MBMA: Solid Operations and Downstream Milestone Progress

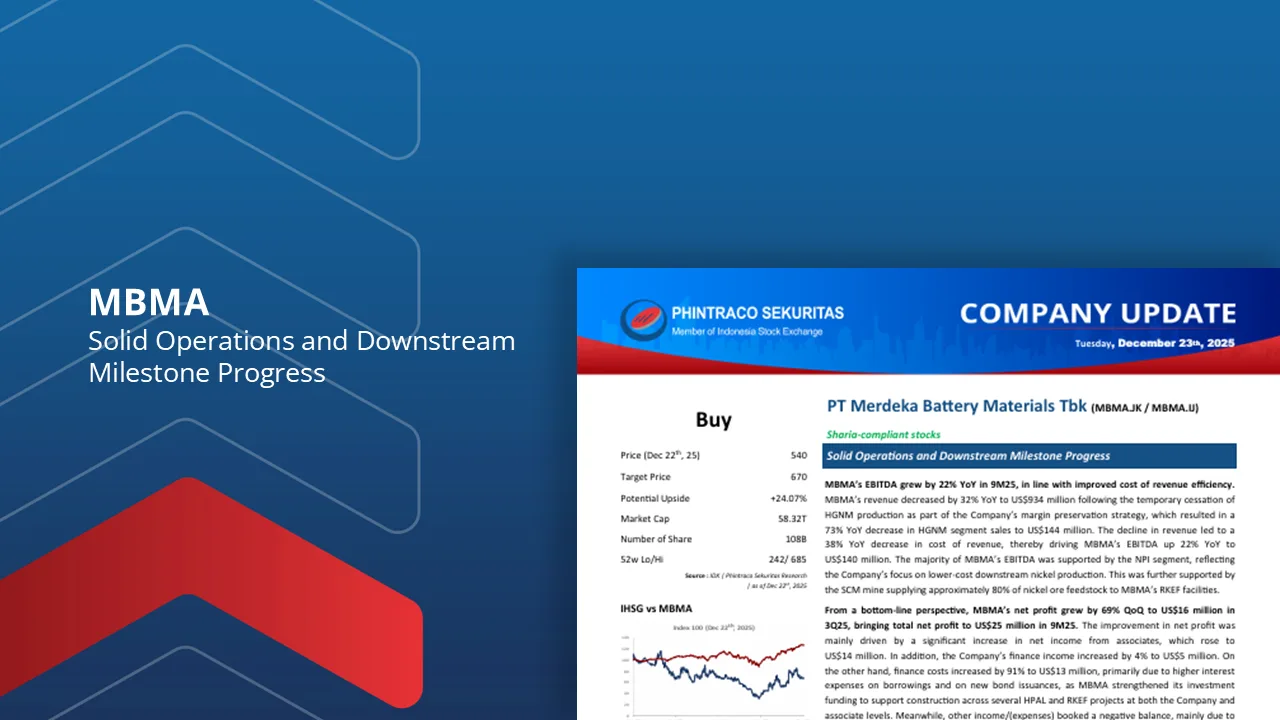

MBMA’s EBITDA grew by 22% YoY in 9M25, in line with improved cost of revenue efficiency. The majority of MBMA’s EBITDA was supported by the NPI segment, reflecting the Company’s focus on lower-cost downstream nickel production.

From a bottom-line perspective, MBMA’s net profit grew by 69% QoQ to US$16 million in 3Q25, bringing total net profit to US$25 million in 9M25. The improvement in net profit was mainly driven by a significant increase in net income from associates, which rose to US$14 million.

MBMA delivered solid operational performance while managing cash costs. Saprolite and limonite ore production was recorded at 4.5 million and 9.9 million wmt in 9M25, with the majority sourced from the SCM nickel mine.

MBMA continues to unlock new opportunities through its AIM and HPAL plants. Commissioning of the AIM plant progressed smoothly, with acid production reaching 251,715 tonnes, alongside initial output from the chloride unit comprising 48,228 tonnes of iron pellets, 464 tonnes of copper sponge, and 7.3 tonnes of gold mud.

Using the Sum of the Parts method, we estimate MBMA’s fair value at p670/share (26.2x Expected EV/EBITDA FY25F, Terminal Growth of 1.46%, and Required Return of 8.58%), higher than the previous Rp525/share. Considering MBMA’s fair price and performance, we assign a Buy rating to MBMA with a potential upside of 24.07%.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –

Contact Us :

WA : 08119560188

IG : phintracosekuritasofficial

YT : Phintraco Sekuritas Official

TELE : phintasprofits

www.phintracosekuritas.com

www.profits.co.id