MYOR : Profitability Improved Driven by Product Selling Price Adjustment in 4Q24

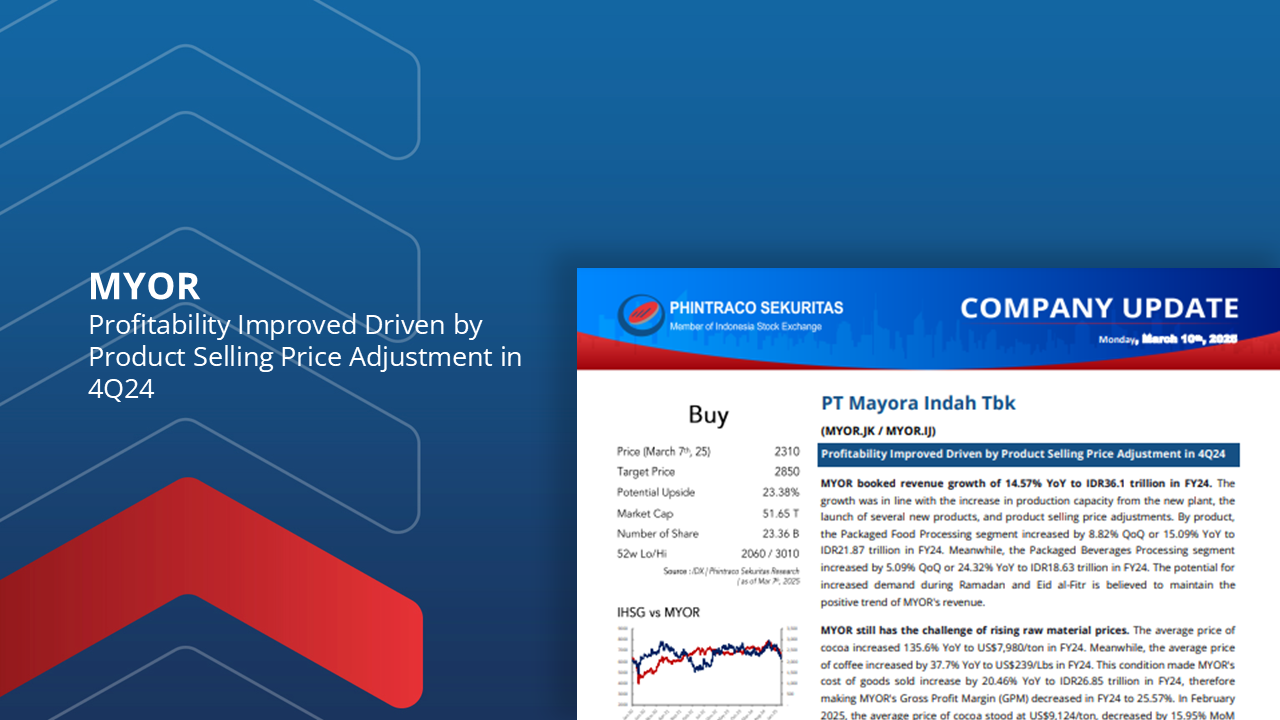

MYOR booked revenue growth of 14.57% YoY to IDR36.1 trillion in FY24. The growth was in line with the increase in production capacity from the new plant, the launch of several new products, and product selling price adjustments. The potential for increased demand during Ramadan and Eid al-Fitr is believed to maintain the positive trend of MYOR’s revenue.

MYOR still has the challenge of rising raw material prices. The average price of cocoa increased 135.6% YoY to US$7,980/ton in FY24. Meanwhile, the average price of coffee increased by 37.7% YoY to US$239/Lbs in FY24. This condition made MYOR’s cost of goods sold increase by 20.46% YoY to IDR26.85 trillion in FY24, therefore making MYOR’s Gross Profit Margin (GPM) decreased in FY24 to 25.57%. We assess that MYOR’s future profitability recovery will depend on the price normalization of both raw materials.

MYOR booked a net profit growth of 227% QoQ to IDR1 trillion in 4Q24. The growth was in line with the increase in revenue by 10.8% QoQ to IDR10.43 trillion due to the launch of several new products and product selling price adjustments made since October 2024. Meanwhile, on an annualized basis, MYOR’s net profit decreased by 5.46% YoY to IDR3.1 trillion in FY24 due to the higher raw material prices and higher interest expenses by 40.52% YoY to IDR425 billion in line with the issuance of IDR500 billion bonds.

MYOR is targeting revenue growth of 12-15% YoY in FY25, while GPM is targeted at 23-25%, assuming coffee and cocoa prices remain relatively stable until the end of 2025. In addition, MYOR has budgeted capital expenditures of IDR1 trillion in 2025, which are focused on driving expansion and increasing production capacity.

Using the Discounted Cash Flow method with a Required Return of 7.18% and Terminal Growth of 3.73%, we estimate MYOR’s fair value at IDR2,850 per share. Therefore, we maintain our Buy rating on MYOR with a lower target and potential upside of 23.38%.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –