EXCL: New Chapter, New Potential

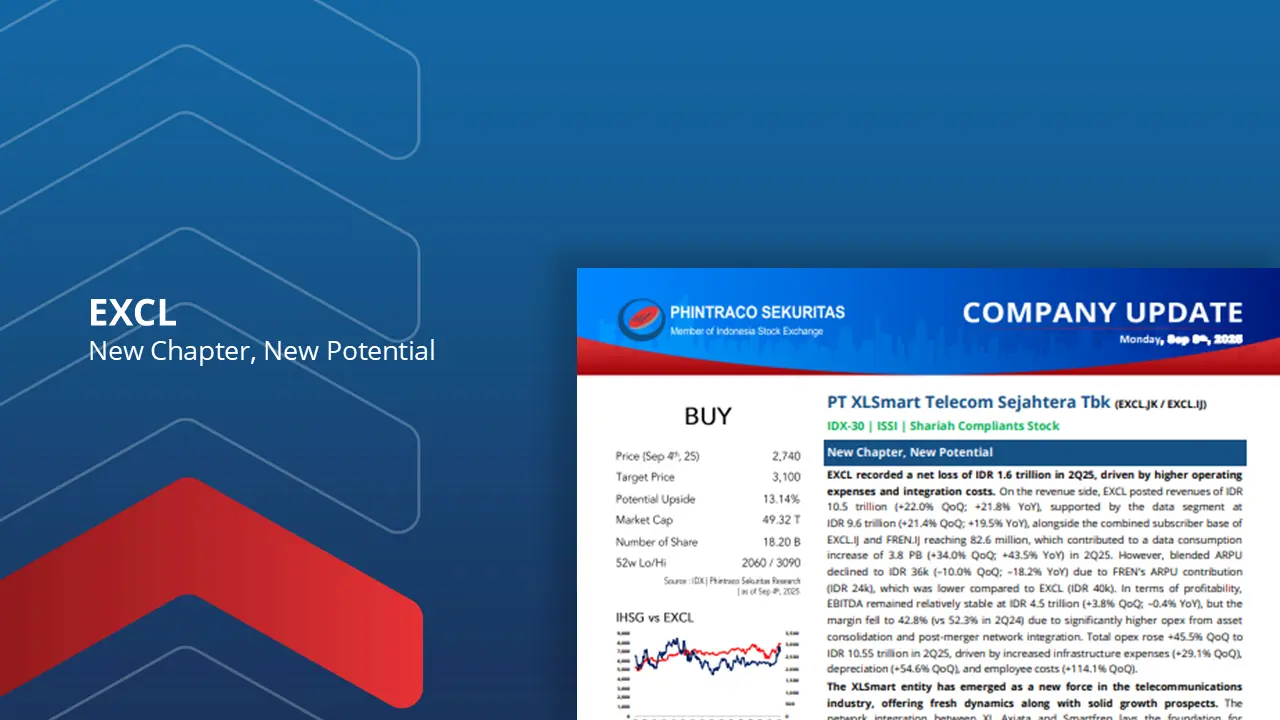

EXCL recorded a net loss of IDR 1.6 trillion in 2Q25, driven by higher operating expenses and integration costs. On the revenue side, EXCL posted IDR 10.5 trillion (+22.0% QoQ; +21.8% YoY), supported by the data segment at IDR 9.6 trillion (+21.4% QoQ; +19.5% YoY). The combined subscriber base of EXCL.IJ and FREN.IJ reached 82.6 million, contributing to a 2Q25 data consumption increase of 3.8 PB (+34.0% QoQ; +43.5% YoY). However, blended ARPU declined to IDR 36k (–10.0% QoQ; –18.2% YoY) due to FREN’s ARPU contribution (IDR 25k in 1Q25), lower than EXCL (IDR 40k in 1Q25).

EBITDA remained relatively stable at IDR 4.5 trillion (+3.8% QoQ; –0.4% YoY), though margin fell to 42.8% (vs 52.3% in 2Q24) as opex rose significantly from asset consolidation and post-merger network integration. Total opex climbed +45.5% QoQ to IDR 10.55 trillion, driven by higher infrastructure costs (+29.1% QoQ), depreciation (+54.6% QoQ), and employee expenses (+114.1% QoQ).

XLSmart has emerged as a new force in the telecom industry, combining XL Axiata and Smartfren’s networks to create a foundation for sustainable growth. The expanded spectrum portfolio and wider coverage now reach 475 cities, including 156 new cities, with 11k BTS activated for Smartfren. Total BTS grew 28% YoY to 209.82k (pre-merger: 163.88k), while 4G BTS increased 39% YoY to 160.34k. The merger is expected to enhance customer experience, improve ARPU, and reinforce EXCL’s position as a leading player with long-term growth potential.

For FY25E, management projects EBITDA margin in the low-to-mid 40% range, reflecting integration costs. Integration costs for 2H25 are guided at IDR 1 trillion, covering network consolidation, tower dismantling, and employee expenses. Total CAPEX is expected at IDR 20 trillion. Gross merger synergies are projected at USD 100–200 million (±IDR 1.6–3.2 trillion), mainly from network consolidation and tower lease savings, creating long-term value for profitability.

We maintain our BUY recommendation on EXCL with a higher target price of Rp3,100/share (prev: Rp2,900), implying EV/EBITDA of 6.35x/5.92x for FY25E/FY26F. We remain optimistic about post-merger prospects as synergies gradually materialize, although integration challenges remain. By comparison, the ISAT-Hutch merger showed flat performance 2–3 years post-merger, though EBITDA improved in the second year as cost structures normalized.

Downside Risks: slower-than-expected traffic growth and longer-than-anticipated network integration.

By PHINTRACO SEKURITAS | Research

–Disclaimer On–