JPFA: Expansion to Strengthen Position in the Industry

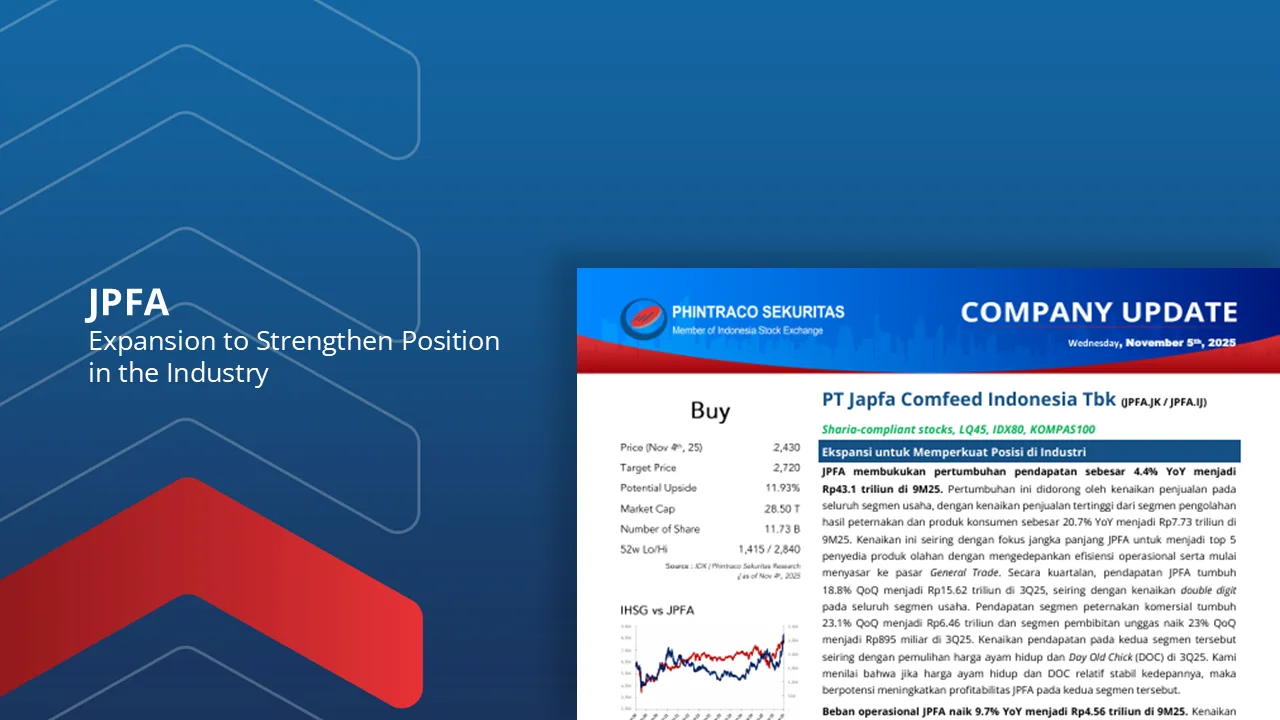

JPFA booked revenue growth of 4.4% YoY to IDR43.1 trillion in 9M25. This growth was driven by increased sales across all business segments, with the highest sales increase from the poultry processing and consumer products segment of 20.7% YoY to IDR7.73 trillion in 9M25.

JPFA’s operating expenses increased by 9.7% YoY to IDR4.56 trillion in 9M25. This increase was due to an increase in sales and distribution expenses of 24.3% YoY to IDR1.91 trillion, as well as general and administrative expenses increased by 9.9% YoY to IDR2.73 trillion in 9M25. Despite the increase in operating expenses, JPFA’s operating profit still grew by 7.7% YoY to IDR3.92 trillion in 9M25.

JPFA’s net profit grew 17.3% YoY to IDR2.63 trillion in 9M25. This growth was supported by an increase in revenue and operating profit in 9M25. In addition, net profit was also driven by better non-operating performance.

During 2025, JPFA has undertaken various strategic initiatives, including increasing animal feed capacity in Makassar, developing aquaculture animal feed in Lamongan, and strengthening the downstream integration of the Poultry Slaughterhouse (RPHU) located in Pemalang.

We maintain our Buy recommendation for JPFA with a higher target price of IDR2,720/share (previous IDR2,400). This recommendation is based on calculations using the Discounted Cash Flow method with a Required Return of 9.83% and a Terminal Growth of 2.64%.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –