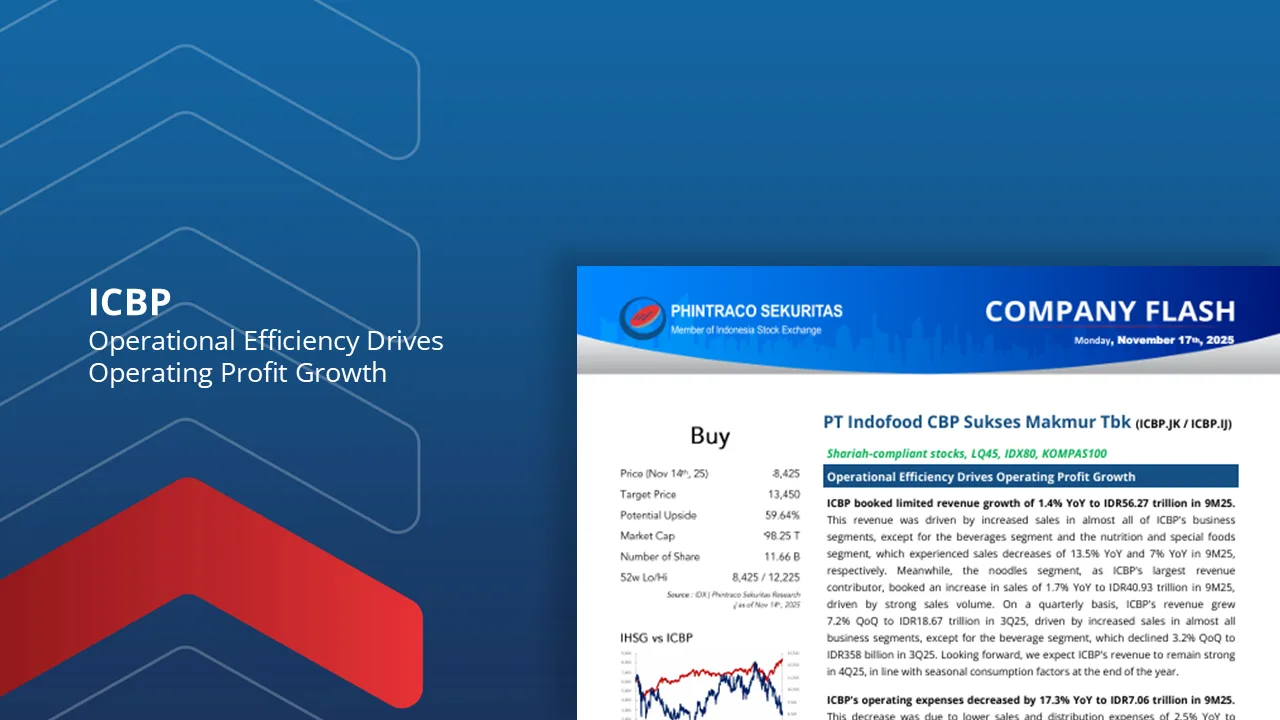

“ICBP: Operational Efficiency Drives Operating Profit Growth”

ICBP booked limited revenue growth of 1.4% YoY to IDR56.27 trillion in 9M25. This revenue was driven by increased sales in almost all of ICBP’s business segments, except for the beverages segment and the nutrition and special foods segment, which experienced sales decreases of 13.5% YoY and 7% YoY in 9M25, respectively.

Meanwhile, the noodles segment, as ICBP’s largest revenue contributor, booked an increase in sales of 1.7% YoY to IDR40.93 trillion in 9M25, driven by strong sales volume.

ICBP’s operating expenses decreased by 17.3% YoY to IDR7.06 trillion in 9M25. This condition caused operating profit to grow 6.2% YoY to IDR12.74 trillion in 9M25.

ICBP’s net profit decreased by 12.6% YoY to IDR8.19 trillion in 9M25. This decrease was mainly due to an increase in financial expenses to IDR3.01 trillion in 9M25 due to foreign exchange losses from financing activities of IDR1.43 trillion.

Therefore, we maintain our Buy rating for ICBP with the same projections and fair value as in the previous company update at IDR13,450.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –