BBCA: Credit Growth Accompanied by Maintained Credit Quality

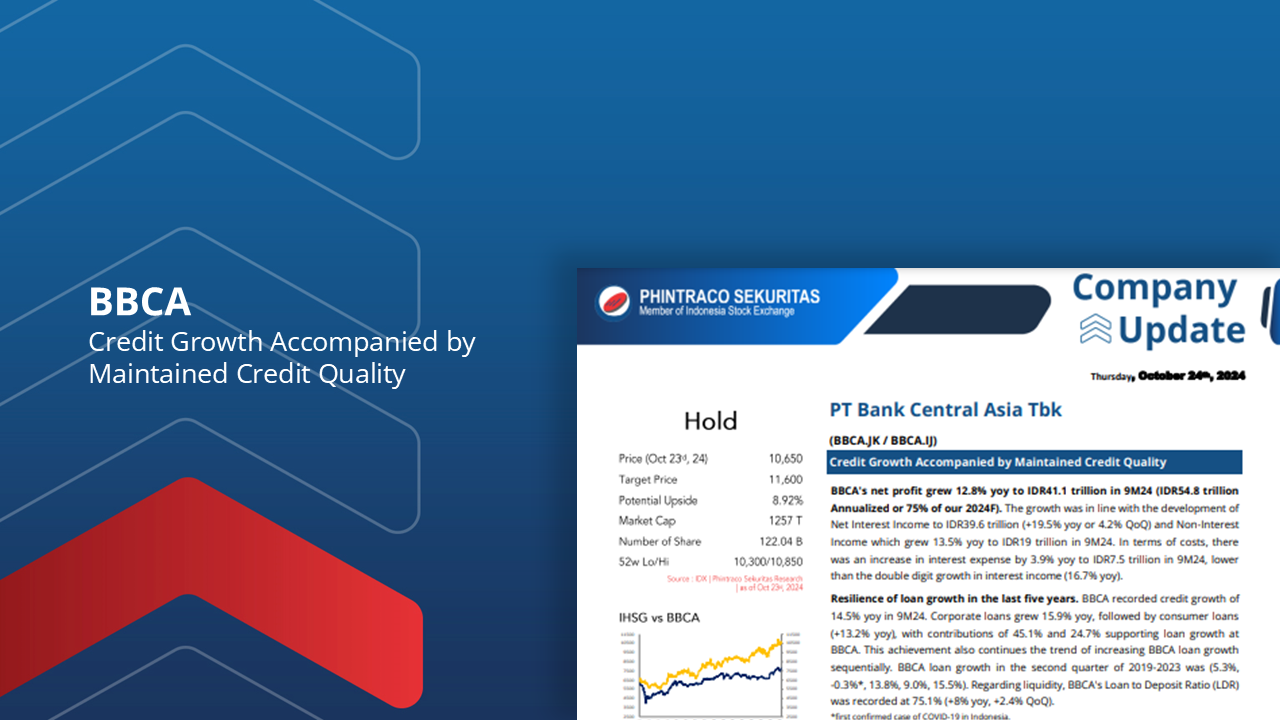

BBCA’s net profit grew 12.8% yoy to IDR41.1 trillion in 9M24 (IDR54.8 trillion Annualized or 75% of our 2024F).

Resilience of loan growth in the last five years. BBCA recorded credit growth of 14.5% yoy in 9M24.

BBCA’s credit quality remains healthy amid macroeconomic fluctuations.

Lowest Cost of Fund (COF) compared to peers amidst high interest rates. Despite high interest rates, BBCA’s cost of funds has remained stable in the last 5 years.

Strong customer relationships are BBCA’s competitive advantage. Customers increased by 5% yoy to 32.6 million in 9M24, with transaction volume reaching 26billion (+21%yoy) in 6M24.

Using the Discounted Cash Flow method with a Required Return of 6.81% and Terminal Growth of 8.09%, we estimate BCA’s fair value at 11,600 (26.14x expected P/E). Therefore, we maintain a hold rating for BBCA with a higher target and potential upside of 8.92%.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –