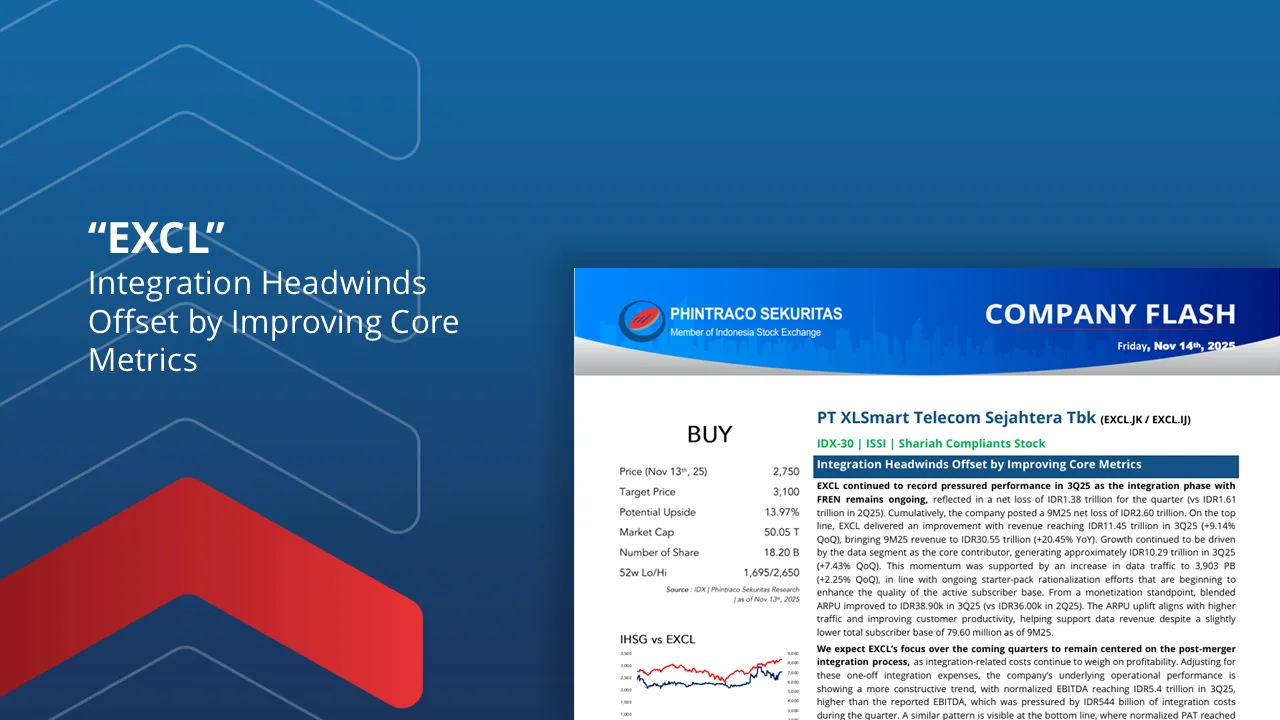

“EXCL : Integration Headwinds Offset by Improving Core Metrics”

>EXCL continued to record pressured performance in 3Q25, as the integration phase with FREN remains ongoing. The company booked a net loss of IDR1.38tn for the quarter (vs IDR1.61tn in 2Q25), bringing 9M25 net loss to IDR2.60tn. On the topline, EXCL delivered sequential improvement with 3Q25 revenue reaching IDR11.45tn (+9.14% QoQ), driving 9M25 revenue to IDR30.55tn (+20.45% YoY). Growth remained anchored by the data segment, which contributed IDR10.29tn (+7.43% QoQ), supported by rising data traffic of 3,903 PB (+2.25% QoQ) and early impacts from starter-pack rationalization that is beginning to lift active customer quality. Blended ARPU increased to IDR38.90k (vs IDR36.00k in 2Q25), reflecting improved customer productivity despite a slightly lower total subscriber base of 79.60mn as of 9M25.

>Profitability remained under pressure as integration-related expenses continued to weigh on operating performance. Adjusting for >these one-off items, underlying trends showed a more constructive picture, with normalized EBITDA rising to IDR5.4tn in 3Q25, compared to reported EBITDA that was held back by IDR544bn of integration costs. A similar divergence was seen in earnings, where normalized PAT reached IDR1.15tn, contrasting sharply with reported net losses driven by integration expenses, accelerated depreciation, and asset impairments. Higher D&A primarily reflected the accelerated amortization of the 900 MHz spectrum (to be returned to Komdigi in FY26) and the accelerated depreciation of legacy equipment following vendor migration. Despite near-term pressures, management remains committed to distributing dividends this year, implying a 1.32% dividend yield based on the 3-year average payout ratio (~41%). However, dividend capacity may be more constrained going forward as integration continues.

>Execution on strategic priorities remains intact, with management outlining three key growth pillars: Mobile, Enterprise, and Home. Across its XL, Axis, and Smartfren brands, EXCL aims to enhance service quality through product simplification and higher digital ecosystem engagement, supported by greater usage across MyXL, MySmartfren, and Axisnet. In enterprise, EXCL continues expanding its position as a preferred ICT partner via ESTA (Enterprise Smart Technology & Automation)—a comprehensive platform offering connectivity, IoT, cloud solutions, cybersecurity, and automation capabilities. In Home Broadband, EXCL is strengthening its positioning as one of Indonesia’s leading fixed broadband providers by enhancing customer experience and flexibility, with XL Satu expected to drive stronger loyalty and deeper household penetration. These initiatives, alongside improving customer quality and the unwinding of integration-related costs, form the foundation for EXCL’s medium-term recovery outlook.

>We maintain our BUY recommendation on EXCL with a TP of IDR3,100. While the company continues to face near-term earnings pressure, we view the weakness as temporary and largely attributable to ongoing integration. We remain constructive on EXCL’s outlook, supported by rising data traffic, improving customer quality, and stabilizing ARPU trends. In our view, the strengthening of EXCL’s three growth pillars will be instrumental in driving operational improvements post-integration. Downside risks include (1) slower-than-expected integration progress, delaying synergy realization, and (2) intensified pricing pressure that could hinder monetization.

By PHINTRACO SEKURITAS | Research

— Disclaimer On —

Contact Us:

WA: 08119055611

IG: phintracosekuritasofficial

YT: Phintraco Sekuritas Official

TELE: phintasprofits

www.phintracosekuritas.com

www.profits.co.id