“INTP : Margins Defended Amid Weak Market Conditions”

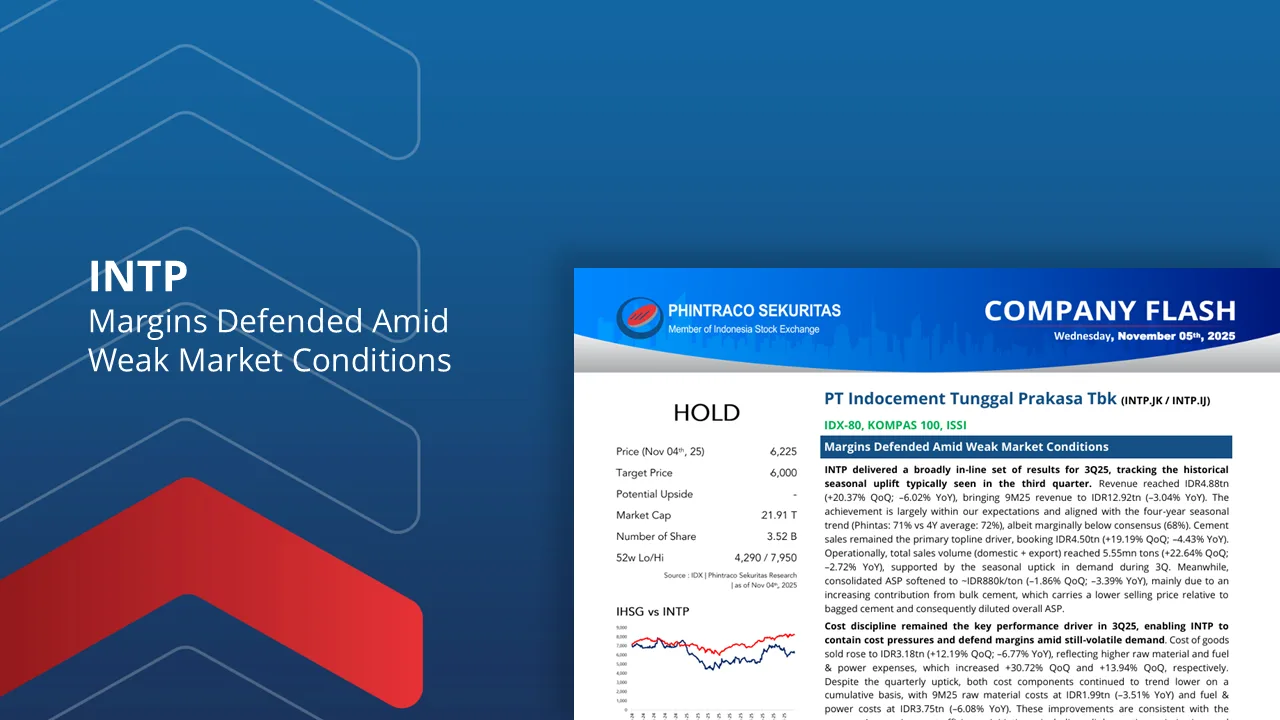

INTP delivered a broadly in-line set of results for 3Q25, supported by the historical seasonal uplift typically seen in the third quarter. Revenue reached IDR4.88tn (+20.37% QoQ; –6.02% YoY), bringing 9M25 revenue to IDR12.92tn (–3.04% YoY). The achievement is largely within our expectations and aligned with the four-year seasonal trend (Phintas: 71% vs 4Y average: 72%), albeit marginally below consensus at 68%. Cement sales remained the primary topline driver, booking IDR4.50tn (+19.19% QoQ; –4.43% YoY). Operationally, total sales volume (domestic + export) reached 5.55mn tons (+22.64% QoQ; –2.72% YoY), supported by seasonal demand recovery. Meanwhile, consolidated ASP softened to ~IDR880k/ton (–1.86% QoQ; –3.39% YoY), mainly due to higher contribution from bulk cement, which carries a lower selling price relative to bagged cement and consequently diluted overall ASP.

Cost discipline remained the key performance driver in 3Q25, enabling INTP to contain cost pressures and defend margins amid still-volatile demand. COGS rose to IDR3.18tn (+12.19% QoQ; –6.77% YoY), reflecting higher raw material and fuel & power expenses (+30.72% QoQ and +13.94% QoQ, respectively). Despite the quarterly uptick, both cost components trended lower on a cumulative basis, with 9M25 raw material costs at IDR1.99tn (–3.51% YoY) and fuel & power costs at IDR3.75tn (–6.08% YoY). These improvements align with INTP’s ongoing cost-efficiency initiatives, particularly clinker ratio optimization and increased RDF utilization. Supported by seasonal demand recovery and cost optimization, INTP reported EBITDA of IDR1.12tn (+51.88% QoQ; –6.71% YoY) in 3Q25. Net profit grew significantly to IDR568bn (+100.06% QoQ; –8.51% YoY), bringing 9M25 net income to IDR1.06tn (+0.68% YoY) and driving NPM higher to 8.23% (vs 7.93% in 9M24).

We view INTP’s 2025 performance as likely to remain within expectations, with sector demand yet to reflect any meaningful inflection. The lack of near-term catalysts — including delayed infrastructure project execution and a transitional government spending cycle — renders 2025 a challenging year for the sector. Looking into 2026, we expect national cement sales growth to remain soft at ~0–1% YoY amid muted demand and persistent oversupply. Our stance could turn more constructive should government infrastructure spending resume at scale, particularly for physical development projects, which historically serve as a key sector demand driver. In the interim, INTP’s disciplined pricing strategy, clinker ratio optimization, and RDF expansion remain crucial to safeguarding profitability.

We downgrade INTP from BUY to HOLD, and revise our target price to IDR6,000 (Prev: IDR6,500) following our valuation roll-forward to FY26F. The downgrade reflects prolonged oversupply, subdued demand, and a continued wait-and-see stance on infrastructure execution — limiting the potential for a meaningful re-rating in the near term. Nonetheless, we positively note INTP’s progress in accelerating RDF usage, which not only enhances cost efficiency but also strengthens its sustainability positioning. Upside risks to our call include: 1) Faster execution of government and private infrastructure projects, potentially lifting demand sooner than expected, and 2) a more aggressive shift toward RDF and alternative fuels that could unlock additional cost savings beyond our baseline assumptions.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –

Contact Us:

WA: 08119055611

IG: phintracosekuritasofficial

YT: Phintraco Sekuritas Official

TELE: phintasprofits

www.phintracosekuritas.com

www.profits.co.id