BBRI : Performance below Expectation, Maintain buy with lower target price

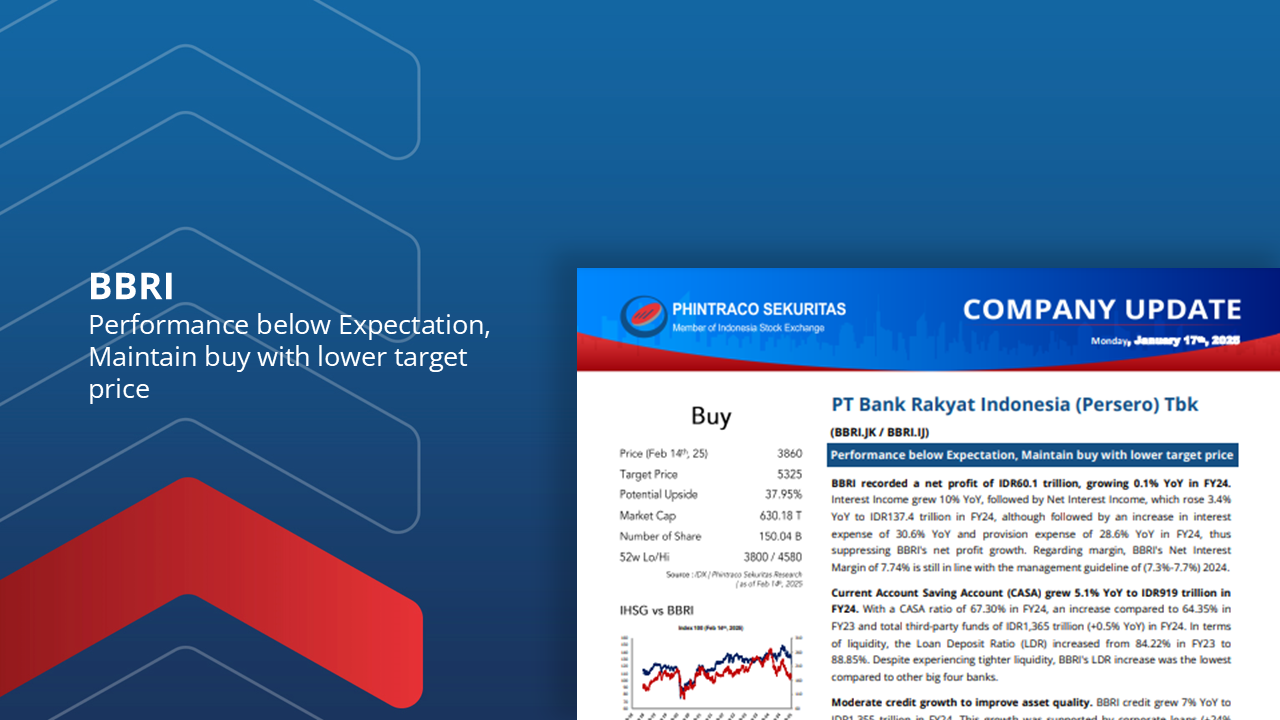

BBRI recorded a net profit of IDR60.1 trillion, growing 0.1% YoY in FY24. Interest Income grew 10% YoY, followed by Net Interest Income, which rose 3.4% YoY to IDR137.4 trillion in FY24.

Current Account Saving Account (CASA) grew 5.1% YoY to IDR919 trillion in FY24. With a CASA ratio of 67.30% in FY24.

Loan Deposit Ratio (LDR) increased from 84.22% in FY23 to 88.85%. Despite experiencing tighter liquidity, BBRI’s LDR increase was the lowest compared to other big four banks.

Moderate credit growth to improve asset quality. BBRI credit grew 7% YoY to IDR1,355 trillion in FY24.4. For FY25F, BBRI targets credit growth of 7%-9% lower than the 2024 target (10%-12%), which aligns with BBRI’s efforts to maintain asset quality.

Based on BBRI’s FY24 performance using the Discounted Cash Flow method, we maintain a BUY rating for BBRI with a fair value of 5.325 (12.94x expected P/E) and a relative valuation below 2.27x its 5-year average P/E and a potential upside of 37.95%.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –