Cement: Weak Demand and High Capacity Keep Pressure on Margins

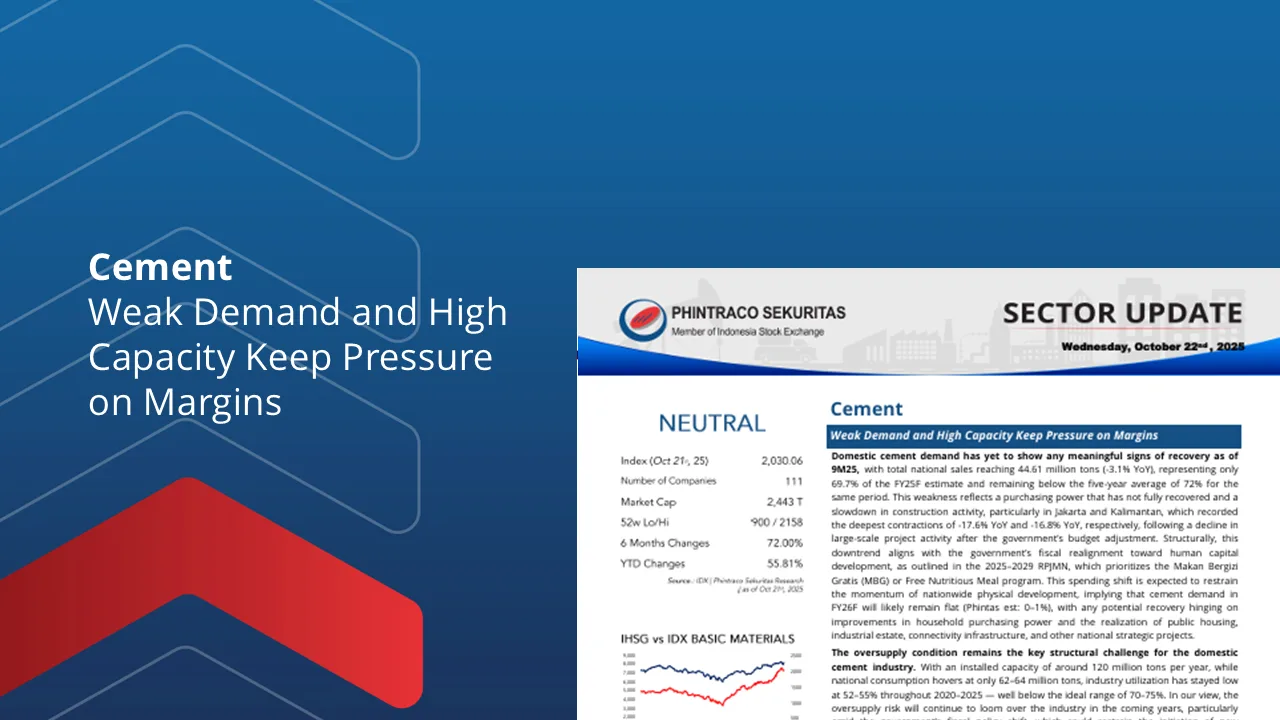

>Domestic cement demand remains sluggish as of 9M25, with total sales of 44.61 mn tons (-3.1% YoY), reflecting only 69.7% of FY25F estimates — below the five-year average of 72%. The slowdown in construction activity, especially in Jakarta (-17.6% YoY) and Kalimantan (-16.8% YoY), reflects weaker purchasing power and the fiscal shift toward human-capital programs under the 2025–2029 RPJMN.

>The structural oversupply issue continues to weigh on the sector, with installed capacity of 120 mn tons versus annual consumption of only 62–64 mn tons, translating to utilization of 52–55%. We expect utilization to hover around 55–58% through FY26F–FY29F, assuming a slow demand recovery, limited new project initiation, and flat FY26F volume growth (Phintas est: 0–1%).

>SMGR recorded 8.44 mn tons (+1.65% QoQ; -3.83% YoY) sales in 3Q25, with market share slipping to 47.9%. INTP posted 5.07 mn tons (+25.6% QoQ; -7.0% YoY) and 13.07 mn tons (-4.5% YoY) in 9M25, maintaining market share at 29.3%. Growth outside Java (+29.4% QoQ) helped offset weakness in Java, but not fully.

>We maintain a Neutral view on the cement sector amid persistent oversupply and muted consumption growth. Operational efficiency remains the main profitability driver. We recommend HOLD INTP with a TP of Rp6,000/share ( EV/EBITDA 4.56x/4.19x FY26F–FY27F ). Potential re-rating may occur if government spending accelerates and bulk cement demand recovers alongside lower energy costs.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –

Contact Us :

WA : 08119560188

IG : phintracosekuritasofficial

YT : Phintraco Sekuritas Official

TELE : phintasprofits

www.phintracosekuritas.com

www.profits.co.id