Daily Research

Read More

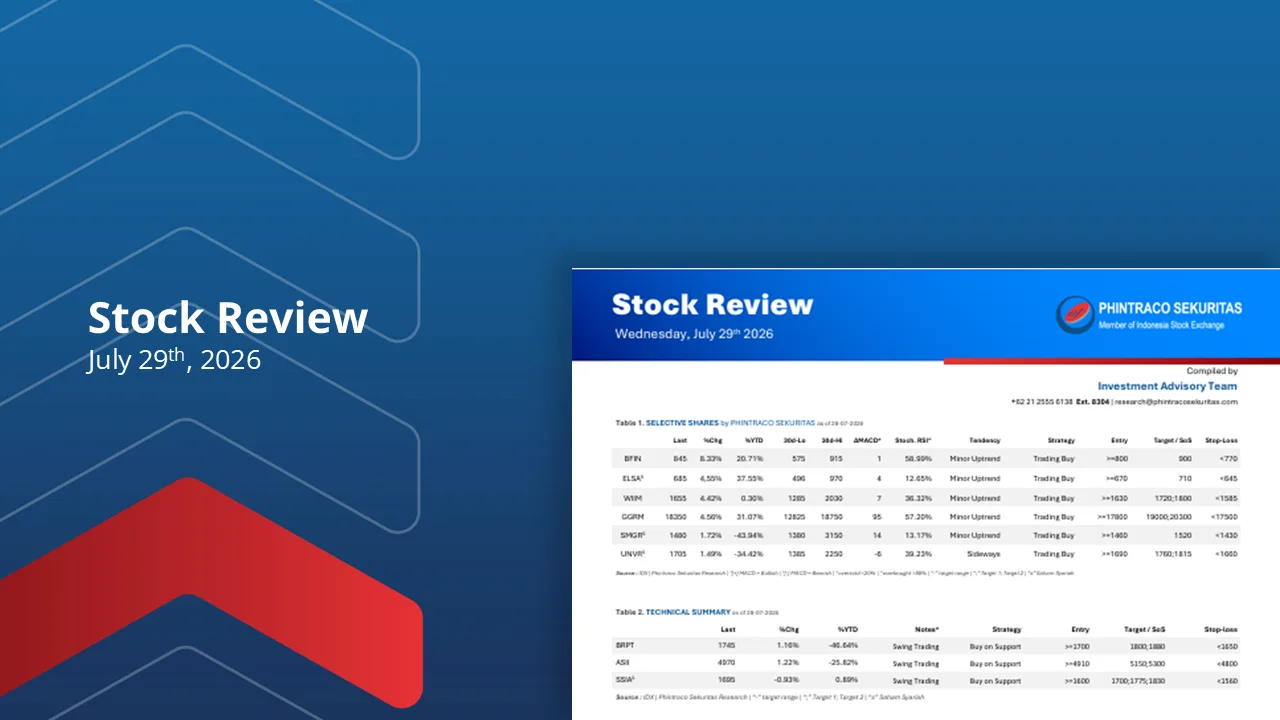

Investor menantikan hasil FOMC meeting

Indeks di Wall Street ditutup mixed pada Selasa (28/7).

Berlanjutnya koreksi harga minyak, kinerja keuangan yang solid, serta rotasi sektor mendorong penguatan indeks Dow Jones.

Saham semikonduktor yang berlanjut koreksi memicu pelemahan Nasdaq Composite.

Wall Street menantikan laporan keuangan saham teknologi dan FOMC meeting (29/7).

The Fed diperkirakan mempertahankan suku bunga acuan pada level 3.5%-3.75% (29/7).

Harga minyak berlanjut melemah sekitar 4% (28/7).

U.S. 10-year Bond Yield turun 4 bps ke level 4.602% (28/7).

Harga emas spot koreksi 1.1% di level US$4,032/troy oz (28/7).

Diperkirakan IHSG akan menguji level 6050-6100 pada perdagangan Rabu (29/7).

Top picks (29/7): UNVR, BFIN, GGRM, ELSA dan WIIM.

By PHINTRACO SEKURITAS | Research

- Disclaimer On -

Baca Laporan

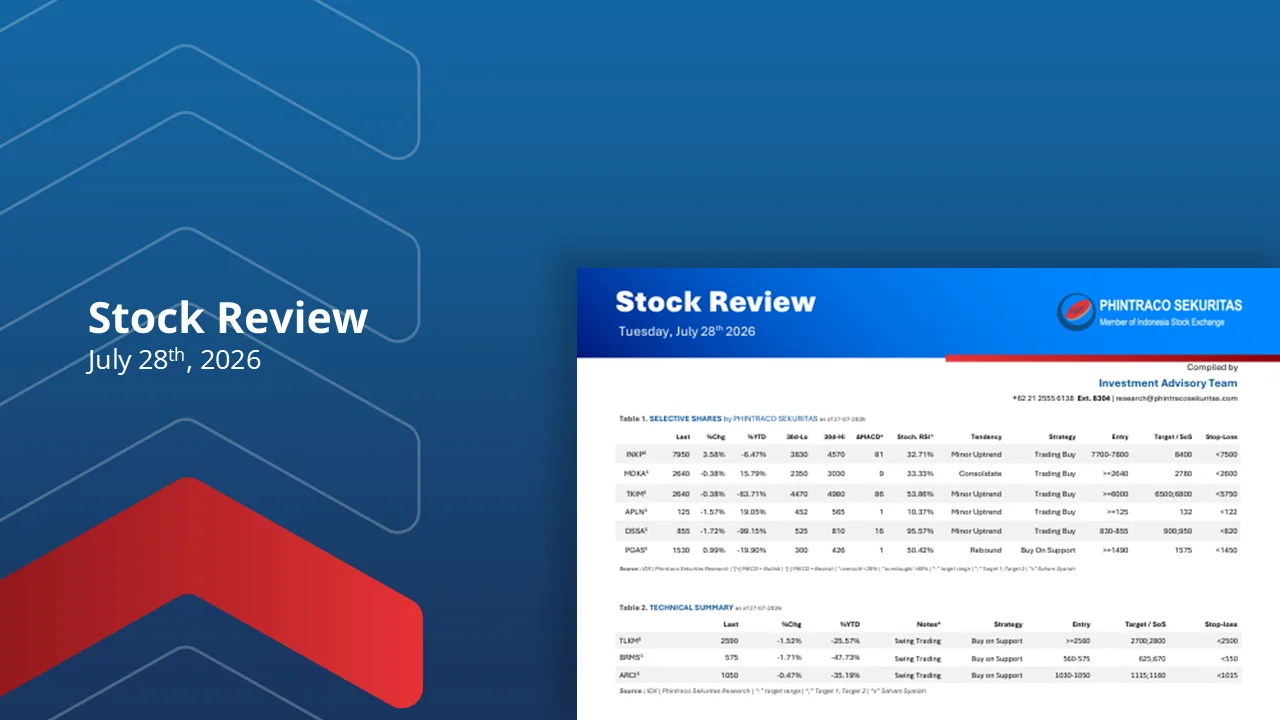

Diperkirakan IHSG akan cenderung berkonsolidasi

Indeks di Wall Street ditutup mixed pada Senin (27/7).

Koreksi harga minyak menjadi faktor positif.

Pelemahan pada saham semikonduktor menjadi katalis negatif.

BEI merombak konstituen indeks LQ45, IDX30, IDX80 dan Kompas 100 yang mulai berlaku pada 3 Agustus-30 Oktober 2026.

Investor menantikan pengganti Gubernur BI yang definitif.

Harga minyak Brent dan WTI masing-masing ditutup melemah lebih dari 8% dan 7% (27/7).

U.S. 10-year Bond Yield turun 3 bps ke level 4.649% (27/7).

Harga emas spot menguat 0.9% di level US$4,087/troy oz (27/7).

Diperkirakan IHSG cenderung berkonsolidasi pada kisaran 6,080-6,250 (28/7).

Top picks (28/7): PGAS, INKP, TLKM, MDKA dan ASII.

By PHINTRACO SEKURITAS | Research

- Disclaimer On -

Baca Laporan

Berlanjutnya kenaikan harga minyak menjadi katalis negatif

Indeks di Wall Street ditutup melemah pada Kamis (23/7).

Pelemahan indeks dipicu oleh peningkatan harga minyak.

Kinerja Alphabet dan Tesla memicu kekhawatiran tentang peningkatan pengeluaran AI.

ECB mempertahankan suku bunga acuan tetap di 2.4% (23/7).

Jumlah uang beredar (M2) Indonesia meningkat 8.7% YoY pada Juni 2026 (23/7).

Harga minyak Brent menguat 7% mencapai level US$100/barel (23/7).

U.S. 10-year Bond Yield naik 6 bps ke level 4.699% (23/7).

Harga emas spot melemah 2.1% di level US$4,041/troy oz (23/7).

Diperkirakan IHSG uji level 6,200-6,280 (24/7).

Top picks (24/7): EMAS, MIKA, AALI, TAPG, AMRT.

By PHINTRACO SEKURITAS | Research

- Disclaimer On -

Baca Laporan

Technical Research

Read More

Weekly Research

Read More

Investor nantikan perkembangan konflik AS-Iran serta kebijakan moneter sejumlah bank sentral

Indeks di bursa Wall Street ditutup melemah pada Jumat (24/7).

Koreksi saham chip bebani indeks, harapan perundingan AS-Iran menjadi faktor positif.

Investor cermati perkembangan konflik di Timur Tengah lebih lanjut.

Pemerintahan Trump berlakukan tarif terhadap produk-produk lebih dari 80 negara.

The Fed diperkirakan pertahankan suku bunga di 3.5%-3.75% (29/7).

Bank of England diperkirakan pertahankan suku bunga acuan di 3.75% (30/7).

Diperkirakan Bank of Japan masih pertahankan suku bunga di level 1% (31/7).

Secara teknikal IHSG berpeluang uji level 6,000-6,100 pada pekan ini.

Top picks pekan ini: BBCA, TPIA, BULL, AKRA, TOWR dan BRIS.

By PHINTRACO SEKURITAS | Research

- Disclaimer On -

Baca Laporan

Investor menantikan hasil RDG Bank Indonesia di tengah kenaikan harga minyak dunia

Indeks di bursa Wall Street ditutup melemah pada Jumat (17/7) dan pekan lalu.

Koreksi disebabkan oleh pelemahan saham semikonduktor dan eskalasi geopolitik.

Pergerakan harga minyak akan menjadi perhatian pasar global.

Di Wall Street akan dirilis sejumlah laporan keuangan perusahaan teknologi pekan ini.

ECB diperkirakan mempertahankan suku bunga acuan tetap di 2.4% (23/7).

Investor akan menantikan RDG Bank Indonesia dan pertumbuhan kredit (22/7).

Sentimen domestik membaik namun perlu waspadai kenaikan harga minyak mentah.

Secara teknikal IHSG berpeluang uji level 6,225-6,280 pada pekan ini.

Top picks pekan ini: UNVR, KLBF, BBYB, ICBP, MDKA dan GTSI.

By PHINTRACO SEKURITAS | Research

- Disclaimer On -

Baca Laporan

Diperkirakan IHSG bergerak sideways pada kisaran 5800-6000 pada pekan ini

Indeks di bursa Wall Street ditutup menguat pada Jumat (10/6).

Penguatan terutama dikontribusikan oleh saham sektor teknologi.

Di Wall Street akan dimulai earning season 2Q26 pada pekan ini.

Data ekonomi AS yang akan dirilis diantaranya CPI dan Michigan Consumer Sentiment.

Investor juga menantikan testimoni Chairman the Fed di DPR AS dan Senat AS.

Pemerintah akan lelang SBSN dengan target indikatif Rp10 triliun (14/7).

BI akan rilis Statistik Utang Luar Negeri Mei 2026 (13/7).

Diperkirakan IHSG masih bergerak sideways pada kisaran 5800-6000 pada pekan ini.

Top picks pekan ini: ADRO, ADMR, BRMS, INCO, ARCI dan SRTG.

By PHINTRACO SEKURITAS | Research

- Disclaimer On -

Baca Laporan

Fixed Income Research

Read More

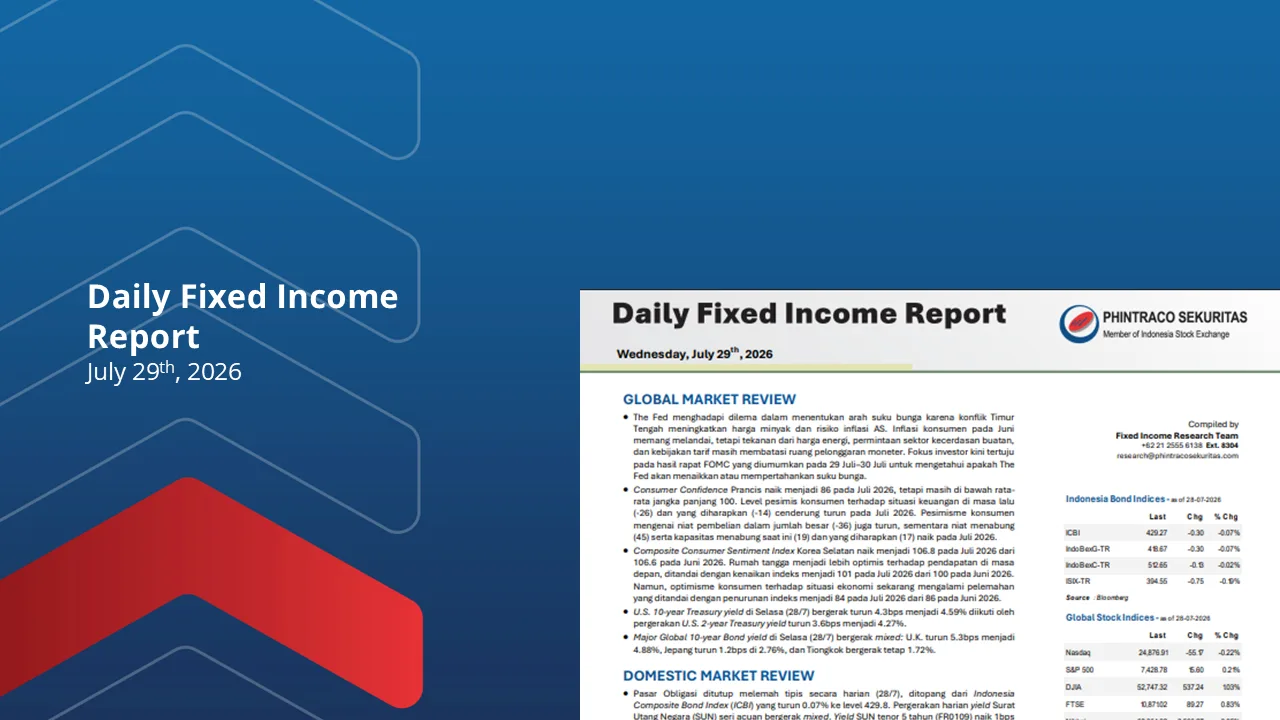

Daily Fixed Income Report – 29 July 2026

The Fed menghadapi dilema dalam menentukan arah suku bunga karena konflik Timur Tengah meningkatkan harga minyak dan risiko inflasi AS. Inflasi konsumen pada Juni memang melandai, tetapi tekanan dari harga energi, permintaan sektor kecerdasan buatan, dan kebijakan tarif masih membatasi ruang pelonggaran moneter. Fokus investor kini tertuju pada hasil rapat FOMC yang diumumkan pada 29 Juli–30 Juli untuk mengetahui apakah The Fed akan menaikkan atau mempertahankan suku bunga.

Pejabat Sementara (Pjs) Gubernur Bank Indonesia (BI), Destry Damayanti, menyatakan bahwa BI akan tetap menjaga stabilitas nilai tukar dengan berbagai kebijakan yang pro-growth seperti sebelumnya. BI akan terus berada di pasar, baik melalui intervensi di spot Domestic Non Deliverable Forward (DNF) maupun Non Deliverable Forward (NDF).

Baca Laporan

Daily Fixed Income Report – 28 July 2026

U.S. Durable Goods Orders meningkat 0.3% MoM menjadi US$334.77 miliar pada Juni 2026, setelah kontraksi 4.0% MoM pada Mei 2026. Kenaikan terutama terjadi pada barang modal sebesar 1.1% MoM, logam dasar 1.1% MoM, komputer dan elektronik 3.1% MoM karena didukung investasi pada AI dan kenaikan belanja pertahanan AS.

Gubernur Bank Indonesia (BI), Perry Warjiyo, mengundurkan diri dari posisinya pada Senin (27/7), yang kemudian posisinya digantikan sementara oleh pejabat Gubernur sementara, Destry Damayanti. Pengunduran diri tersebut memicu respons berupa kenaikan yield pada 14 seri tenor dari 20 seri tenor SUN. Selain itu, Credit Default Swap (CDS) tercatat naik, menunjukkan premi risiko yang lebih tinggi.

Baca Laporan

Weekly Fixed Income Report – 27 July 2026

Presiden AS Donald Trump, menetapkan tarif impor baru sebesar 10.0% hingga 12.5% terhadap sebagian besar mitra dagang AS sebagai bagian dari kebijakan perdagangan yang lebih proteksionis. Kebijakan tersebut diperkirakan meningkatkan biaya impor ke pasar AS, berpotensi memicu ketidakpastian perdagangan global.

Menteri Keuangan RI Purbaya Yudhi Sadewa, memproyeksikan pertumbuhan ekonomi Indonesia melambat menjadi sekitar 5.4% pada 2Q26 dari 5.61% pada 1Q26, seiring normalisasi aktivitas ekonomi setelah kenaikan dan percepatan belanja pada awal 2026. Meski demikian, pemerintah optimistis pertumbuhan akan kembali menguat pada 2H26. dengan dukungan daya beli masyarakat dan perbaikan iklim investasi dan dunia usaha.

Baca Laporan

Single Stock Future

Read More

IPO Summary

Read More

PT Rans Entertainmen Indonesia Tbk (RANS)

Code : RANS

Sector : Consumer Cyclicals

Sub-Sector : Entertainment & Movie Production

---------------------------------------------

PERKIRAAN JADWAL PENAWARAN UMUM PERDANA SAHAM

Perkiraan Tanggal Efektif :

30 Juni 2026

Perkiraan Masa Penawaran Umum :

2 Juli 2026 - 8 Juli 2026

Perkiraan Tanggal Penjatahan :

8 Juli 2026

Perkiraan Tanggal Distribusi Saham :

9 Juli 2026

Perkiraan Tanggal Pencatatan Saham di BEI :

10 Juli 2026

---------------------------------------------

STRUKTUR PENAWARAN UMUM PERDANA SAHAM

Sebanyak-banyaknya sebesar 2,525,000,000 (dua miliar lima ratus dua puluh lima juta) saham biasa atas nama, atau sebanyak-banyaknya sebesar 20.02% (dua puluh koma nol dua persen) dari modal ditempatkan dan disetor Perseroan setelah Penawaran Umum Perdana Saham dengan nilai nominal Rp10,- (sepuluh Rupiah) setiap saham.

Nilai Nominal :

Rp10 per lembar saham

Harga Penawaran :

Rp135 - Rp170 per lembar saham

Jumlah Penawaran Umum :

Sebanyak-banyaknya sebesar Rp429,250,000,000,- (empat ratus dua puluh sembilan miliar dua ratus lima puluh juta Rupiah).

Penjamin Pelaksana Emisi Efek:

PT Trimegah Sekuritas Indonesia

Penjamin Emisi :

Akan ditentukan kemudian

By PHINTRACO SEKURITAS | Research

- Disclaimer On -

Baca Laporan

PT Bach Multi Global Tbk (BACH)

Code : BACH

Sector : Industrials

Sub-Sector : Diversified Industrial Trading

---------------------------------------------

PERKIRAAN JADWAL PENAWARAN UMUM PERDANA SAHAM

Perkiraan Tanggal Efektif :

29 Juni 2026

Perkiraan Masa Penawaran Umum :

1 Juli 2026 - 3 Juli 2026

Perkiraan Tanggal Penjatahan :

3 Juli 2026

Perkiraan Tanggal Distribusi Saham :

6 Juli 2026

Perkiraan Tanggal Pencatatan Saham di BEI :

7 Juli 2026

---------------------------------------------

STRUKTUR PENAWARAN UMUM PERDANA SAHAM

Sebanyak-banyaknya 615,000,000 (enam ratus lima belas juta) saham biasa atas nama yang merupakan saham baru, dengan nilai nominal Rp50,- (lima puluh Rupiah) setiap saham yang mewakili sebanyak 15.06% (lima belas koma nol enam persen) dari modal yang telah ditempatkan dan disetor penuh setelah Penawaran Umum.

Nilai Nominal :

Rp50 per lembar saham

Harga Penawaran :

Rp400 - Rp500 per lembar saham

Jumlah Penawaran Umum :

Sebanyak-banyaknya sebesar Rp246,000,000,000,- (dua ratus empat puluh enam miliar rupiah) sampai dengan Rp307,500,000,000,-(tiga ratus tujuh miliar lima ratus juta rupiah).

Penjamin Pelaksana Emisi Efek:

PT Erdhika Elit Sekuritas

Penjamin Emisi :

Akan ditentukan kemudian

By PHINTRACO SEKURITAS | Research

- Disclaimer On -

Baca Laporan

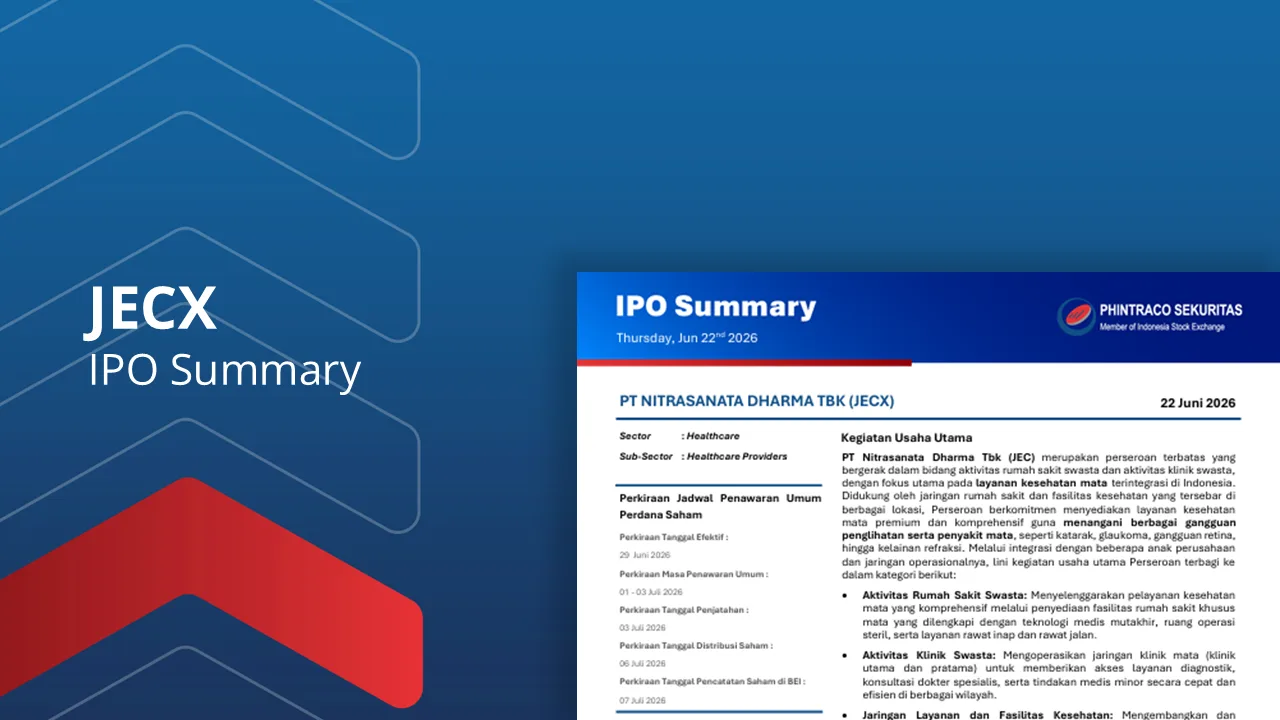

PT Nitrasanata Dharma Tbk (JECX)

Code : JECX

Sector : Healthcare

Sub-Sector : Healthcare Providers

---------------------------------------------

PERKIRAAN JADWAL PENAWARAN UMUM PERDANA SAHAM

Perkiraan Tanggal Efektif :

29 Juni 2026

Perkiraan Masa Penawaran Umum :

1 Juli 2026 - 3 Juli 2026

Perkiraan Tanggal Penjatahan :

3 Juli 2026

Perkiraan Tanggal Distribusi Saham :

6 Juli 2026

Perkiraan Tanggal Pencatatan Saham di BEI :

7 Juli 2026

---------------------------------------------

STRUKTUR PENAWARAN UMUM PERDANA SAHAM

Sebanyak-banyaknya 487,983,500 saham biasa, yang terdiri dari (i) 325,322,300 saham baru yang dikeluarkan dari portepel Perseroan yang mewakili 10.00% dan (ii) 162,661,200 saham milik DR.Dr. Waldensius Girsang, SpM(K) yang mewakili 5.00% dari modal ditempatkan dan disetor Perseroan setelah Penawaran Umum Perdana Saham yang mana seluruhnya sejumlah sebanyak-banyaknya 15% dari modal ditempatkan dan disetor Perseroan setelah Penawaran Umum Perdana Saham dengan nilai nominal Rp16,- (enam belas Rupiah) setiap saham.

Nilai Nominal :

Rp16 per lembar saham

Harga Penawaran :

Rp1,200 - Rp1,400 per lembar saham

Jumlah Penawaran Umum :

Sebanyak-banyaknya sebesar Rp683.176.900.000 (enam ratus delapan puluh tiga miliar seratus tujuh puluh enam juta sembilan ratus ribu Rupiah)

Penjamin Pelaksana Emisi Efek:

PT Trimegah Sekuritas

Penjamin Emisi :

Akan ditentukan kemudian

By PHINTRACO SEKURITAS | Research

- Disclaimer On -

Baca Laporan

Company Flash

Read More

ELSA: Strong Revenue Growth in the Distribution and Logistics Segment

ELSA reported solid 6M26 earnings, with revenue rising 8.9% YoY to Rp7.59 trillion and net profit increasing 29.2% YoY to Rp435 billion, supported by strong growth in the distribution and logistics segment despite weaker upstream service performance.

The distribution and logistics segment remained the key growth driver, contributing 64.8% of total revenue after expanding 26.6% YoY, offsetting declines in both integrated upstream oil & gas services and upstream support services.

Despite a 10.0% YoY increase in cost of revenue that compressed GPM by 89 bps to 9.51%, ELSA maintained stable operating profitability, while NPM improved to 5.73% through continued cost efficiency and disciplined expense management.

ELSA successfully implemented Indonesia’s first Chemical Enhanced Oil Recovery (CEOR) technology, strengthening its long-term growth prospects while supporting higher oil recovery and the government's 1 million barrels per day production target by 2030.

We maintain a positive outlook on ELSA, supported by resilient operational performance, higher global oil prices, the government's energy self-sufficiency agenda, accelerating domestic fuel demand, and ongoing expansion of upstream oil & gas activities.

By PHINTRACO SEKURITAS | Research

- Disclaimer On -

Baca Laporan

BTPS: Asset Quality Improves, Performance Recovery Continues

BTPS reported resilient 6M26 earnings, with net income rising 2% YoY to IDR655 billion, supported by a 34% YoY decline in provision expenses, despite Net Margin Income declining 2% YoY.

Total financing grew 9% YoY to IDR11.03 trillion, driven by 157% YoY growth in NBFI financing, while retail financing remained relatively stable and total financing increased 4% QoQ.

Funding quality improved, with CASA rising 27% YoY, reducing Margin Expense by 6% YoY, although pressure on financing yields continued to weigh on Financing Margin Income.

Asset quality continued to strengthen, as Net Financing Loss improved to 5.1%, NPF coverage increased to 334%, and CAR remained strong at 58.7%, providing ample room for future financing expansion.

We view the 6M26 results as broadly in line with our expectations, supported by improving financing growth, lower provisioning expenses, stronger asset quality, and a higher CASA mix, leading us to maintain our FY26 earnings forecast.

By PHINTRACO SEKURITAS | Research

- Disclaimer On -

Baca Laporan

BMRI: Profitability Sustained Despite Funding Cost Pressure

BMRI booked resilient 6M26 earnings, with net profit rising 24.4% YoY to IDR30.4 trillion, driven by 8.0% YoY NII growth, higher non-interest income (+14.9% YoY), lower operating expenses (-1.4% YoY), and a 12.5% YoY decline in provision expenses, despite continued NIM compression to 4.6%.

Loan growth remained robust at 18.8% YoY, well above management's 7–9% FY26 guidance, supported by 17.1% YoY TPF growth. However, the funding mix shifted toward higher cost time deposits, reducing the CASA ratio to 69.2%.

Asset quality continued to improve, with Gross NPL declining to 1.01% and Loan at Risk (LaR) decreasing to 5.83%. Liquidity and capital also remained solid, reflected by an LDR of 92.3% and CAR of 17.9%.

Management lowered FY26 NIM guidance to 4.3%–4.5% (from 4.5%–4.7%) due to persistent loan yield pressure, while maintaining loan growth guidance of 7–9% and cost of credit at 0.6–0.8%. Meanwhile, Livin' revenue increased 46.5% YoY to IDR2.03 trillion, supporting fee-based income growth.

We view the 6M26 results as broadly in line with our expectations, with net profit reaching 55% of our FY26 forecast. While margin pressure is likely to persist in 2H26, strong loan growth, healthy asset quality, and resilient fee-based income support our unchanged FY26 earnings outlook.

By PHINTRACO SEKURITAS | Research

- Disclaimer On -

Baca Laporan

Company Update

Read More

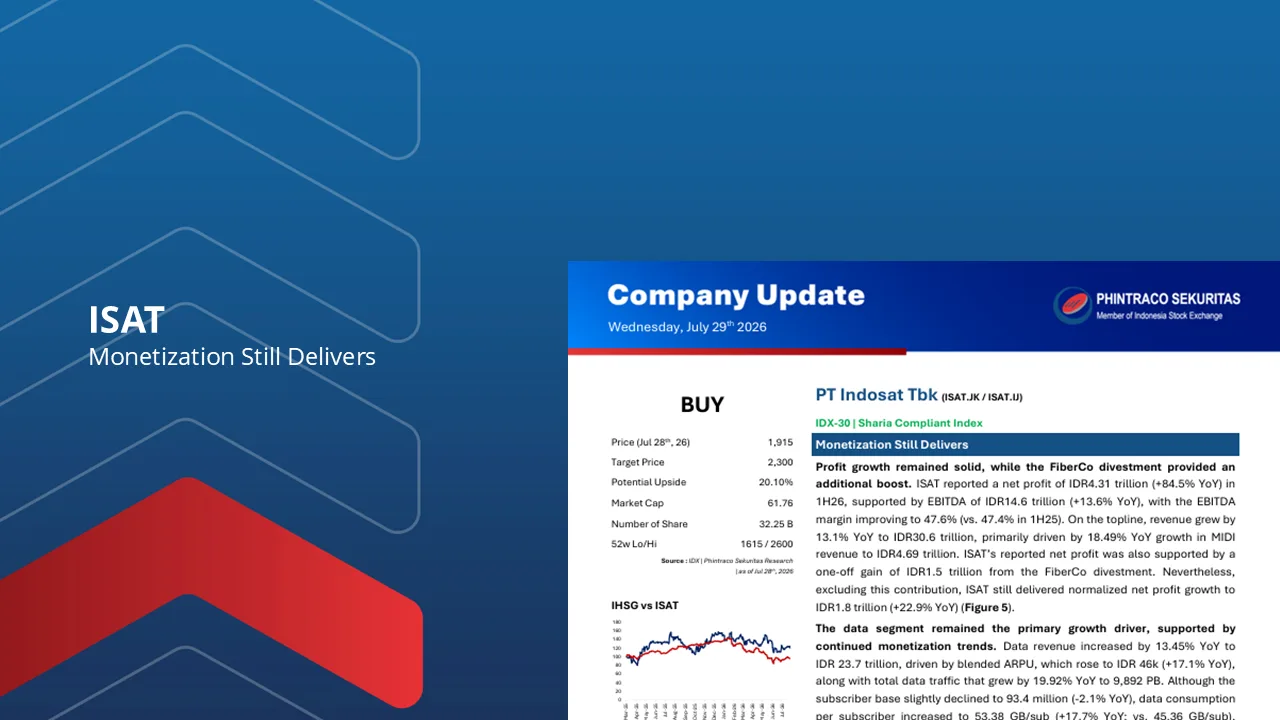

ISAT : Monetization Still Delivers

Phintraco Sekuritas Company Update

Aditya Prayoga

>ISAT reporting revenue of IDR30.6tn (+13.1% YoY) in 1H26, was primarily supported by the data business with data revenue increasing 13.45% YoY to IDR23.7tn, driven by stronger monetization as blended ARPU improved to IDR46K (+17.1% YoY) alongside data traffic growth of 19.9% YoY to 9,892PB. Although subscribers declined slightly to 93.4 million (-2.1% YoY), higher data consumption per user (53.4GB/sub; +17.7% YoY) reflected continued improvement in customer monetization quality.

>EBITDA reached IDR14.6tn (+13.6% YoY) with the EBITDA margin improving to 47.6% (vs. 47.4% in 1H25). Reported net profit surged to IDR4.31tn (+84.5% YoY), supported by a one-off gain of IDR1.5tn from the FiberCo divestment. Excluding this non-recurring gain, normalized net profit still increased 22.9% YoY to IDR1.8tn, highlighting resilient underlying operational performance despite higher financing costs. Meanwhile, legacy Voice and SMS revenues continued to decline by 28.5% YoY and 25.6% YoY, respectively, reflecting the ongoing migration toward OTT services.

>Solid execution in the data segment continues to underpin operational momentum, while higher interest expenses remain a key constraint on bottom-line growth. Following stronger-than-expected 1H26 results, management upgraded its FY26 guidance, now expecting close-to-double-digit revenue and EBITDA growth.

>Reflecting stronger ARPU realization and improving non-data contributions, we raise our FY26F/FY27F revenue forecasts by 1.6%/2.9% and EBITDA forecasts by 4.2%/6.3%, with EBITDA margins projected at 48.8%/49.4%. Nevertheless, we lower our FY26F/FY27F net profit forecasts by 12.6%/15.6%, incorporating expectations of persistently higher financing costs.

Downside risks include: (1) more aggressive industry competition leading to weaker ARPU and pricing pressure, (2) higher-than-expected financing costs amid a prolonged high interest rate environment, and (3) capex spending exceeding our estimates, potentially weighing on free cash flow and earnings growth.

By PHINTRACO SEKURITAS | Research

— Disclaimer On —

Contact Us:

WA: 08119560188

IG: phintracosekuritasofficial

YT: Phintraco Sekuritas Official

TELE: phintasprofits

www.phintracosekuritas.com

www.profits.co.id

Baca Laporan

INKP : Sustainable Revenue Through Demand and Capacity Growth

China's pulp demand remains resilient, with 2M26 import volumes reaching 2.47 million metric tons, or 14.4% above the 10-year average. Despite ongoing digitalization, demand continues to shift toward downstream products, supported by projected FY24–FY28F CAGR of 5.0% for tissue, 3.6% for packaging paper, and 2.7% for pulp, while printing paper demand is expected to decline.

INKP's production capacity expansion is expected to become a key catalyst in FY26F. The addition of 2.4 million metric tons of downstream capacity increases total capacity to 9.4 million metric tons, supporting a 20.7% YoY increase in total sales volume to 6.5 million metric tons and accelerating downstream production growth.

The company's sales mix is expected to shift further toward downstream products, with downstream contribution projected to increase to 48% of total sales volume in FY26F (vs 37% in FY25), reducing reliance on the cultural paper segment and strengthening exposure to higher-growth packaging-related products.

Industrial paper is expected to remain the primary earnings driver, with segment revenue projected to increase 61.3% YoY to US$1.66 billion, raising its

contribution to total revenue to 43% (vs 32% in FY25) and supporting total revenue growth of 20.6% YoY to US$3.82 billion.

We estimate FY26F net income to increase 13.3% YoY to US$514 million. Although higher raw material costs are expected to slightly compress margins, improved economies of scale and operating efficiency are projected to drive 22.3% YoY growth in operating profit, supporting overall earnings expansion.

By PHINTRACO SEKURITAS | Research

- Disclaimer On -

Baca Laporan

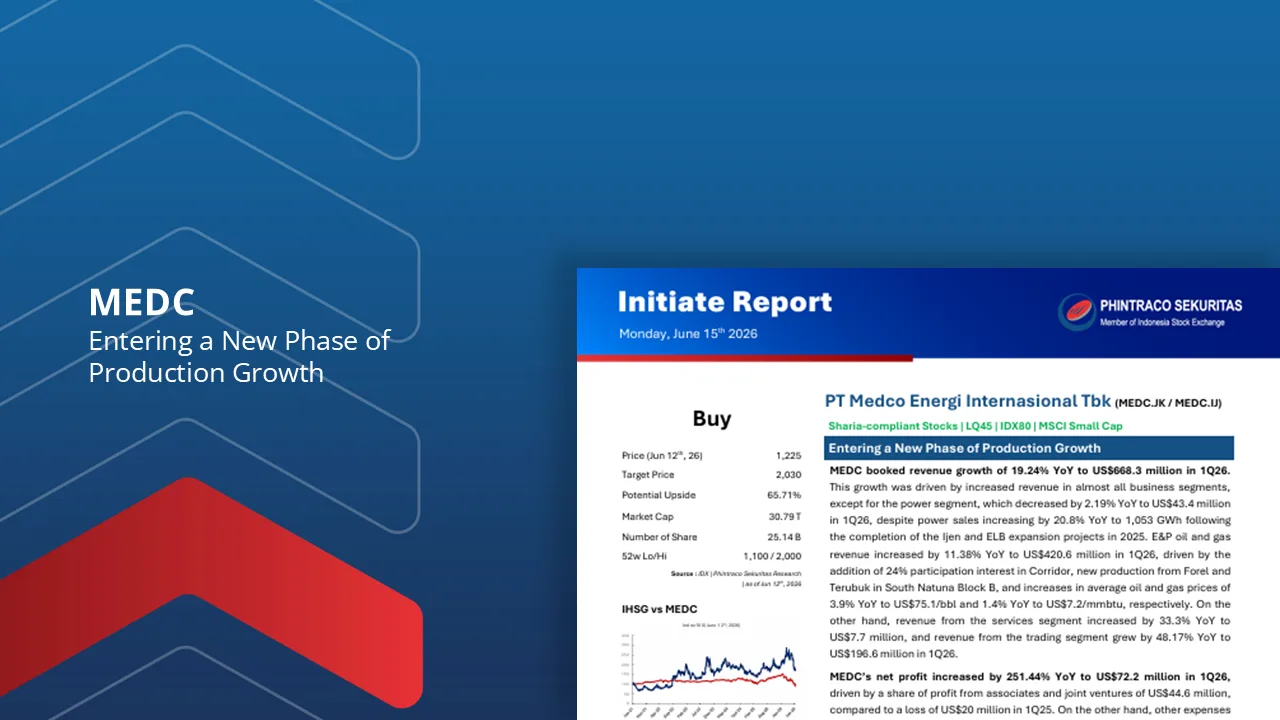

MEDC: Entering a New Phase of Production Growth

MEDC booked revenue growth of 19.24% YoY to US$668.3 million in 1Q26. This growth was driven by increased revenue in almost all business segments, except for the power segment, which decreased by 2.19% YoY to US$43.4 million in 1Q26, despite power sales increasing by 20.8% YoY to 1,053 GWh following the completion of the Ijen and ELB expansion projects in 2025.

E&P oil and gas revenue increased by 11.38% YoY to US$420.6 million in 1Q26, driven by the addition of 24% participation interest in Corridor, new production from Forel and Terubuk in South Natuna Block B, and increases in average oil and gas prices of 3.9% YoY to US$75.1/bbl and 1.4% YoY to US$7.2/mmbtu, respectively.

MEDC’s net profit increased by 251.44% YoY to US$72.2 million in 1Q26, driven by a share of profit from associates and joint ventures of US$44.6 million, compared to a loss of US$20 million in 1Q25. On the other hand, other expenses decreased to US$1.2 million in 1Q26, primarily due to foreign exchange losses turning into gains.

MEDC has a strategic position as an integrated oil and gas producer with significant exposure to oil prices. MEDC has a portfolio of upstream oil and gas assets spread across Indonesia, the Middle East, and Southeast Asia. The exploration and production (E&P) business remains the primary contributor to the Company’s revenue and EBITDA, placing MEDC in an advantageous position as global oil prices remain at high levels.

MEDC has entered a phase of stronger production growth following the successful operation of several strategic oil and gas projects resulting from investments made over the past few years. The operation of the Forel and Terubuk fields in Natuna, which have a production capacity of approximately 30 mboepd, has become the primary catalyst for increased production volumes while also strengthening the Company’s operating cash flow.

By PHINTRACO SEKURITAS | Research

- Disclaimer On -

Baca Laporan

Sectoral Update

Read More

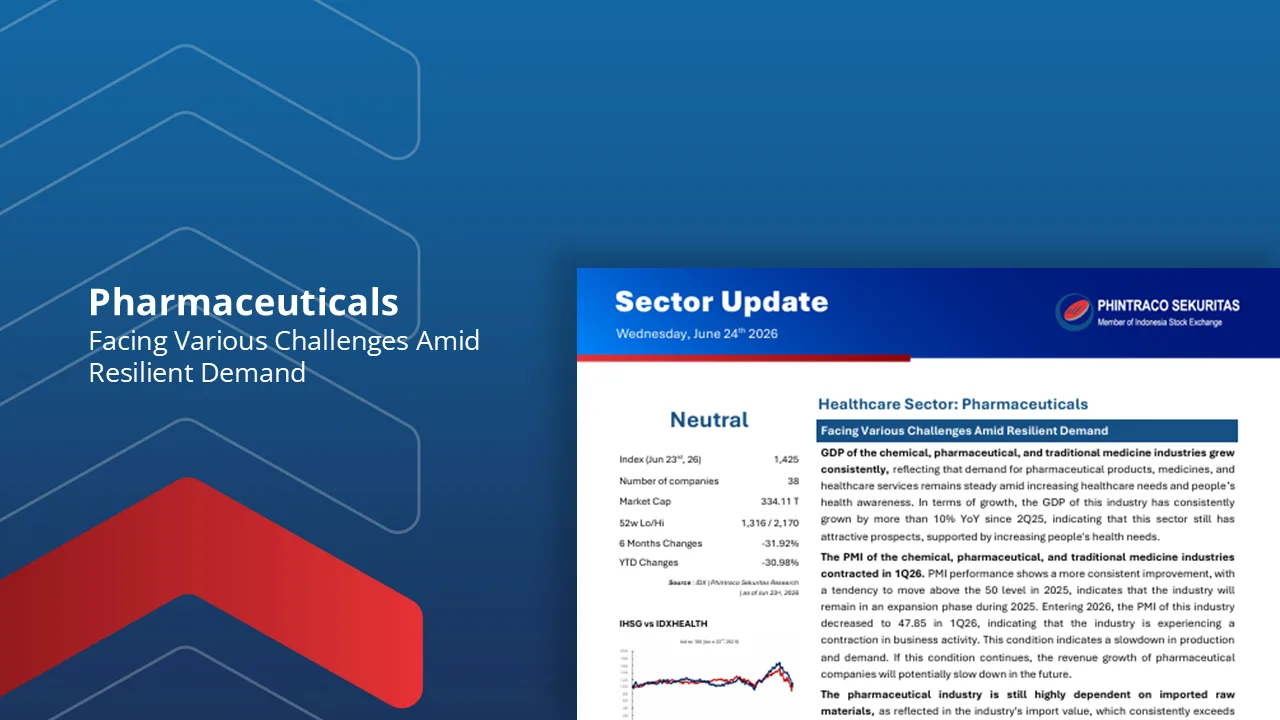

Pharmaceuticals Sector: Facing Various Challenges Amid Resilient Demand

GDP of the chemical, pharmaceutical, and traditional medicine industries grew consistently, reflecting that demand for pharmaceutical products, medicines, and healthcare services remains steady amid increasing healthcare needs and people’s health awareness.

The PMI of the chemical, pharmaceutical, and traditional medicine industries contracted in 1Q26. This condition indicates a slowdown in production and demand. If this condition continues, the revenue growth of pharmaceutical companies will potentially slow down in the future.

The pharmaceutical industry is still highly dependent on imported raw materials, as reflected in the industry's import value, which consistently exceeds its export value. This condition has caused the sector’s trade balance to consistently experience a deficit.

The performance of the pharmaceutical companies in our coverage

is mixed. KLBF booked revenue growth of 10.13% YoY in 1Q26. This growth was driven by increased sales across all business segments.

Downside risks in this sector include a more-than-expected weakening of purchasing power, restrictions on expansion, and intense competition with e-commerce platforms. Meanwhile, SIDO booked a revenue decrease of 18.83% YoY in 1Q26, primarily due to SIDO’s inventory normalization efforts in its distribution channels.

Downside risks in this sector include dependence on imported raw materials, the risk of changes in pharmaceutical regulations, and intense competition between industry players.

By PHINTRACO SEKURITAS | Research

- Disclaimer On -

Baca Laporan

Plantation: Demand Takes the Lead

**Phintraco Sekuritas Sector Update**

**Plantation Sector**

**Aditya Prayoga**

> The plantation sector's performance in 1Q26 showed a quarterly normalization following the strong performance recorded in 4Q25. Aggregate revenue grew 7.3% YoY to IDR 16.0 Trillion, but declined 3.8% QoQ as the peak production and harvesting season came to an end, resulting in lower sales volumes across most companies under our coverage. A similar trend was reflected in aggregate gross profit and net profit, which declined by 22.9% QoQ and 14.3% QoQ, respectively.

> STAA recorded the strongest growth within our coverage universe, with revenue rising 49.2% YoY to IDR 2.5 Trillion, driven by the contribution from its refinery business, which was not reflected in 1Q25. However, its quarterly performance also normalized, with revenue and net profit declining by 20.0% QoQ and 31.6% QoQ, respectively. In terms of profitability, SSMS remained the sector leader with a GPM of 36.0%, while AALI posted the lowest margins, with a GPM of 15.5% and an NPM of 5.0%.

>We expect Indonesia’s CPO production to remain relatively stagnant in FY26F at around 58 million tons (+0–1% YoY) While 2H26 production is likely to be slightly stronger than 1H26, supported by seasonal patterns where approximately 53% of annual output is generated in the second half, we believe the improvement will be largely seasonal in nature.

>Looking ahead, the potential emergence of El Niño in 2H26 remains a factor worth monitoring. Nevertheless, we believe the risk to FY26F production remains relatively limited, given that weather-related impacts on palm oil productivity typically materialize with a lag of 9–12 months. As a result, any stronger-than-expected El Niño event is more likely to affect the FY27F production outlook rather than FY26F.

> On the demand side, the implementation of the mandatory B50 biodiesel program, effective from 1 July 2026, is expected to significantly increase domestic CPO consumption. Based on the government’s simulation, CPO demand for biodiesel could rise to approximately 17.9 million tons (+33.4%), creating additional demand of around 4.35 million tons compared to the current B40 scheme. As domestic demand growth is expected to outpace supply growth, market balances could tighten further and support CPO prices.

> External demand is also expected to remain supportive. India's seasonal restocking cycle ahead of the Diwali festival is likely to strengthen imports during 2H26, while recent data suggest that China's palm oil imports are beginning to recover after several years of decline. We believe these factors should help absorb additional supply entering the market during the second half of the year.

>Downside risks to our view include: (1) volatility in CPO and other vegetable oil prices, (2) changes in biodiesel or export policies, and (3) higher-than-expected fertilizer and operating costs resulting from geopolitical tensions and global supply chain disruptions.

Full Report : https://phintracosekuritas.com/

By PHINTRACO SEKURITAS | Research

– Disclaimer On –

Baca Laporan

Telco : Monetization Remains the Key Earnings Driver

**Phintraco Sekuritas Sector Update**

**Telecommunication Sector**

**Aditya Prayoga**

**Telecommunication: **Monetization Remains the Key Earnings Driver**

> The telecommunications sector delivered relatively solid earnings growth in 3M26, with aggregate revenue increasing 9.2% YoY to IDR 64.23 Trillion. The growth was primarily driven by the consolidation impact at EXCL following the merger of XL Axiata and Smartfren into XLSmart, which lifted EXCL's revenue by 37.4% YoY to IDR 11.82 Trillion. Excluding the merger impact, sector growth was more moderate, as reflected in revenue growth of 12.1% YoY at ISAT and 1.5% YoY at TLKM.

> On the profitability front, sector EBITDA increased 5.7% YoY to IDR 30.62 Trillion. However, EBITDA margin contracted to 47.2% (-1.9ppt YoY), indicating that revenue growth has yet to be fully accompanied by operating efficiency improvements. At the bottom-line level, aggregate net profit declined 30.0% YoY to IDR 5.07 Trillion, primarily due to weaker earnings from TLKM and the ongoing post-merger integration process at EXCL.

> The SIM card starter pack repricing strategy implemented since last year continued to support customer monetization improvement. This was reflected in sector ARPU, which increased 13.2% YoY to IDR 45.9K, supported by a 17.2% YoY increase in data consumption to 14.5K PB and higher average data usage per subscriber, reaching 48.3 GB (+15.7% YoY). As a result, sector data yield improved by 5.8% YoY to IDR 2,905/GB.

> Despite the strong improvement in monetization, the aggregate subscriber base remained relatively stable at 320.1 million subscribers (+2.3% YoY; -0.8% QoQ), suggesting that industry growth is increasingly being driven by improving revenue quality rather than subscriber expansion. Among operators, TLKM recorded the strongest data yield growth (+25.9% YoY), while ISAT continued to deliver robust data traffic growth (+25.1% YoY).

> Looking ahead, we see two key catalysts that could shape the sector in FY26, namely the upcoming 700 MHz and 2.6 GHz spectrum auctions and the implementation of facial verification-based SIM registration starting in July 2026. We believe both initiatives have the potential to improve network capacity while enhancing the quality of the industry's subscriber base.

> While facial verification-based SIM registration could lead to a c.5–10% decline in subscriber numbers in the near term due to customer base cleansing, we view the impact positively as it should improve subscriber quality and support stronger monetization. At the same time, additional spectrum allocation is expected to strengthen network quality and support future data traffic growth.

> Downside risks to our view include: (1) weaker-than-expected ARPU growth due to softer consumer purchasing power, (2) a larger-than-expected decline in subscriber numbers following customer base cleansing, and (3) higher-than-expected spectrum acquisition costs and capex requirements.

Full Report : https://phintracosekuritas.com

By PHINTRACO SEKURITAS | Research

– Disclaimer On –

Baca Laporan

Macro Flash

Read More

Indonesia’s M2 Growth Eased to 8.7% YoY in June 2026 Due to Lower Net Claims on Central Government Growth

Broad money supply (M2) recorded an 8.7% YoY growth to Rp10,432.8 trillion in June 2026, lower than a 10.8% YoY growth in May 2026. According to the M2 components, the growth was supported by a growth of narrower money supply (M1) which grew by 9.8% YoY to Rp5,937.5 trillion and quasi-money which grew by 6.9% YoY to Rp4,409.3 trillion in June 2026. Moreover, the growth of M2 was also influenced by the growth of loan distribution (12.1% YoY) and net claims on central government (NCG) (10.1% YoY) in June 2026.

Baca Laporan

Bank Indonesia Keeps Interest Rate Unchanged at 5.75% in July 2026 to Maintain Rupiah Stability

The Bank Indonesia (BI) Board of Governors’ Meeting (RDG) held on July 21-22, 2026, ended up with a decision to hold the interest rate at 5.75% after 100bps hikes in the last two months. In addition, BI also kept the Deposit Facility and Lending Facility Rate unchanged at 4.75% and 6.50%, respectively. To strengthen the stability of the Rupiah exchange rate, accelerate the deepening of the money market and foreign exchange market (PUVA), as well as increase liquidity and reduce liquidity segmentation in the money and banking markets, BI will expand incentive policies and various other policies. The decision remains consistent in strengthening Rupiah stability amid global uncertainty and keeping inflation within the target range set by the government of 2.5±1%.

Baca Laporan

Indonesia’s State Budget Recorded a Deficit of 0.76% of GDP through End of 1H26

Indonesia’s State Budget and Revenue (APBN) realization recorded a deficit of Rp196.5 trillion in 1H26, equivalent to 28.5% of APBN 2026 target. The deficit in 1H26 slightly declined from the deficit of Rp204.2 trillion in 1H25. The deficit reflects a risk on Indonesia’s fiscal room as the deficit rose significantly since 2022 for the cumulative period from January until June each year. However, the Indonesia’s fiscal deficit ratio (-0.76%) to Gross Domestic Product (GDP) realization in 1H26 still relatively maintained below the proper fiscal threshold of 3%. This indicates that there is still a fiscal room that allows APBN to act effectively in tackling the global economic turmoil disruption while also stabilize the domestic economic stability.

Baca Laporan

Market Outlook

Read More

Higher for Longer: The New Market Reality

Middle East geopolitical tensions disrupted global energy supply, pushing up oil prices and increasing pressure on inflation, exchange rates, and global monetary policy.

The US–Iran peace agreement and the planned reopening of the Strait of Hormuz improved market sentiment and eased oil prices, although geopolitical risks remain.

Global growth is expected to moderate in 2026, with persistent market volatility driven by energy prices, inflation, and higher-for-longer interest rates.

Indonesia targets 5.4% GDP growth in 2026, supported by fiscal stimulus, while inflation is expected to remain within Bank Indonesia's target range in 2H26.

Bank Indonesia is expected to maintain a tight monetary stance amid Rupiah depreciation, global rate pressures, and inflation risks.

Fiscal conditions remain manageable, with the 2026 budget deficit reaching 0.7% of GDP by May, still well below the full-year target despite widening from last year.

Foreign investors are likely to remain cautious, as the market awaits MSCI's market accessibility review and S&P's sovereign credit rating assessment.

By PHINTRACO SEKURITAS | Research

- Disclaimer On -

Baca Laporan

Global Economic Research : Embracing the Economic Dynamics of 2026

Global economic growth is expected to keep slowing amid high global uncertainty. This situation continues to weigh on trade, investment, and overall economic performance.

U.S. President Donald Trump’s import tariff policies have created uncertainty, though recent negotiations indicate potential progress. Efforts toward a U.S.–China trade deal, including partial tariff cuts and delayed export restrictions, are offset by new risks from stricter transshipment monitoring.

Artificial Intelligence (AI) is transforming the global economy by automating production and addressing labor shortages. The integration of AI and robotics enhances industrial efficiency and supports productivity through adaptive labor and migration policies.

Global inflation pressures have eased except in the U.S., Europe, and the U.K., driven by import tariffs and strong demand. Several major central banks have started to cut interest rates, while others remain cautious to maintain stability.

Global fiscal conditions are becoming more fragile due to geopolitical tensions, U.S. tariff policies, and high public debt. Expansionary fiscal policies and rising interest rates are increasing debt costs and limiting fiscal space.

Geopolitical tensions continue to disrupt supply chains, raising energy and food prices. However, global commodity prices in 2025 show mixed trends, influenced by weaker demand, supply disruptions, and climate change.

By PHINTRACO SEKURITAS | Research

- Disclaimer On -

Baca Laporan

Indonesia Economic Research: Embracing the Economic Dynamics of 2026

Indonesia's economy is projected to grow 5.0%-5.2% YoY in 2026. Indonesia's economic growth is expected to accelerate in 2026, in line with expectations of improving global conditions and increased domestic investment activity.

Consumer confidence index and retail sales are expected to remain positive in 2026. Supported by the government's stimulus program, assuming controlled inflation and consumption incentive.

Inflation in 2026 is expected to remain within BI's target range of 2.5% ± 1%. This projection is based on relatively stable inflation expectations at low levels, the stability of the Rupiah exchange rate, and synergistic efforts by Bank Indonesia and the Government.

The opportunity for further cuts by Bank Indonesia (BI) Rate remains possible in 2026. This projection is based on relatively stable inflation expectations at low levels, the stability of the Rupiah exchange rate, and synergistic efforts by Bank Indonesia and the Government.

The allocation of government funds in banks has positively influenced national liquidity. By September 2025, the adjusted base money rose to Rp2,152.4 trillion, up from Rp1,961.34 trillion in August 2025.

The 2026 APBN deficit is targeted at 2.68% of GDP. The 2026 APBN targets state revenue at IDR 3,153.6 trillion, comprising IDR 2,357.7 trillion in tax revenue and IDR 336 trillion in customs and excise revenue.

IHSG's conservative level for 2026 is estimated at 9,255 and its aggressive level at 9,883.

Sectoral Coverage: Banks, Properties & Real estate, F&B and Poultry, Retails, Telecommunication, Tower, Coal, Pharmaceuticals, Plantations, Construction, Metals & Mining, Industrial, and Cement.

By PHINTRACO SEKURITAS | Research

- Disclaimer On -

Baca Laporan

Monthly Strategy

Read More

Bond Monthly Strategy: Indonesia Bond Market Faces Higher Yield Risks Amid Global Volatility and Hikes Policy Rate

Indonesia’s government bond yield curve continues to bearishly flatten, with short-to-medium tenors amid higher front-end risk premiums, fiscal concerns, and persistent global market volatility.

Bank Indonesia raised the BI Rate by 50 bps to 5.25% to support Rupiah stability and maintain attractive real yield swhile domestic inflation has started to moderation.

The Federal Reserve is expected to keep rates unchanged at 3.50%–3.75% in the near term, as markets price a 99.4% probability of no change in June 2026, reflecting policymakers’ caution toward inflation and geopolitical risks.

The latest Fed Dot Plot signals a gradual and shallow easing cycle, with the median Fed Funds Rate projected at 3.375% by end-2026 and 3.125% by end-2027, reinforcing the higher-for-longer interest rate environmen

Limited policy flexibility from Bank Indonesia, driven by Rupiah depreciation, declining foreign exchange reserves, and ongoing geopolitical uncertainties, is expected to keep upward pressure on government bond yields and reduce the likelihood of near-term rate cuts.

By PHINTRACO SEKURITAS | Research

-Disclaimer On-

Baca Laporan

Equity Monthly Strategy: Navigating Market Volatility in a Higher-for-Longer Era

Global Highlight: Global economic conditions remained relatively resilient despite geopolitical tensions and the temporary Strait of Hormuz disruption, supported by stable oil prices, resilient U.S. economic activity, and improving manufacturing and services data. Although U.S. inflation pressures increased due to higher energy costs, stable labor market conditions and easing recession risks reinforced expectations that the Federal Reserve will maintain a “higher-for-longer” interest rate stance in the near term.

Indonesia Highlight: Indonesia’s economy remained resilient in 1Q26, supported by strong household consumption, rising government spending, and recovering manufacturing activity. However, pressure from Rupiah depreciation, capital outflows, widening balance of payments deficits, and rising inflation prompted Bank Indonesia to raise interest rates to 5.25% to maintain currency stability amid heightened global uncertainty and Middle East tensions.

IHSG View: Global equity markets remained volatile in May 2026 amid uncertainty over a potential U.S.-Iran peace agreement, rising inflation concerns, and fluctuations in global bond yields. Domestically, the JCI declined 29.14% YTD due to Rupiah depreciation, BI Rate hikes, MSCI and FTSE rebalancing pressures, and uncertainty surrounding several government policies. Looking ahead, investors are expected to closely monitor Indonesia’s MSCI Market Accessibility Review, FTSE Russell rebalancing, export policy implementation, and mining royalty revisions, while JCI outlook for 2026 remains supported by projected earnings growth.

Sector Allocation:

Banks, Oil & Gas, F&B, Metal Mining, and Cement. Read more for the Stock pick.

By PHINTRACO SEKURITAS | Research

- Disclaimer On -

Baca Laporan

Equity Monthly Strategy : From Global Volatility to Local Pressures: Navigating Market Trends

-May 2026-

Global Highlight: Global conditions weakened as U.S., Israel, Iran tensions escalated, with the Strait of Hormuz closure disrupting arround 20% of global oil supply and raising stagflation risks. Ongoing military tensions and fragile ceasefire efforts continue to pressure markets and supply chains. Meanwhile, the U.S. economy remains relatively resilient, though moderating growth and energy driven inflation support a higher for longer interest rate outlook.

Indonesia Highlight: Bank Indonesia kept rates at 4.75% amid global uncertainty and rupiah pressure, while inflation eased to 2.42% YoY in April 2026 on lower food prices. FX reserves declined due to intervention, and although retail sales and trade surplus remained supportive, weakening consumer confidence and a contractionary PMI indicate softer economic momentum.

IHSG View: The JCI decreased 1.3% MoM in April 2026 (-19.55% YTD), pressured by rising oil prices, capital outflows, and negative bank outlook revisions, with continued foreign net sell and MSCI uncertainty. Market volatility is expected to persist, with the JCI projected at 8,157-8,625, supporting a selective strategy on fundamentally strong sectors.

Sector Allocation:

Metal Mining, Oil & Gas, Retailers, Poultry, Banks, and Infrastructure. Read more for the Stock pick.

By PHINTRACO SEKURITAS | Research

- Disclaimer On -

Baca Laporan