“MYOR : Increase in Cost of Goods Sold Pressures Net Profit in 1Q25”

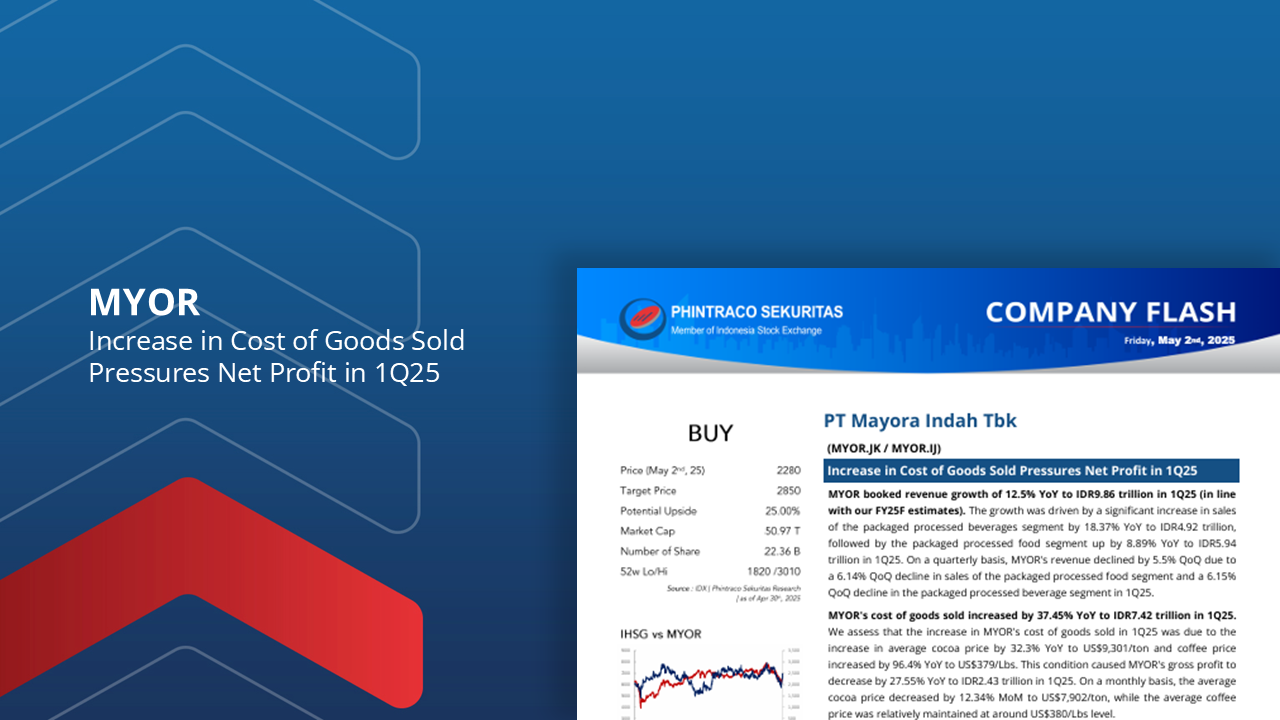

MYOR booked revenue growth of 12.5% YoY to IDR9.86 trillion in 1Q25 (in line with our FY25F estimates). The growth was driven by a significant increase in sales of the packaged processed beverages segment by 18.37% YoY to IDR4.92 trillion, followed by the packaged processed food segment up by 8.89% YoY to IDR5.94 trillion in 1Q25.

MYOR’s cost of goods sold increased by 37.45% YoY to IDR7.42 trillion in 1Q25. We assess that the increase in MYOR’s cost of goods sold in 1Q25 was due to the increase in average cocoa price by 32.3% YoY to US$9,301/ton and coffee price increased by 96.4% YoY to US$379/Lbs. This condition caused MYOR’s gross profit to decrease by 27.55% YoY to IDR2.43 trillion in 1Q25.

MYOR’s net profit decreased by 30% YoY to IDR705 billion in 1Q25. The decrease in net profit was in line with the significant increase in cost of goods sold and operating expenses, which increased 21.74% YoY to IDR1.31 trillion in 1Q25. This condition caused MYOR’s operating profit to decrease by 35.58% YoY to IDR846 billion.

We maintain our Buy rating for MYOR with the same projection and fair value in the previous MYOR company update at IDR2,850 per share. This is in line with MYOR’s revenue growth, which is still in line with our FY25F estimate.