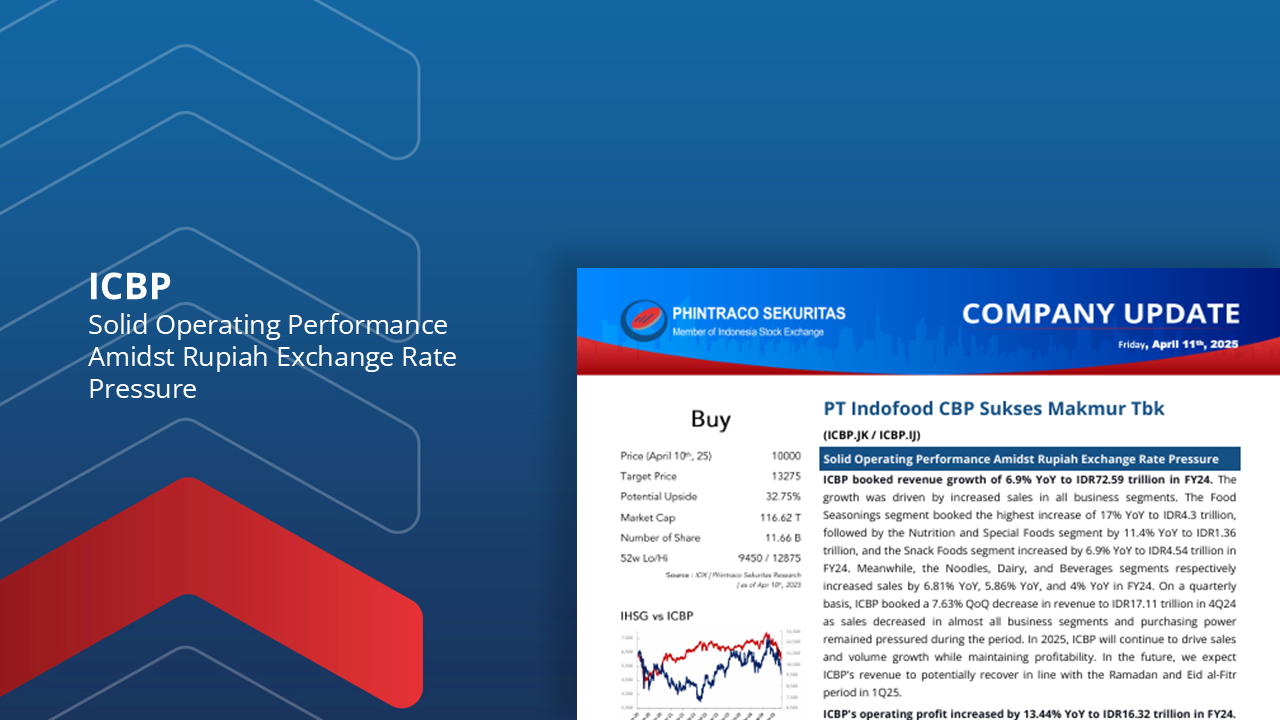

ICBP : Solid Operating Performance Amidst Rupiah Exchange Rate Pressure

ICBP booked revenue growth of 6.9% YoY to IDR72.59 trillion in FY24. The growth was driven by increased sales in all business segments. The Food Seasonings segment booked the highest increase of 17% YoY to IDR4.3 trillion, followed by the Nutrition and Special Foods segment by 11.4% YoY to IDR1.36 trillion, and the Snack Foods segment increased by 6.9% YoY to IDR4.54 trillion in FY24.

In 2025, ICBP will continue to drive sales and volume growth while maintaining profitability. In the future, we expect ICBP’s revenue to potentially recover in line with the Ramadan and Eid al-Fitr period in 1Q25.

ICBP’s operating profit increased by 13.44% YoY to IDR16.32 trillion in FY24. The growth aligned with lower operating expenses due to lower foreign exchange losses from operating activities. Operating profit growth in all segments also contributed to the increase in operating profit in FY24. Cumulatively, ICBP’s segment operating profit increased by 9.59% YoY to IDR16.19 trillion in FY24.

We estimate ICBP’s net profit to potentially increase by 6.77% YoY to IDR9.41 trillion in FY25F. This estimate aligns with the potential of solid operating performance to maintain profitability. On a quarterly basis, ICBP booked a net loss of IDR559 billion in 4Q24, bringing cumulative net profit to IDR8.81 trillion in FY24. The loss was mainly due to foreign exchange losses from financing activities of Rp2.11 trillion in 4Q24. In the future, the risk that needs to be considered is related to fluctuations in the rupiah exchange rate, which could potentially affect ICBP’s bottom line.

Using the Discounted Cash Flow method with a Required Return of 7.48% and Terminal Growth of 2.99%, we estimate ICBP’s fair value at IDR13,275 per share. Therefore, we maintain our Buy rating on ICBP with a lower target and potential upside of 32.75%.