BNGA: Optimize Consumer Loans with Maintained Liquidity

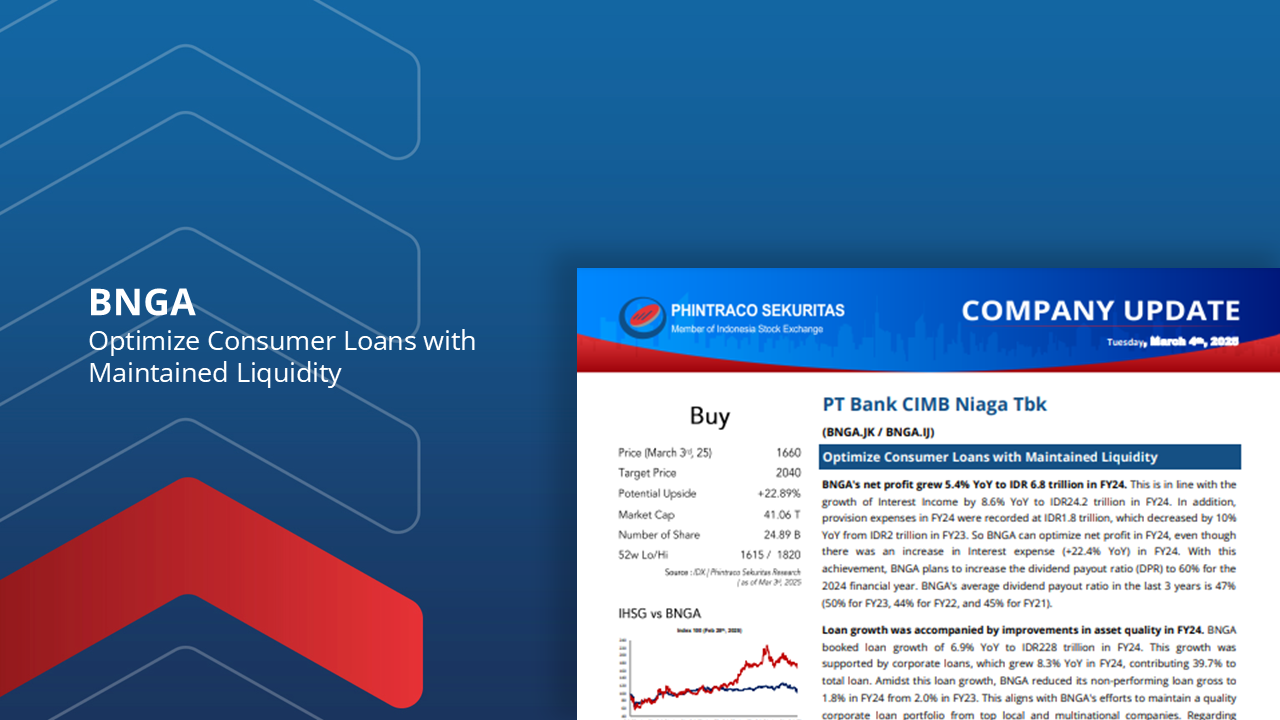

BNGA’s net profit grew 5.4% YoY to IDR 6.8 trillion in FY24. This is in line with the growth of Interest Income by 8.6% YoY to IDR24.2 trillion in FY24.

BNGA plans to increase the dividend payout ratio (DPR) to 60% for the 2024 financial year. BNGA’s average dividend payout ratio in the last 3 years is 47% (50% for FY23, 44% for FY22, and 45% for FY21).

Loan growth was accompanied by improvements in asset quality in FY24. BNGA booked loan growth of 6.9% YoY to IDR228 trillion in FY24.

Current Account Saving Account (CASA) grew 14.2% YoY to IDR172 trillion in FY24.

BNGA aims to optimize consumer loans through mortgage loan optimization and OCTO mobile. For the consumer segment, BNGA will optimize mortgage loans by focusing on secondary cities without ignoring big cities (with low Risk-Adjusted Return on Capital)

Using the Discounted Cash Flow method with a Required Return of 7.74% and Terminal Growth of 4.9%, we estimate BNGA’s fair value at Rp2,040 (7.15x expected P/E). Therefore, we maintain a buy rating for BNGA with a potential upside of 22.89%.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –