relatif terkendali secara global, terutama di 2H-2022. >Akselerasi pemulihan aktivitas ekonomi tidak dapat diimbangi oleh peningkatan supply. >Perang Rusia-Ukraina memperparah...

Baca Laporan