INCO: Navigating Price Volatility with Efficiency and Downstreaming

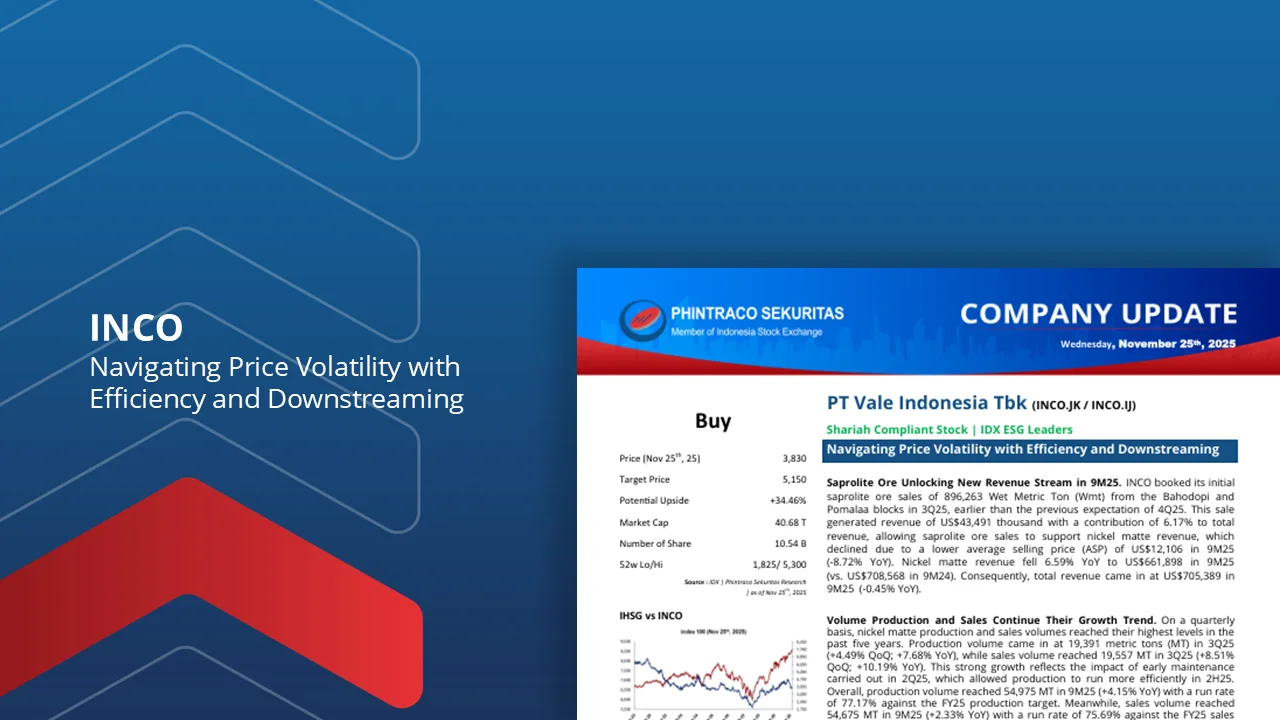

Saprolite Ore Unlocking New Revenue Stream in 9M25. INCO booked its initial saprolite ore sales of 896,263 Wet Metric Ton (Wmt) from the Bahodopi and Pomalaa blocks in 3Q25, earlier than the previous expectation of 4Q25. This sale generated revenue of US$43,491 thousand with a contribution of 6.17% to total revenue, allowing saprolite ore sales to support nickel matte revenue, which declined due to a lower average selling price (ASP) of US$12,106 in 9M25 (-8.72% YoY).

Volume Production and Sales Continue Their Growth Trend. On a quarterly basis, nickel matte production and sales volumes reached their highest levels in the past five years. Production volume came in at 19,391 metric tons (MT) in 3Q25 (+4.49% QoQ; +7.68% YoY), while sales volume reached 19,557 MT in 3Q25 (+8.51% QoQ; +10.19% YoY).

Fuel Oil and Coal Efficiency. Operational efficiency, especially in energy consumption costs, continues to be prioritized as production activity increases. Fuel oil and lubricant expenses fell 7.20% YoY to US$138,535 in 9M25 (vs. US$149,288 in 9M24), while coal fuel expenses reached US$52,746 thousand in 9M25 (-10.70% YoY).

CAPEX Realization Supporting Long Term Growth. INCO continues to invest in projects that will strengthen future operations. As of 9M25, CAPEX realization reached US$331.4 million, up 64.96% YoY (vs. US$200.9 million in 9M24). This CAPEX allocation is aimed at accelerating the progress of the Bahodopi and Pomalaa mine execution projects.

Using the Sum-of-the-Parts (SOTP) method, we raise our fair value estimate for INCO to Rp5,150 (from previously Rp3,560) and maintain a Buy recommendation with an upside potential of 34.46%.

By PHINTRACO SEKURITAS | Research

* Disclaimer On –