BDMN : Credit Growth Maintained with Good Asset Quality

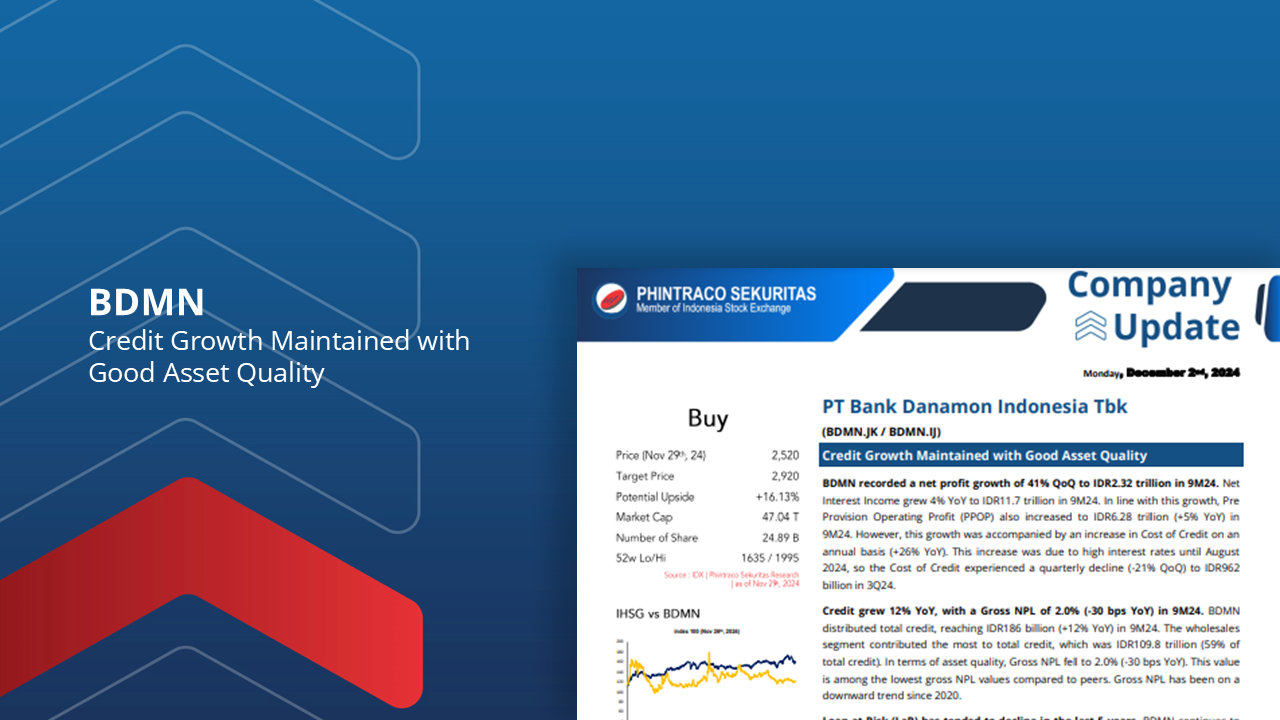

BDMN recorded a net profit growth of 41% QoQ to IDR2.32 trillion in 9M24. Net Interest Income grew 4% YoY to IDR11.7 trillion in 9M24.

Credit grew 12% YoY, with a Gross NPL of 2.0% (-30 bps YoY) in 9M24. BDMN distributed total credit, reaching IDR186 billion (+12% YoY) in 9M24.

Loan at Risk (LaR) has tended to decline in the last 5 years. BDMN continues to improve in terms of disbursed credit.

Adira Finance’s contribution to total credit is maintained at around 30%. Adira Finance is the second highest contributing segment after wholesales to BDMN’s total credit.

Interest Income is estimated to grow 9% to IDR13.7 trillion in FY24. Management targets BDMN’s credit growth 2024 of 9% to 10%.Corporate credit is targeted to grow double digits, with credit for the green energy sector reaching 25% of total credit in FY24.

Using the Discounted Cash Flow method with a Required Return of 8.5% and Terminal Growth of 1.6%, we estimate BDMN’s fair value at 2,920 (11.44x expected P/E). So, we give BDMN a buy rating with a potential upside of 15.21%.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –