ICBP : Innovation and Efficiency to Drive Performance in FY25

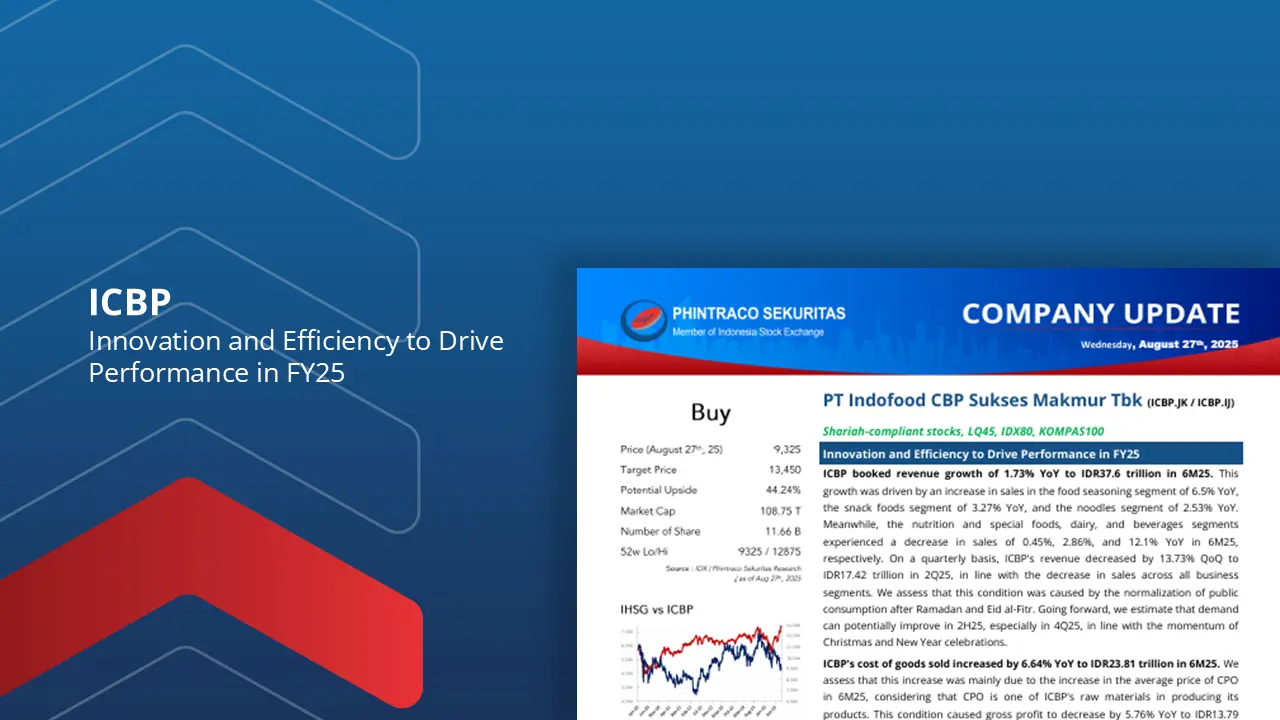

ICBP booked revenue growth of 1.73% YoY to IDR37.6 trillion in 6M25. This growth was driven by an increase in sales in the food seasoning segment of 6.5% YoY, the snack foods segment of 3.27% YoY, and the noodles segment of 2.53% YoY.

On a quarterly basis, ICBP’s revenue decreased by 13.73% QoQ to IDR17.42 trillion in 2Q25, in line with the decrease in sales across all business segments. We assess that this condition was caused by the normalization of public consumption after Ramadan and Eid al-Fitr. Going forward, we estimate that demand can potentially improve in 2H25, especially in 4Q25, in line with the momentum of Christmas and New Year celebrations.

ICBP’s cost of goods sold increased by 6.64% YoY to IDR23.81 trillion in 6M25. We assess that this increase was mainly due to the increase in the average price of CPO in 6M25, considering that CPO is one of ICBP’s raw materials in producing its products. This condition caused gross profit to decrease by 5.76% YoY to IDR13.79 trillion in 6M25.

ICBP’s net profit grew 41.81% YoY to IDR6.2 trillion in 6M25. This growth was driven by a decrease in financial expenses of 66.35% YoY to IDR1.29 trillion in 6M25 due to a decrease in foreign exchange losses from financing activities to IDR227 billion in 6M25 (vs. IDR2.75 trillion in 6M24).

We estimate that ICBP’s net profit has the potential to grow 13.31% YoY to IDR10.36 trillion in FY25F. This estimate is based on the expectation of continued operational efficiency and a stable rupiah exchange rate against the US dollar, which has the potential to decrease financial expenses.

We maintain our Buy Recommendation for ICBP with a higher target price of IDR13,450 per share (previous IDR13,275). This recommendation is based on calculations using the Discounted Cash Flow method with a Required Return of 7.29% and a Terminal Growth of 2.95%.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –