“PGAS: Revenue meets estimates, higher supplier prices weigh on profits”

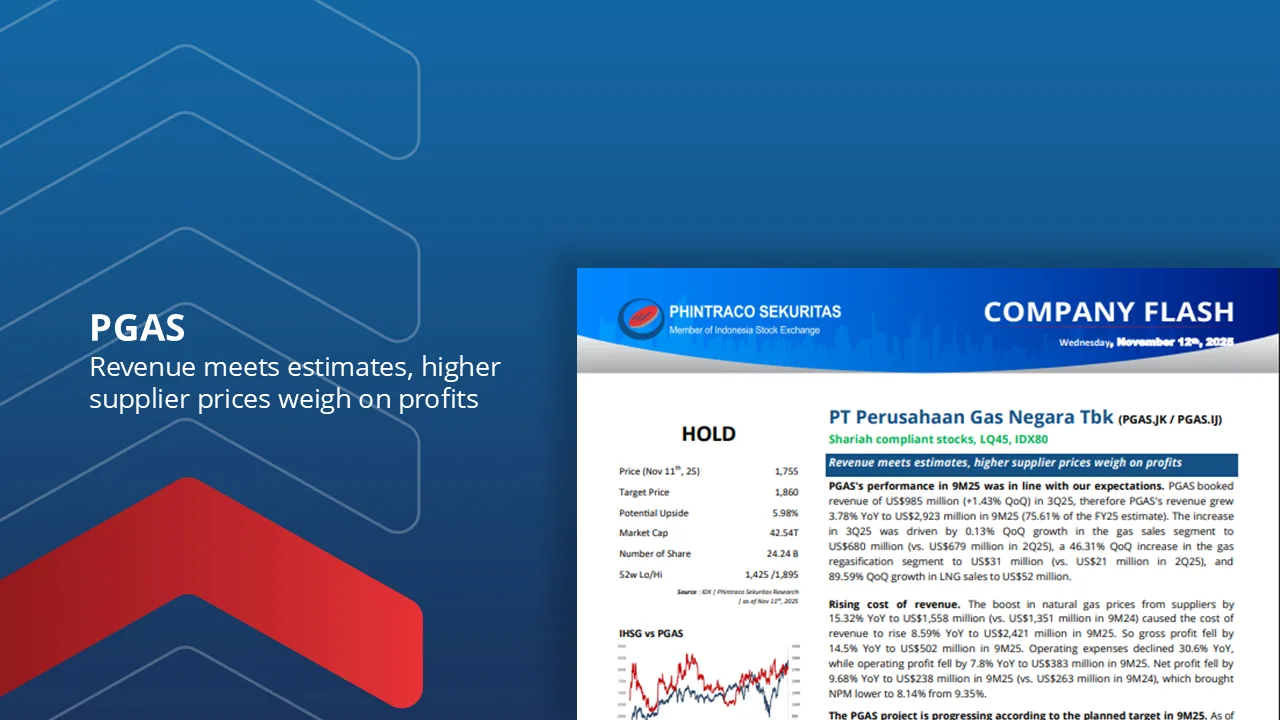

PGAS’s performance in 9M25 was in line with our expectations. PGAS booked revenue of US$985 million

(+1.43% QoQ) in 3Q25, therefore PGAS’s revenue grew 3.78% YoY to US$2,923 million in 9M25 (75.61% of the FY25 estimate).

Rising cost of revenue. The boost in natural gas prices from suppliers by

15.32% YoY to US$1,558 million (vs. US$1,351 million in 9M24) caused the cost of revenue to rise 8.59% YoY to US$2,421 million in 9M25.

Net profit fell by 9.68% YoY to US$238 million in 9M25 (vs. US$263 million in 9M24), which brought NPM lower to 8.14% from 9.35%.

The PGAS project is progressing according to the planned target in 9M25. As of 9M25, the oil transportation project has begun to progress towards the Engineering, Procurement, and Construction (EPC) stage, with a focus on welding.

We changed our recommendation from Buy to Hold, with the same fair value as in the initiate report at Rp1,860/saham.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –