“TLKM: Margin Pressure Amid Weak Consumer Spending”

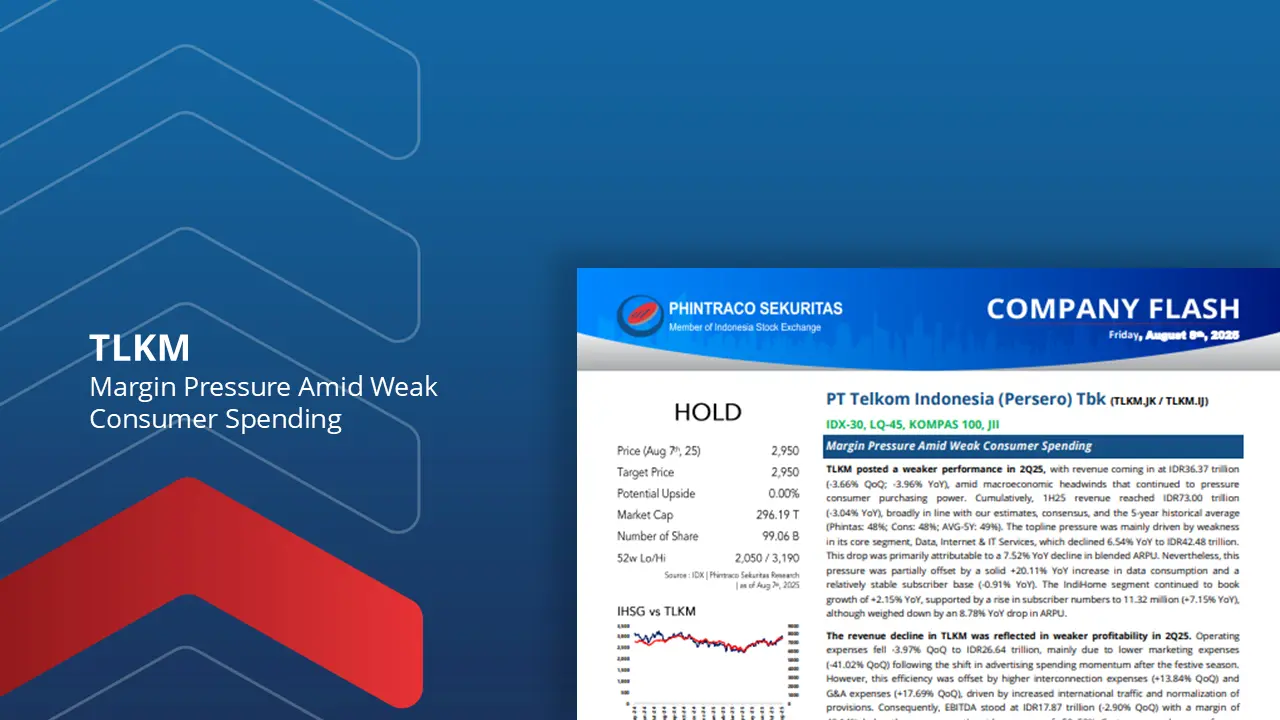

TLKM posted a weaker performance in 2Q25, with revenue coming in at IDR36.37 trillion (–3.66% QoQ; –3.96% YoY), amid macroeconomic headwinds that continued to pressure consumer purchasing power. Cumulatively, 1H25 revenue reached IDR73.00 trillion (–3.04% YoY), broadly in line with our estimates, consensus, and the 5-year historical average (Phintas: 48%; Cons: 48%; 5Y Avg: 49%). The topline pressure was mainly driven by weakness in its core segment, Data, Internet & IT Services, which declined 6.54% YoY to IDR42.48 trillion, primarily due to a 7.52% YoY drop in blended ARPU. This was partly offset by a solid +20.11% YoY growth in data consumption and a relatively stable subscriber base (–0.91% YoY). Meanwhile, IndiHome booked +2.15% YoY revenue growth, supported by subscriber growth to 11.32 million (+7.15% YoY), though weighed down by an 8.78% YoY ARPU decline.

The revenue decline was mirrored in weaker profitability. Operating expenses fell –3.97% QoQ to IDR26.64 trillion, mainly from lower marketing costs (–41.02% QoQ) following the post-festive season shift in advertising spend. However, this was offset by higher interconnection expenses (+13.84% QoQ) and G&A expenses (+17.69% QoQ), driven by increased international traffic and normalization of provisions. Consequently, EBITDA fell to IDR17.87 trillion (–2.90% QoQ) with a margin of 49.14%, below management’s ~50–52% guidance. Additional cost pressure came from O&M expenses (+5.70% QoQ) due to network expansion, while personnel expenses declined –5.80% QoQ, reflecting benefits from last year’s early retirement program (ERP) and adjustments to employee tax expenses in the prior quarter. Net profit dropped to IDR5.17 trillion (–13.54% QoQ), with NPM at 14.20% (vs. 15.83% in 1Q25). Cumulatively, 1H25 net profit reached IDR10.98 trillion (–6.68% YoY), broadly in line with our and consensus estimates, but below the 5-year average (Phintas: 49%; Cons: 48%; 5Y Avg: 54%).

Management revised down its FY25 guidance, with revenue growth now projected to be flat (vs. previous low single-digit growth expectation). The FY25 EBITDA margin target was also lowered to 50% (prev: 50–52%), reflecting expectations that consumer purchasing power will not improve significantly. A recovery in 2H25F is anticipated, supported by a total of 75 bps benchmark rate cuts by Bank Indonesia and government stimulus measures such as the Wage Subsidy Assistance (BSU), which may spur data consumption. Strategically, TLKM plans to spin off >50% of its fiber assets to Infranexia in 4Q25, which we view positively for utilization improvement and long-term value creation.

We downgrade TLKM from BUY to HOLD following the achievement of our previous TP of IDR2,950, which implies an EV/EBITDA of 4.55×/4.33× for FY25F/FY26F. The main risk remains weak consumer purchasing power, which limits data traffic monetization potential despite ongoing efforts to boost margins through starter pack price adjustments and product simplification—the full impact of which may only be seen toward year-end. Upside risks: (1) faster monetization of fiber assets; (2) stronger-than-expected recovery in purchasing power driving better data traffic growth and yields.

By PHINTRACO SEKURITAS | Research

–Disclaimer On–