ANTM: Despite declining revenue in 9M23, there was an increase in net profit

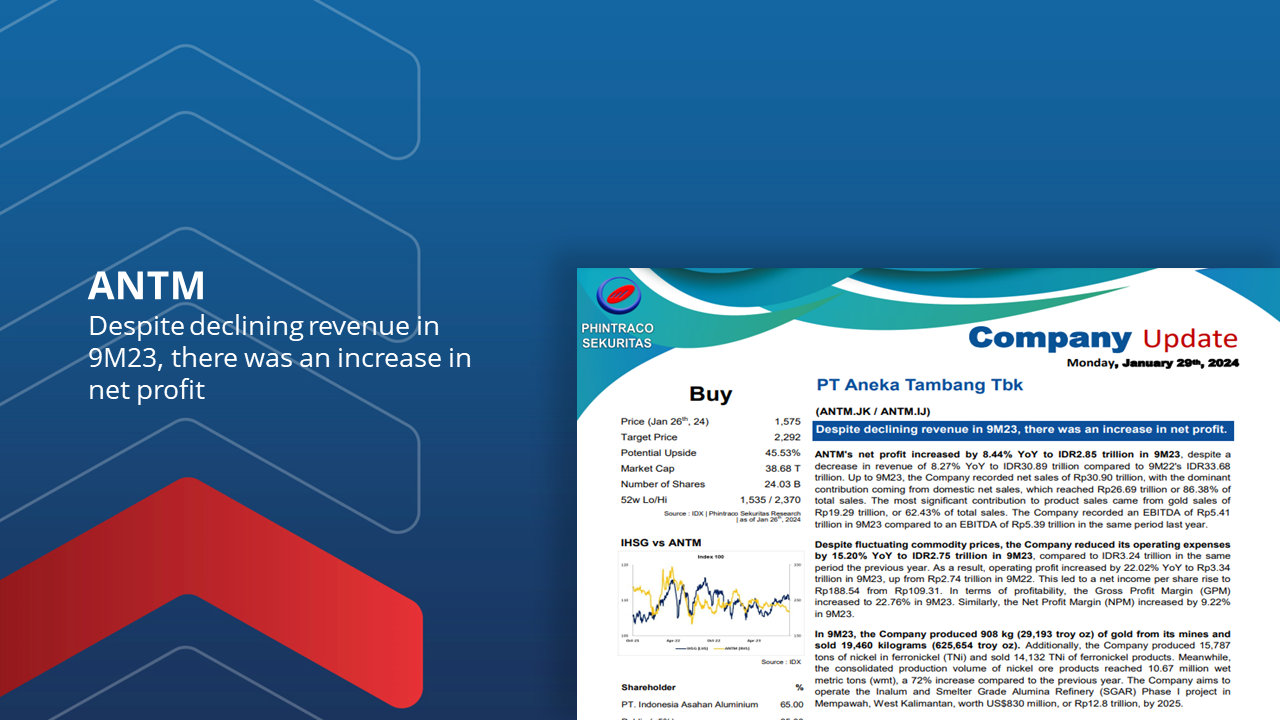

>ANTM’s net profit increased by 8.44% YoY to IDR2.85 trillion in 9M23, despite a decrease in revenue of 8.27% YoY to IDR30.89 trillion compared to 9M22’s IDR33.68 trillion.

>The most significant contribution to product sales came from gold sales of Rp19.29 trillion, or 62.43% of total sales.

>Despite fluctuating commodity prices, the Company reduced its operating expenses by 15.20% YoY to IDR2.75 trillion in 9M23, compared to IDR3.24 trillion in the same period the previous year.

>In 9M23, the Company produced 908 kg (29,193 troy oz) of gold from its mines and sold 19,460 kilograms (625,654 troy oz).

>The Company is collaborating with Ningbo Contemporary Brunp Lygend Co Ltd (CBL) to expedite the development of new renewable energy ventures.

>Sales growth is expected to decline by -2.14% in FY2023F. We further expect sales growth to normalize to 12.23% by FY2027F, which is still relatively high compared to the average of recent years due to the potential for additional production capacity and new product mix.

>Using the Discounted Cash Flow method with a Required Return of 9.72% and Terminal Growth of 5.01%, we estimate ANTM’s fair value at 2,292 (20.29x expected P/E). Based on ANTM’s fair price and potential upside of 39.34%, we recommend a buy rating for ANTM.