TBIG: Balancing Challenges and Growth Potential Amidst a Moderate Outlook

3Q24 Financial Performance and Near-Term Challenges

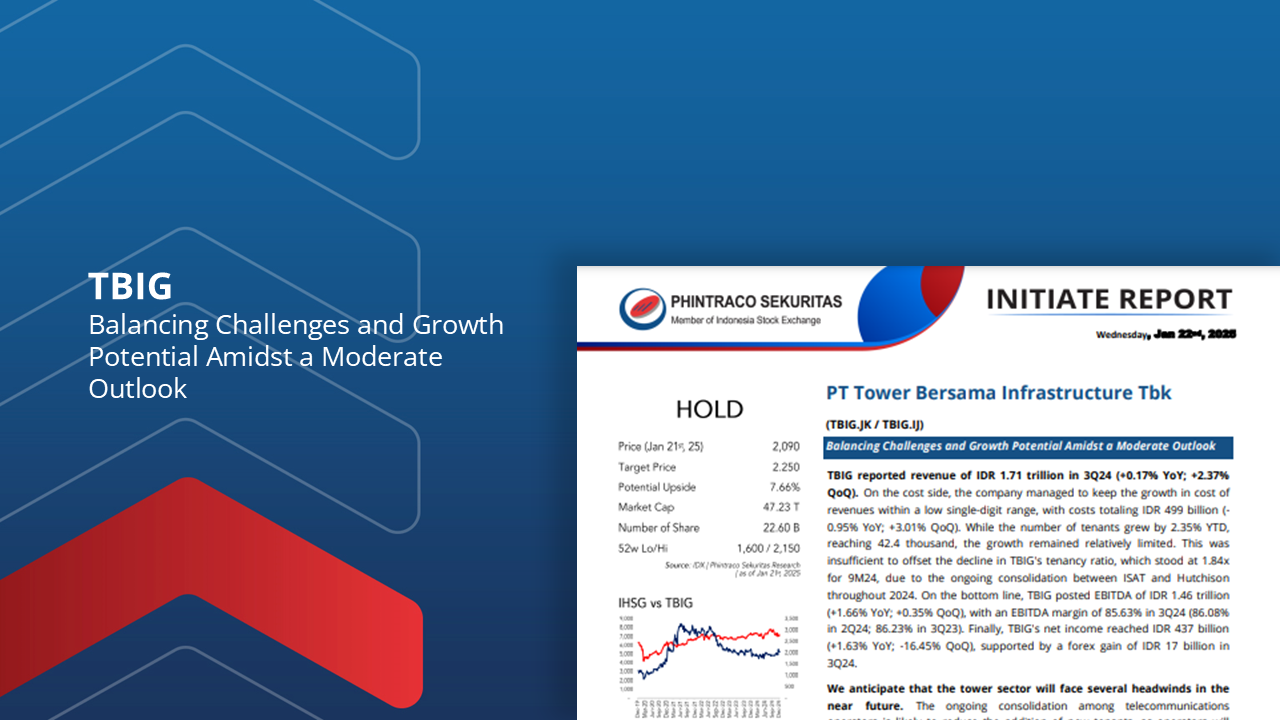

TBIG reported revenue of IDR 1.71 trillion in 3Q24 (+0.17% YoY; +2.37% QoQ), with EBITDA reaching IDR 1.46 trillion (+1.66% YoY; +0.35% QoQ) and an EBITDA margin of 85.63%. Despite a slight increase in revenue, tenant growth remains limited, with a total of 42.4 thousand tenants (+2.35% YTD). The decline in tenancy ratio to 1.84x for 9M24 reflects the impact of the ongoing consolidation between ISAT and Hutchison. We anticipate continued pressure through 2025 due to high interest rates and ongoing consolidation among telecommunications operators.

Moderate Growth Projection and Fiber Segment Contribution

Although the challenges of operator consolidation and high interest rates will limit growth, the fiber segment is expected to provide significant contribution to TBIG’s growth. We project TBIG’s topline to grow moderately by 8.08% in 2025F, with the fiber segment contributing 11.50% to revenue in 2025F. However, tenant growth is expected to remain flat, with a projected total of 43 thousand tenants by 2025 and a slight decrease in tenancy ratio to 1.79x.

Initiate Coverage with HOLD Rating

We initiate coverage on TBIG with a HOLD rating and a target price of IDR 2,250, implying an upside potential of 7.66%, which reflects an EV/EBITDA multiple of 12.50x for FY25F. Our valuation is based on a combination of DCF (70%) and EV/EBITDA multiple (30%). The HOLD rating is assigned considering the moderate sentiment we expect to prevail throughout 2025. Challenges such as ongoing telecommunications operator consolidation and relatively high interest rates are projected to limit TBIG’s growth potential. Upside risks include: (1) A reduction in interest rates, and (2) a low level of overlapping tenants.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –