“BNGA : Optimize Consumer Loans with Maintained Liquidity”

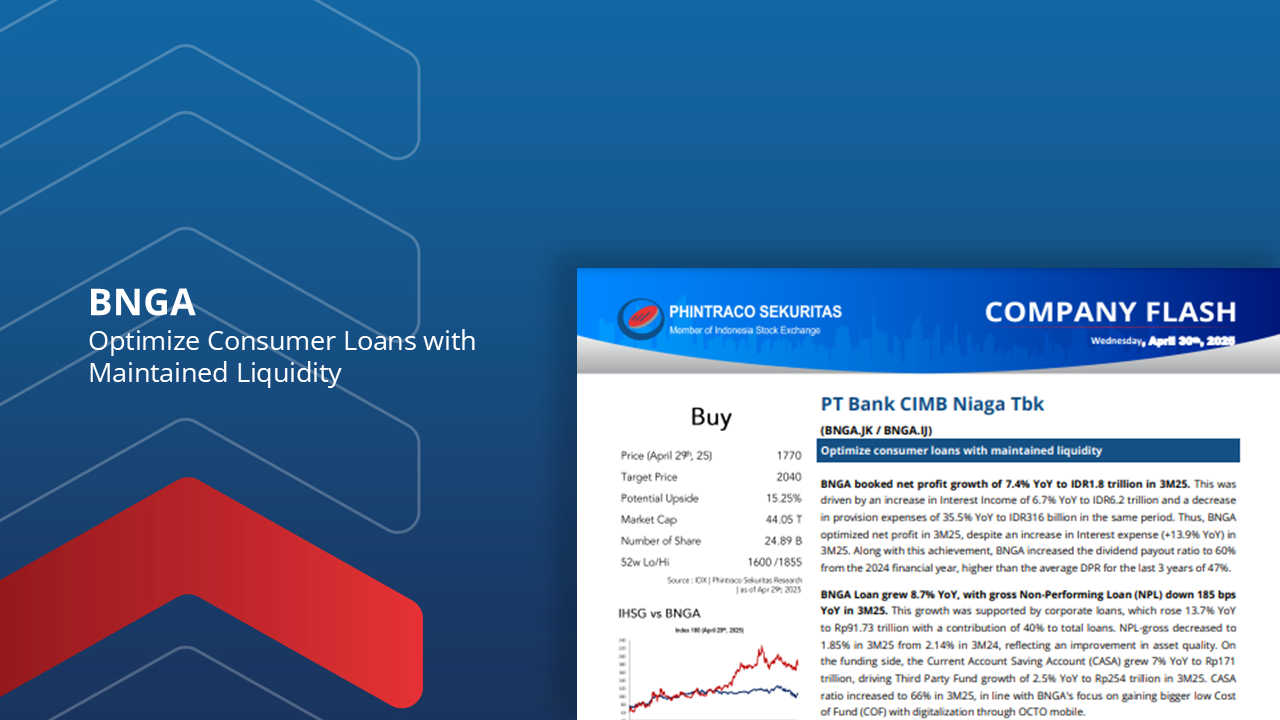

BNGA booked net profit growth of 7.4% YoY to IDR1.8 trillion in 3M25. This was driven by an increase in Interest Income of 6.7% YoY to IDR6.2 trillion and a decrease in provision expenses of 35.5% YoY to IDR316 billion in the same period.

Along with this achievement, BNGA increased the dividend payout ratio to 60% from the 2024 financial year, higher than the average DPR for the last 3 years of 47%.

BNGA Loan grew 8.7% YoY, with gross Non-Performing Loan (NPL) down 185 bps YoY in 3M25. This growth was supported by corporate loans, which rose 13.7% YoY to Rp91.73 trillion with a contribution of 40% to total loans.

CASA ratio increased to 66% in 3M25, in line with BNGA’s focus on gaining bigger low Cost

of Fund (COF) with digitalization through OCTO mobile.

BNGA aims to optimize consumer loans through mortgage loan optimization and OCTO mobile. For the consumer segment, BNGA will optimize mortgage loans by focusing on secondary cities without ignoring big cities (with low Risk-Adjusted Return on Capital).

Therefore, we maintain the Buy rating for BNGA with the same projection and fair value as in the previous BNGA company update, namely 2040, with a potential upside of 15.25%.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –