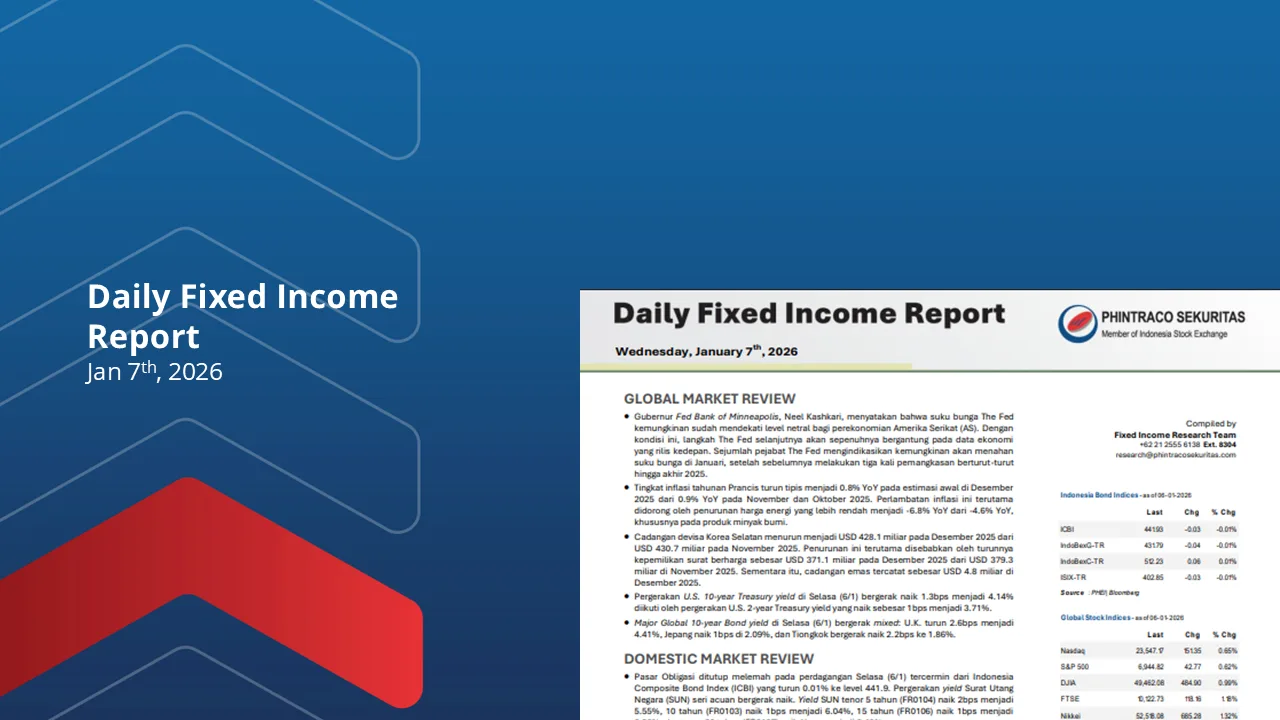

Daily Fixed Income Report – 7 January 2026

Gubernur Fed Bank of Minneapolis, Neel Kashkari, menyatakan bahwa suku bunga The Fed kemungkinan sudah mendekati level netral bagi perekonomian Amerika Serikat (AS). Dengan kondisi ini, langkah The Fed selanjutnya...

Baca Laporan

Daily Fixed Income Report – 30 Desember 2025

Dallas Fed Manufacturing Index di AS turun 0.5 poin menjadi -10.9 pada Desember 2025 terendah sejak Juni sementara indeks prospek bisnis merosot ke -11.9, mencerminkan pelemahan luas di produksi (-3.2),...

Baca Laporan

Daily Fixed Income Report – 24 Desember 2024

Pertumbuhan ekonomi AS tumbuh kuat sebesar 4.3% YoY di estimasi kedua pada 3Q25, naik dari 3.8% YoY di 2Q25 dan melampaui perkiraan pasar 3.3% YoY, didorong terutama oleh kenaikan konsumsi...

Baca Laporan

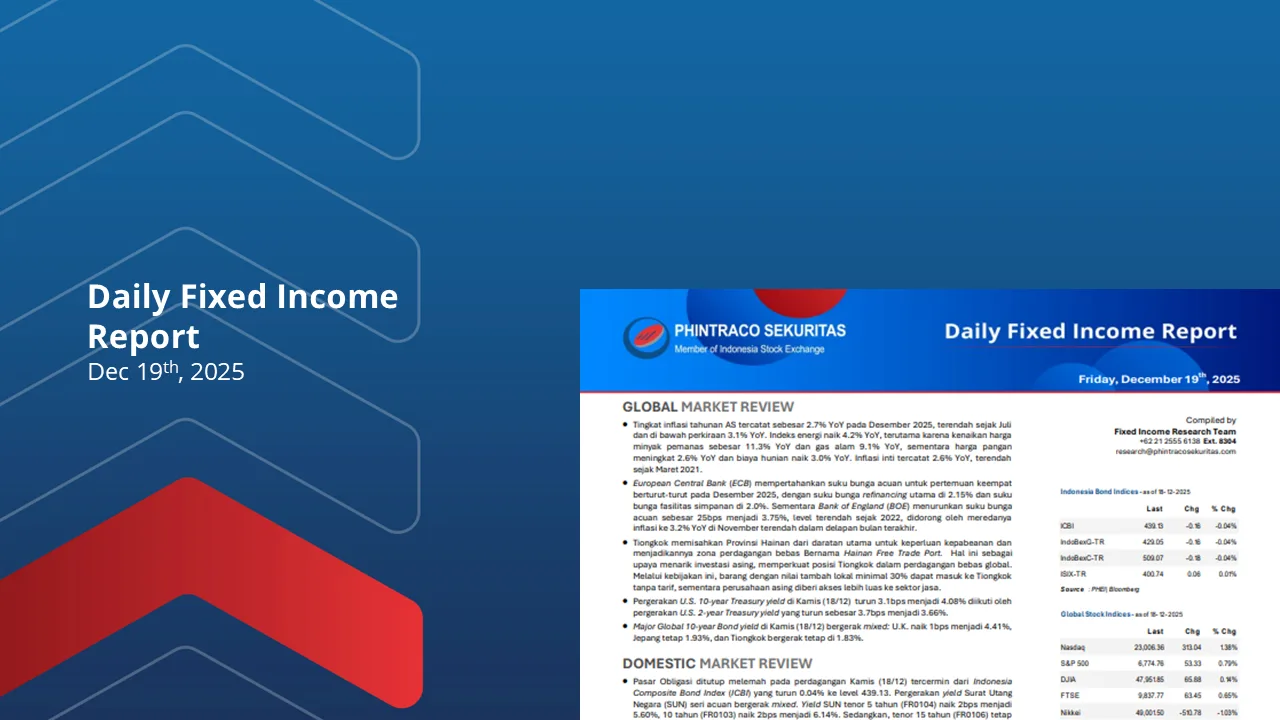

Daily Fixed Income Report – 19 Desember 2025

Tingkat inflasi tahunan AS tercatat sebesar 2.7% YoY pada Desember 2025, terendah sejak Juli dan di bawah perkiraan 3.1% YoY. Indeks energi naik 4.2% YoY, terutama karena kenaikan harga minyak...

Baca Laporan

Diperkirakan IHSG berpotensi menguji support 8550-8600

Indeks di Wall Street ditutup mixed pada Kamis (11/12). Indeks Dow Jones dan indeks S&P500 menguat mencapai level tertinggi baru. Nasdaq Composite ditutup melemah akibat koreksi pada saham Oracle. The...

Baca Laporan

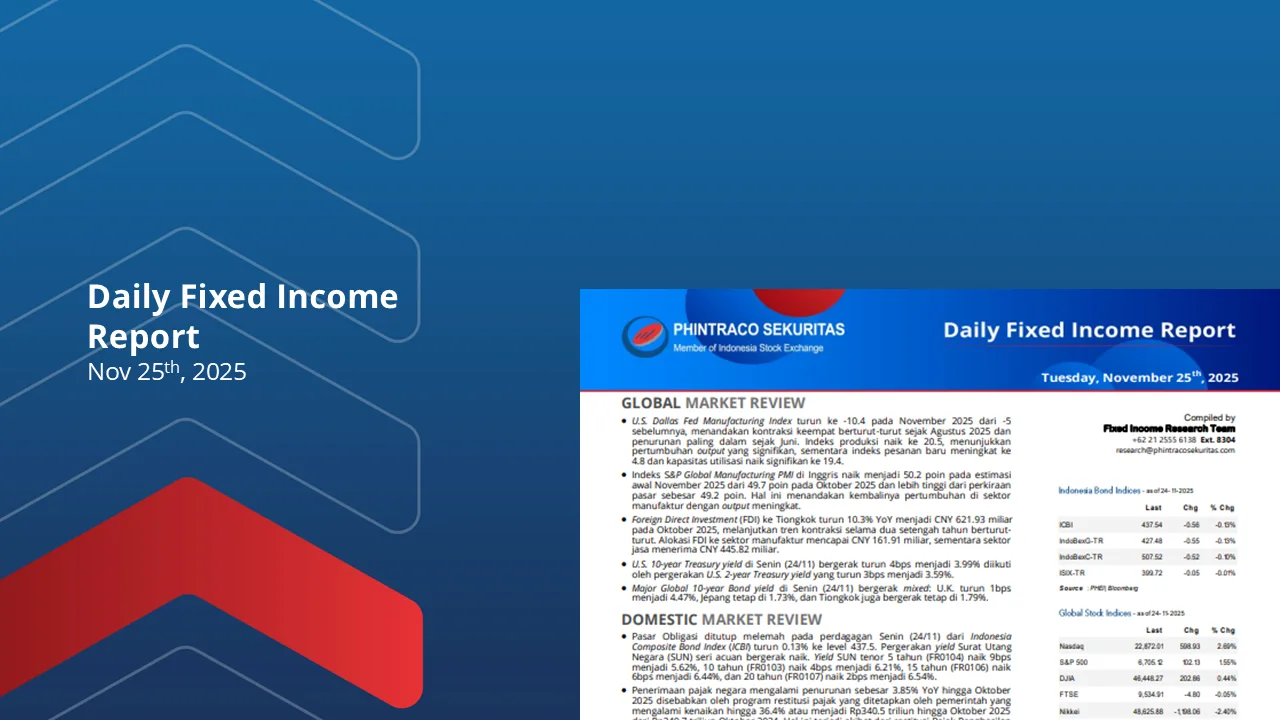

Daily Fixed Income Report – 25 November 2025

U.S. Dallas Fed Manufacturing Index turun ke -10.4 pada November 2025 dari -5 sebelumnya, menandakan kontraksi keempat berturut-turut sejak Agustus 2025 dan penurunan paling dalam sejak Juni. Indeks produksi naik...

Baca Laporan

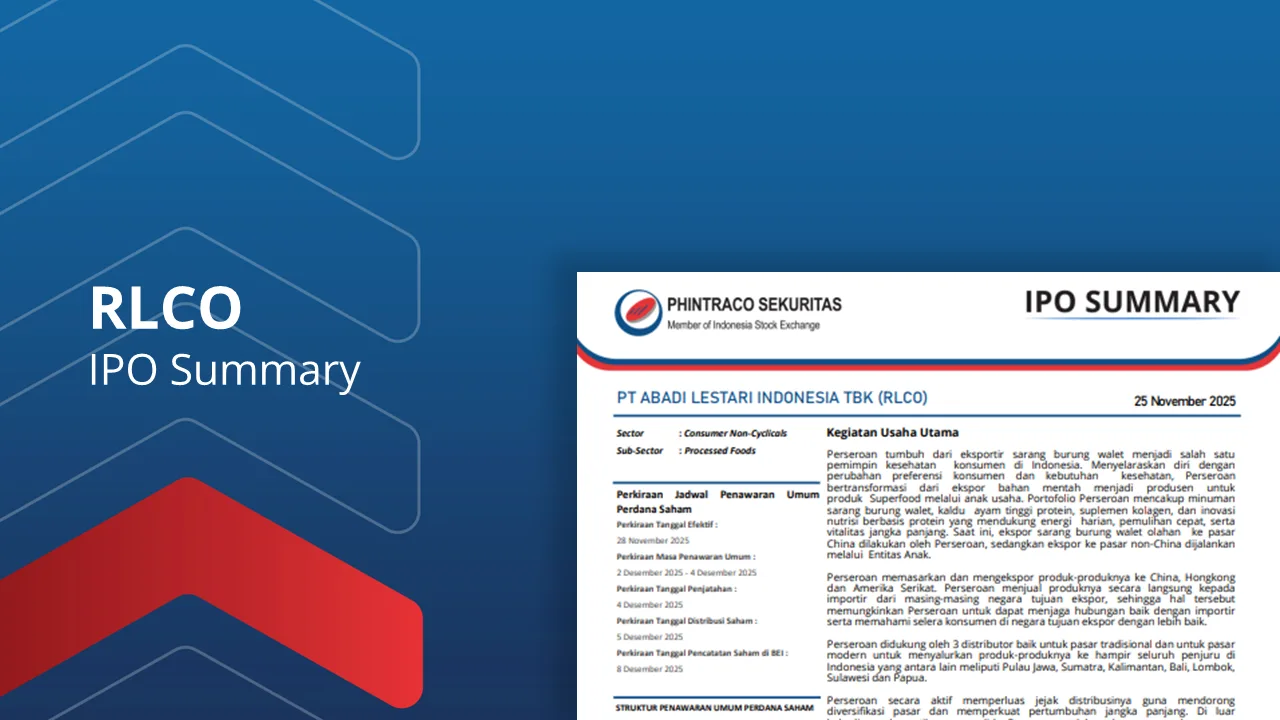

PT Abadi Lestari Indonesia Tbk (RLCO)

Code : RLCO Sector : Consumer Non-Cyclicals Sub-Sector : Processed Foods --------------------------------------------- PERKIRAAN JADWAL PENAWARAN UMUM PERDANA SAHAM Perkiraan Tanggal Efektif : 28 November 2025 Perkiraan Masa Penawaran Umum :...

Baca Laporan

Weekly Fixed Income Report – 24 November 2025

Tingkat pengangguran AS naik menjadi 4.4% pada September 2025 dari 4.3% di Agustus 2025, lebih tinggi dari ekspektasi pasar sebesar 4.3% dan merupakan level tertinggi sejak Oktober 2021. Jumlah penganggur...

Baca Laporan