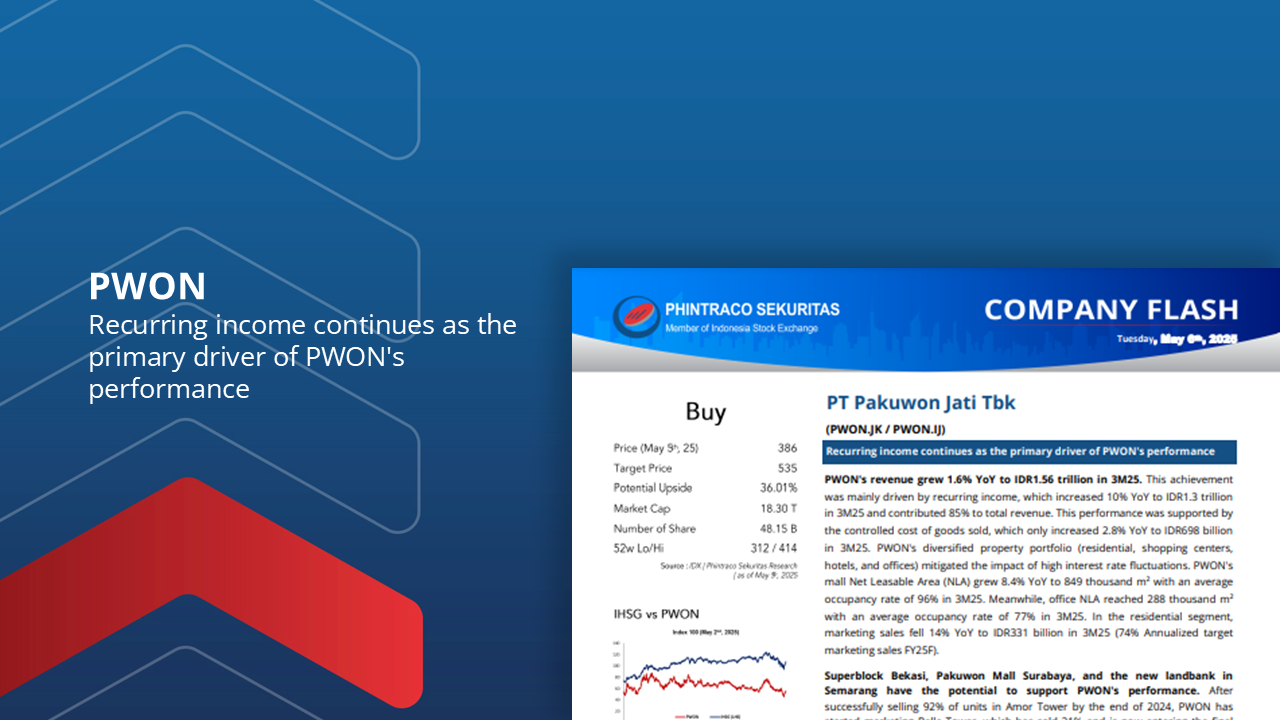

“PWON: Recurring income continues as the primary driver of PWON’s performance”

PWON’s revenue grew 1.6% YoY to IDR1.56 trillion in 3M25. This achievement was mainly driven by recurring income, which increased 10% YoY to IDR1.3 trillion in 3M25 and contributed 85% to total revenue.

PWON’s diversified property portfolio (residential, shopping centers, hotels, and offices) mitigated the impact of high interest rate fluctuations.

PWON’s mall Net Leasable Area (NLA) grew 8.4% YoY to 849 thousand m² with an average occupancy rate of 96% in 3M25. Meanwhile, office NLA reached 288 thousand m² with an average occupancy rate of 77% in 3M25.

Superblock Bekasi, Pakuwon Mall Surabaya, and the new landbank in Semarang have the potential to support PWON’s performance.

With the support of VAT incentives that will continue until the end of 2025 and solid progress from projects, PWON targets marketing sales of IDR1.8 trillion (+15.8% YoY) in FY25F.

We maintain our Buy rating for PWON with the same projection and fair value as in PWON’s previous company update, which is 535 with an upside potential of 36.01%.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –