BTPS : Potential for continued asset quality improvements

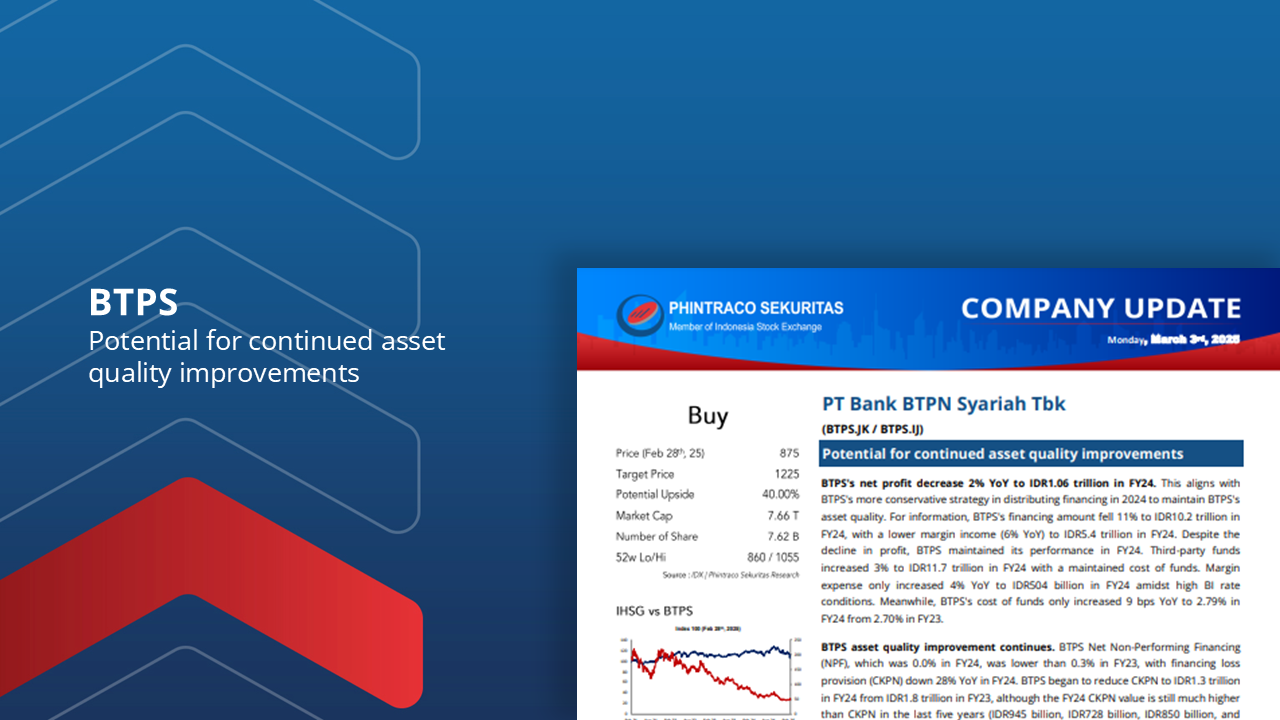

BTPS’s net profit decrease 2% YoY to IDR1.06 trillion in FY24. This aligns with BTPS’s more conservative strategy in distributing financing in 2024 to maintain BTPS’s asset quality.

BTPS asset quality improvement continues. BTPS Net Non-Performing Financing (NPF), which was 0.0% in FY24, was lower than 0.3% in FY23, with financing loss provision (CKPN) down 28% YoY in FY24.

BTPS focuses on reducing cycle one financing (new customers) to enhance asset quality. For information, the number of cycle one customers was 23% in FY24, lower than 29% in FY23 and 32% in FY22.

Consumer empowerment to increase consumer loyalty. BTPS has an empowerment program called bestee” to increase the capacity of its customers as entrepreneurs by providing them access to knowledge or assistance from contributors through an integrated digital platform.

With the potential of Islamic banking in Indonesia, asset quality and development, and improvement of BTPS service quality, We estimate BTPS’s net profit can grow ~3% in FY25F.

We estimate BTPS’ fair value at 1,225 (8.68x expected P/E). Considering BTPS’ fair price and relative valuation below 1.7x –1 standard deviation of 5-year P/B, we maintain our buy rating for BTPS with a potential upside of 40.00%.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –