MIDI : Potential Efficiency From Lawson Divestment

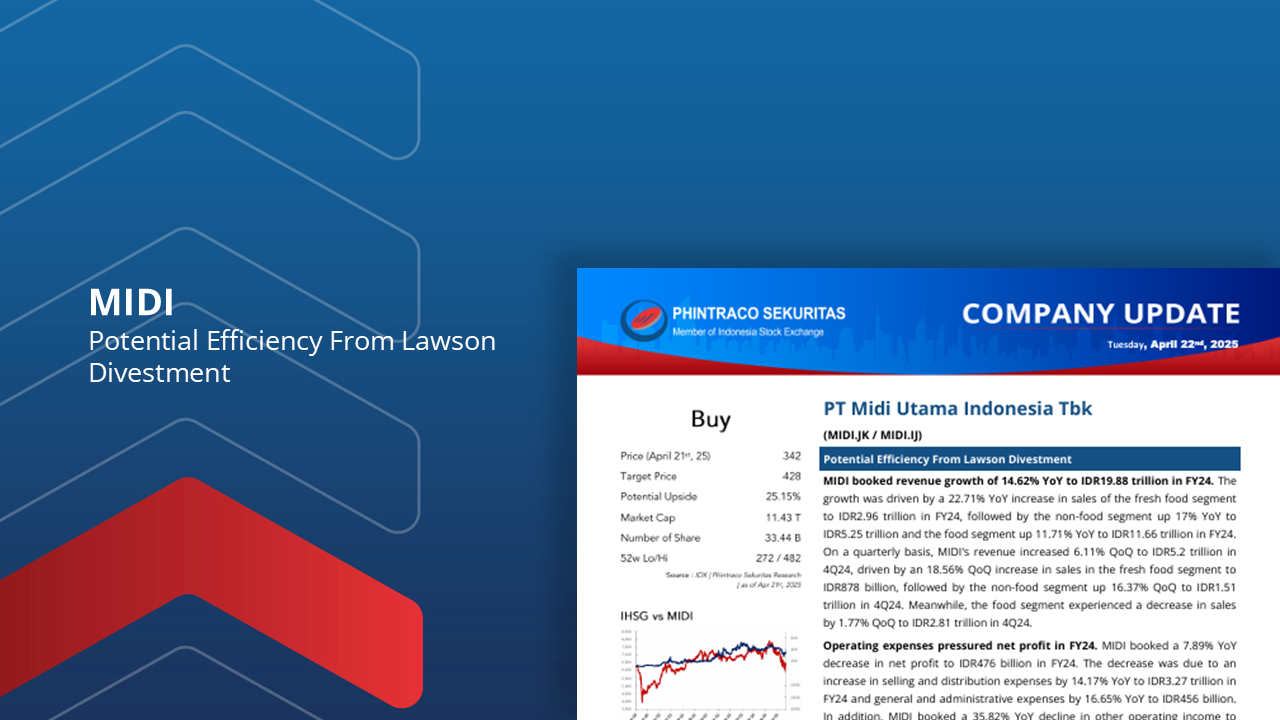

MIDI booked revenue growth of 14.62% YoY to IDR19.88 trillion in FY24. The growth was driven by a 22.71% YoY increase in sales of the fresh food segment to IDR2.96 trillion in FY24, followed by the non-food segment up 17% YoY to IDR5.25 trillion and the food segment up 11.71% YoY to IDR11.66 trillion in FY24.

Operating expenses pressured net profit in FY24. MIDI booked a 7.89% YoY decrease in net profit to IDR476 billion in FY24. The decrease was due to an increase in selling and distribution expenses by 14.17% YoY to IDR3.27 trillion in FY24 and general and administrative expenses by 16.65% YoY to IDR456 billion.

Continued expansion supported revenue growth in FY24. Alfamidi stores increased by 190 stores to 2,368 stores, and Alfamidi Super stores increased by 16 stores to 62 stores in FY24. Meanwhile, MIDI closed 3 Midi Fresh stores in FY24, bringing the number of MIDI Fresh stores to 5 stores.

MIDI divested Lawson to AMRT. This decision is based on considerations for implementing a more effective and efficient business strategy. With this transaction, MIDI is expected to improve and enhance its financial performance and focus more on its core business in the minimarket and supermarket segment.

Using the Discounted Cash Flow method with a Required Return of 9.58% and Terminal Growth of 3.88%, we estimate MIDI’s fair value at IDR428 per share. Therefore, we maintain our Buy rating on MIDI with a lower target and potential upside of 25.15%.