BDMN : Loan Growth Maintained with Good Asset Quality

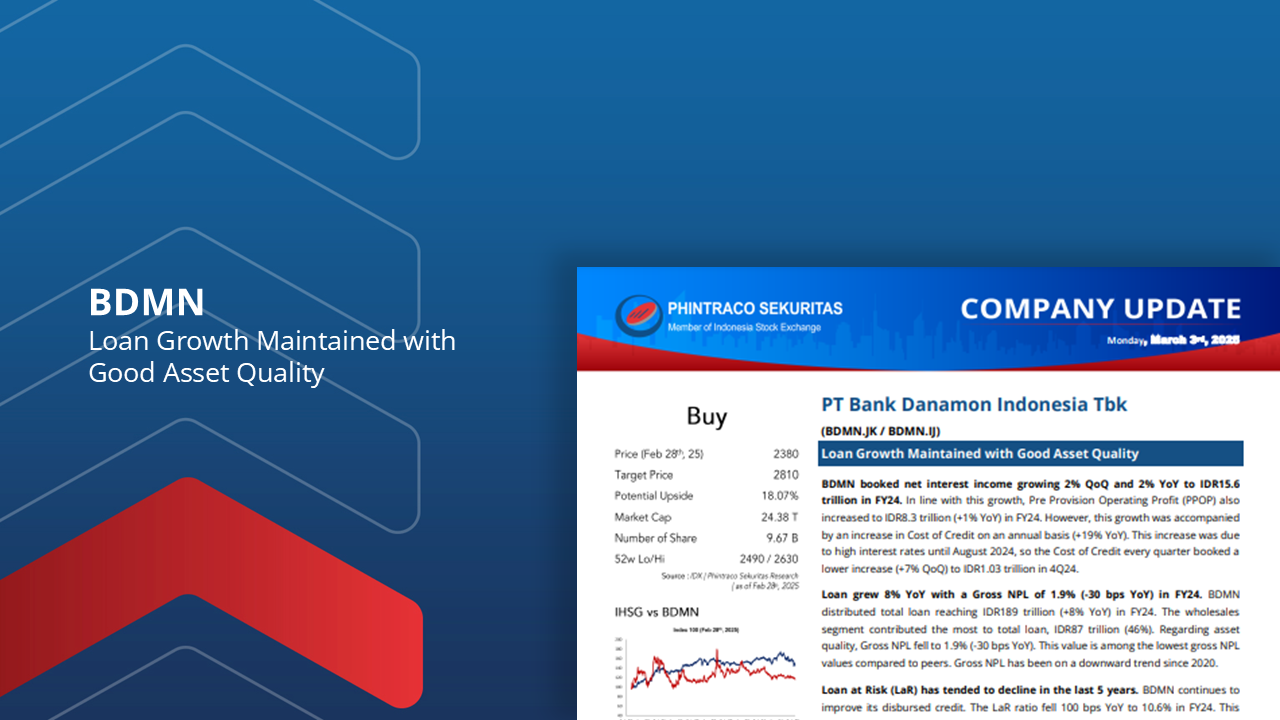

BDMN booked net interest income growing 2% QoQ and 2% YoY to IDR15.6 trillion in FY24. In line with this growth, Pre Provision Operating Profit (PPOP) also increased to IDR8.3 trillion (+1% YoY) in FY24.

Loan grew 8% YoY with a Gross NPL of 1.9% (-30 bps YoY) in FY24.This value is among the lowest gross NPL values compared to peers.

Loan at Risk (LaR) has tended to decline in the last 5 years. The LaR ratio fell 100 bps YoY to 10.6% in FY24.

Adira Finance’s contribution to total loan is maintained at around 30%. Adira Finance is the second highest contributing segment after wholesales to BDMN’s total loan.

Interest Income is estimated to grow 6% YoY to IDR15.6 trillion in FY25F. Management targets BDMN’s loan growth in 2025 of 9% to 11%, with Corporate loan is targeted to grow double digits.

Using the Discounted Cash Flow method with a Required Return of 7.93% and Terminal Growth of 1.35%, we estimate BDMN’s fair value at 2,810 (7.34x expected P/E). Therefore, we maintain a buy rating for BDMN with a potential upside of 18.07%

By PHINTRACO SEKURITAS | Research

– Disclaimer On –