INDF : Operational Efficiency Drives EBITDA Improvement

INDF’s revenue grew limited 0.81% YoY to IDR30.7 trillion in 3M24. Despite the limited revenue growth, INDF recorded a Cost of Goods Sold (COGS) decline by 3.87% YoY to IDR19.5 trillion in 3M24. As a result, the gross profit grew significantly by 10.19% YoY to IDR11.2 trillion in 3M24.

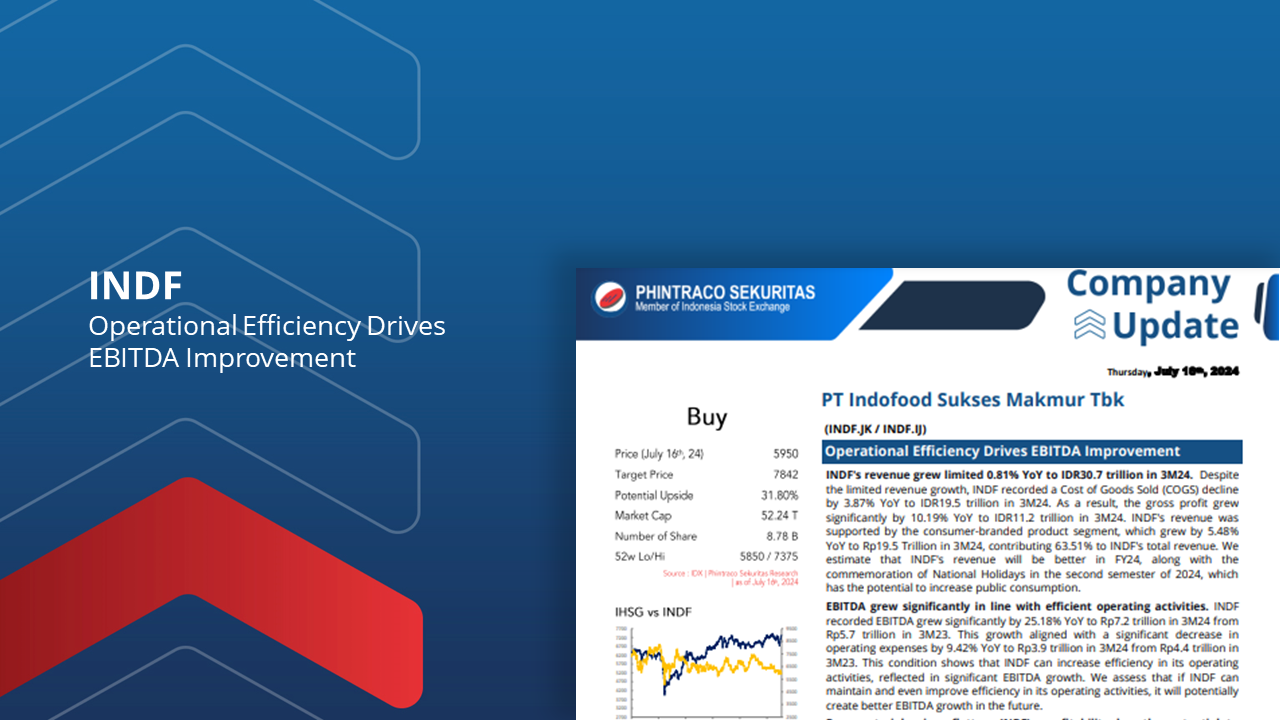

EBITDA grew significantly in line with efficient operating activities. INDF recorded EBITDA grew significantly by 25.18% YoY to Rp7.2 trillion in 3M24 from Rp5.7 trillion in 3M23. This growth aligned with a significant decrease in operating expenses by 9.42% YoY to Rp3.9 trillion in 3M24 from Rp4.4 trillion in 3M23. This condition shows that INDF can increase efficiency in its operating activities, reflected in significant EBITDA growth.

Raw material prices flatten, INDF’s profitability has the potential to stabilize. In producing its products, INDF utilizes critical raw materials such as CPO and Wheat, so its profitability depends on fluctuations in raw material prices. If CPO and Wheat prices are more stable in the future, INDF’s profitability will potentially stabilize.

The Company’s subsidiaries have a global bond burden in USD. PT Indofood CBP Sukses Makmur Tbk (ICBP), as a subsidiary of INDF restructured its debt to finance the acquisition of Pinehill Company Ltd. (PCL) by issuing four global bonds in USD. This action increased ICBP’s total debt in FY21, and its interest expenses also increased significantly. ICBP’s average sales growth post-PCL acquisition from 2020 to 2023 was 12.73%. Then, ICBP’s average net profit margin (NPM) from 2020 to 2023 is 12.78%, so we believe ICBP’s NPM will stabilize at a 2-digit level in the next few years. We estimate that this condition can cover high-interest expenses and minimize liquidity risk.

Using the Discounted Cash Flow method with Required Return of 8.05% and Terminal Growth of 2.75%, we estimate INDF’s fair value at IDR7,842 per share (Expected PE at 6.48x and EV/EBITDA at 3.91x in FY24). We give INDF a Buy rating with potential upside 31.80%.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –