“BBCA : Inline with our estimated, changed to Buy”

BBCA’s interest income grew 8.6% YoY to IDR95 trillion in FY24. This growth was in line with the development of Net Interest Income to IDR82.5 trillion (+12.7% yoY or 1.4% QoQ)

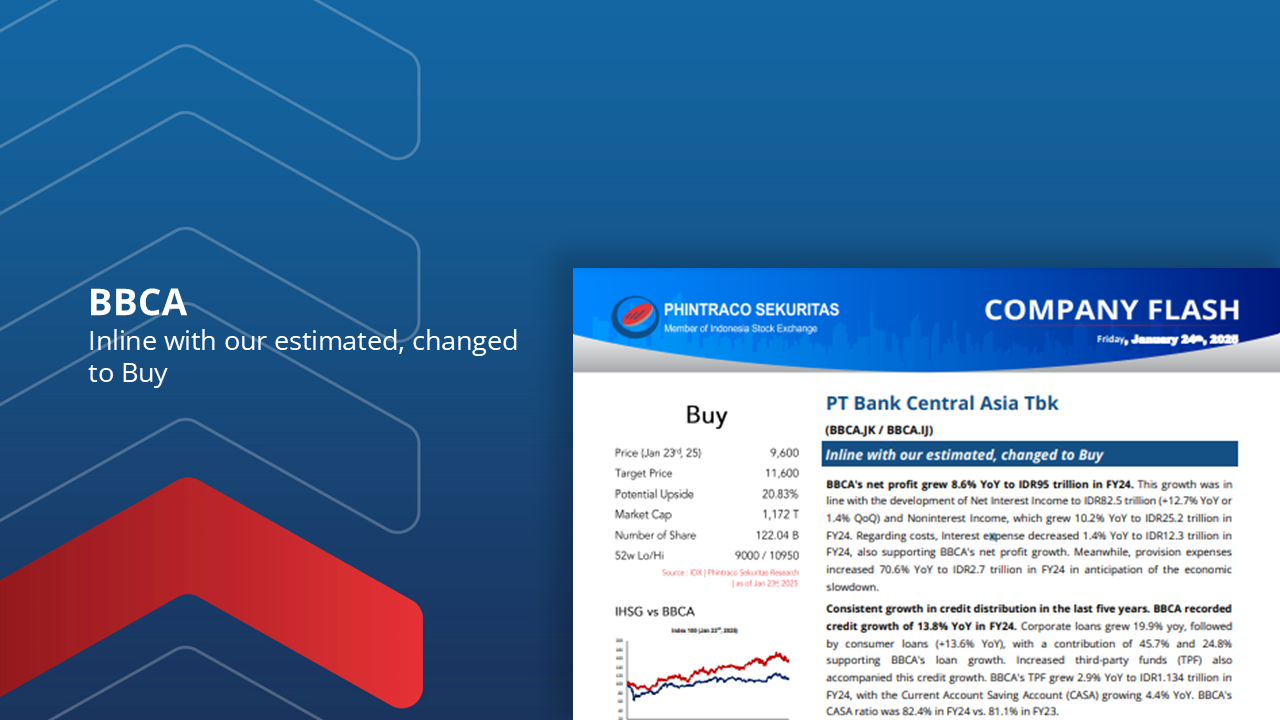

Consistent growth in credit distribution in the last five years. BBCA recorded credit growth of 13.8% YoY in FY24.

Increased third-party funds (TPF) also accompanied this credit growth. BBCA’s TPF grew 2.9% YoY to IDR1.134 trillion in FY24, with the Current Account Saving Account (CASA) growing 4.4% YoY.

BBCA’s gross Non-Performing Loan (NPL) decreased to 1.8% (10 bps YoY; 30 bps QoQ) in FY24.

Thus, with the current price and performance of BBCA shares, we change BBCA’s rating to buy by maintaining the fair value from the previous Company Update at 11,600, so the potential upside becomes 20.83%.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –