TLKM : Earnings Normalization in Progress, Structural Upside Intact

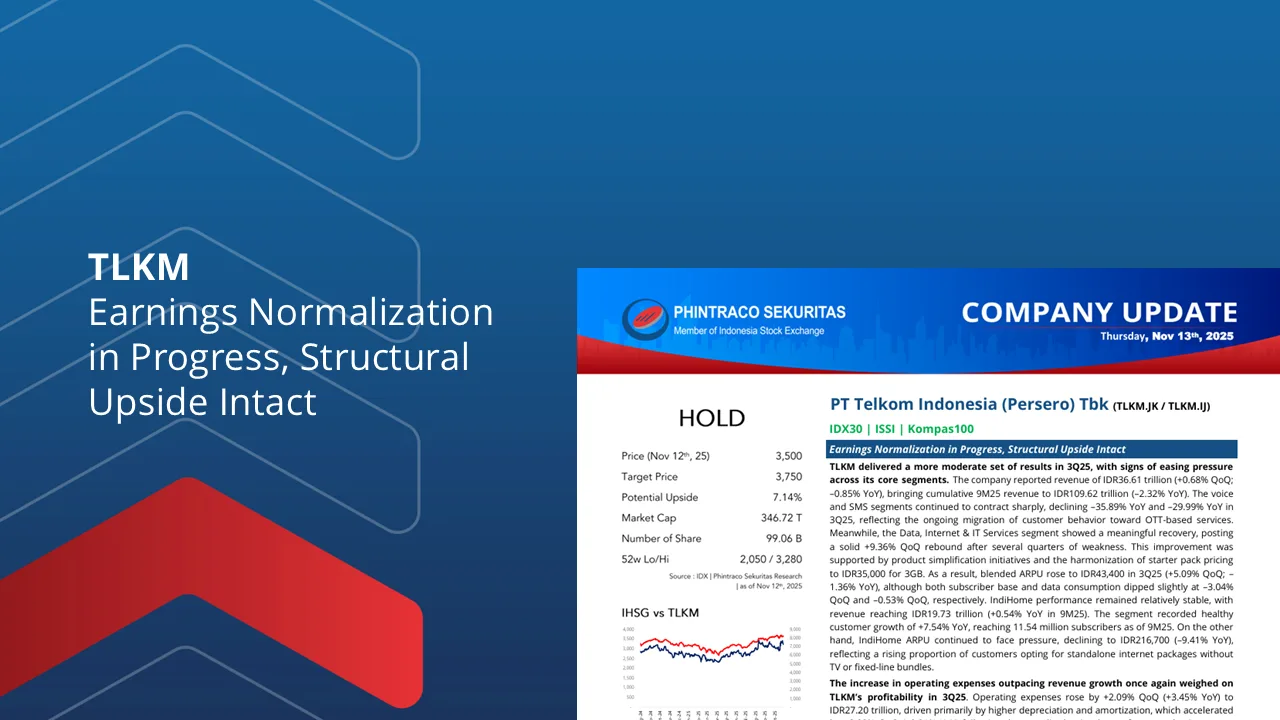

>TLKM delivered a moderate set of results in 3Q25, with topline growth beginning to stabilize. Revenue reached IDR36.61tn (+0.68% QoQ; –0.85% YoY), bringing 9M25 revenue to IDR109.62tn (–2.32% YoY). Legacy segments remained a key drag, with voice and SMS plunging –35.89% YoY and –29.99% YoY, while the Data, Internet & IT Services segment rebounded strongly at +9.4% QoQ following product simplification and harmonized starter pack pricing. Blended ARPU improved to IDR43.4k (+5.1% QoQ), while IndiHome posted steady performance with subscriber growth of +7.5% YoY despite ARPU declining –9.4% YoY as standalone internet plans gained traction.

>Profitability came under pressure as operating expenses rose ahead of revenue. Opex climbed to IDR27.20tn (+2.1% QoQ; +3.5% YoY), driven mainly by higher depreciation and amortization from accelerated asset write-downs. EBITDA reached IDR18.29tn (+2.3% QoQ; –2.5% YoY), with margins inching up to 49.95%, but the improvement was not enough to offset broader cost pressure and non-operating expenses. Net profit softened to IDR4.81tn (–6.9% QoQ; –18.7% YoY), with margin contracting to 13.13% (vs. 16.02% in 3Q24).

>Strategic execution remains intact, with early signs of stronger data monetization supporting gradual recovery. With data contributing ~59% of revenue, continued ARPU uplift will be key to stabilizing earnings. IndiHome provides medium-term potential amidst low fixed broadband penetration, while the planned InfraCo (TIF) spin-off offers long-term value creation through greater infrastructure efficiency and monetization.

>We reiterate our HOLD call on TLKM with a higher TP of IDR3,750 (Prev: IDR2,950), reflecting valuation roll-forward to FY26F. We believe the company’s product simplification initiatives provide a solid foundation for a more sustainable profitability recovery. Additionally, the expansion of fixed broadband services and the planned spin-off of Telkom InfraCo (TIF) are expected to enhance operational efficiency and unlock long-term asset monetization opportunities

>Upside risks include: (1) stronger-than-expected ARPU improvement, (2) faster broadband traction, and (3) accelerated value crystallization from the InfraCo spin-off.

By PHINTRACO SEKURITAS | Research

— Disclaimer On —

Contact Us:

WA: 08119055611

IG: phintracosekuritasofficial

YT: Phintraco Sekuritas Official

TELE: phintasprofits

www.phintracosekuritas.com

www.profits.co.id