“EXCL Result Update FY24 : Robust Performance Inline with Solid 4Q24 Results”

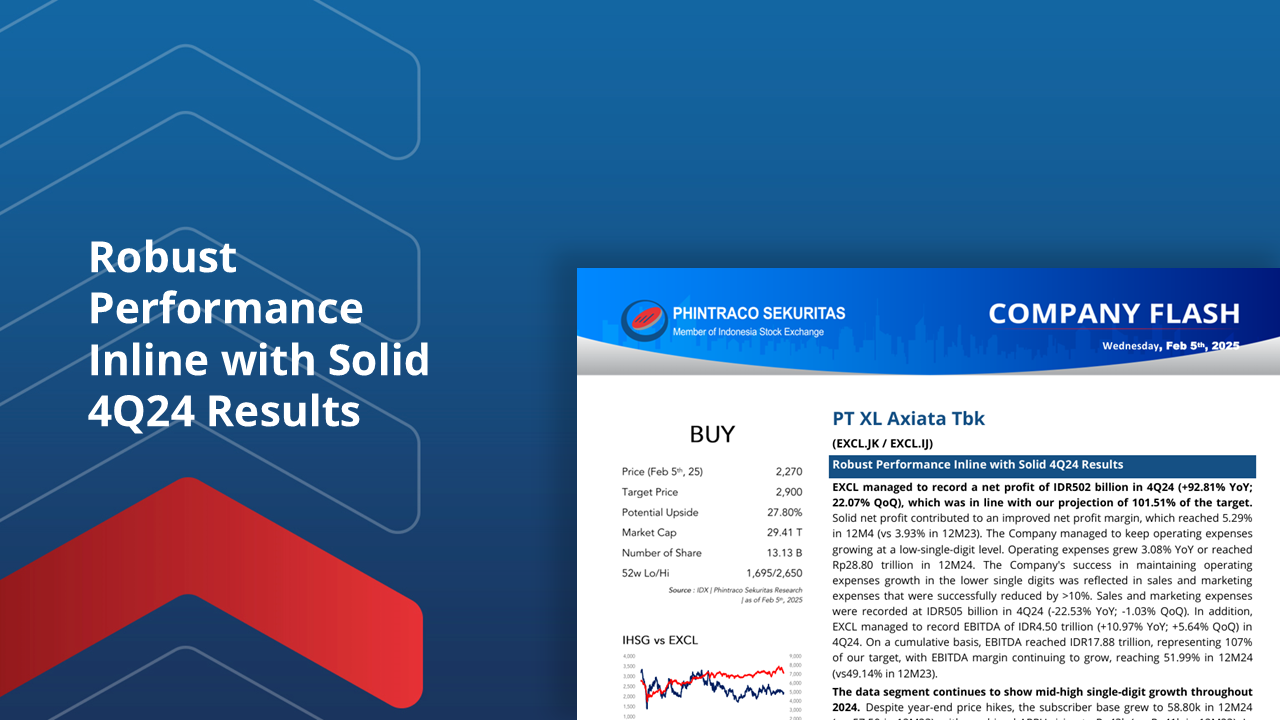

EXCL recorded a net profit of IDR502 billion in 4Q24 (+92.81% YoY; +22.07% QoQ), which was in line with our projection of 101.51% of the target. This solid net profit contributed to an improved net profit margin that reached 5.29% in 12M24 (vs 3.93% in 12M23). In addition, the company managed to keep operating expenses growing at the lower-single-digit level, with total operating expenses reaching Rp28.80 trillion in 12M24 (+3.08% YoY). This achievement was reflected in sales and marketing expenses that were successfully reduced by >10%, recording Rp505 billion in 4Q24 (-22.53% YoY; -1.03% QoQ). Overall, EXCL’s EBITDA was recorded at IDR4.50 trillion in 4Q24 (+10.97% YoY; +5.64% QoQ), with EBITDA margin continuing to grow reaching 51.99% in 12M24 (vs 49.14% in 12M23).

EXCL’s data segment continues to show mid-high single-digit growth throughout 2024, with data consumption rising sharply at year-end, reaching 2,724 petabytes in 4Q24 (vs 2,194 PB in 3Q24). The increase in data consumption was driven by high demand due to the momentum of Christmas, New Year, and regional elections. In the broadband sector, EXCL is now the second largest ISP player in Indonesia, with >1 million fixed broadband subscribers. Although its contribution to revenue is still relatively small (<10%), this segment shows attractive growth potential in the future.

We maintain a BUY rating on EXCL with a potential upside of 22.76% to IDR2,900 per share. Currently, we have not updated our valuation pending FY25 guidance from the management. However, we remain optimistic about EXCL’s prospects, especially as the fixed broadband segment still has significant room for growth, supported by the acquisition of ~750k Link Net subscribers, as we have discussed in our previous report (please see report). We see this segment as having great potential going forward, both in fixed broadband and fixed mobile convergence. Downside risk: potential regulatory hurdles in the merger process and pressure from price competition.

By PHINTRACO SEKURITAS | Research

-Disclaimer On-

.