“MYOR: Profitability Maintained Amid Production Cost Pressures”

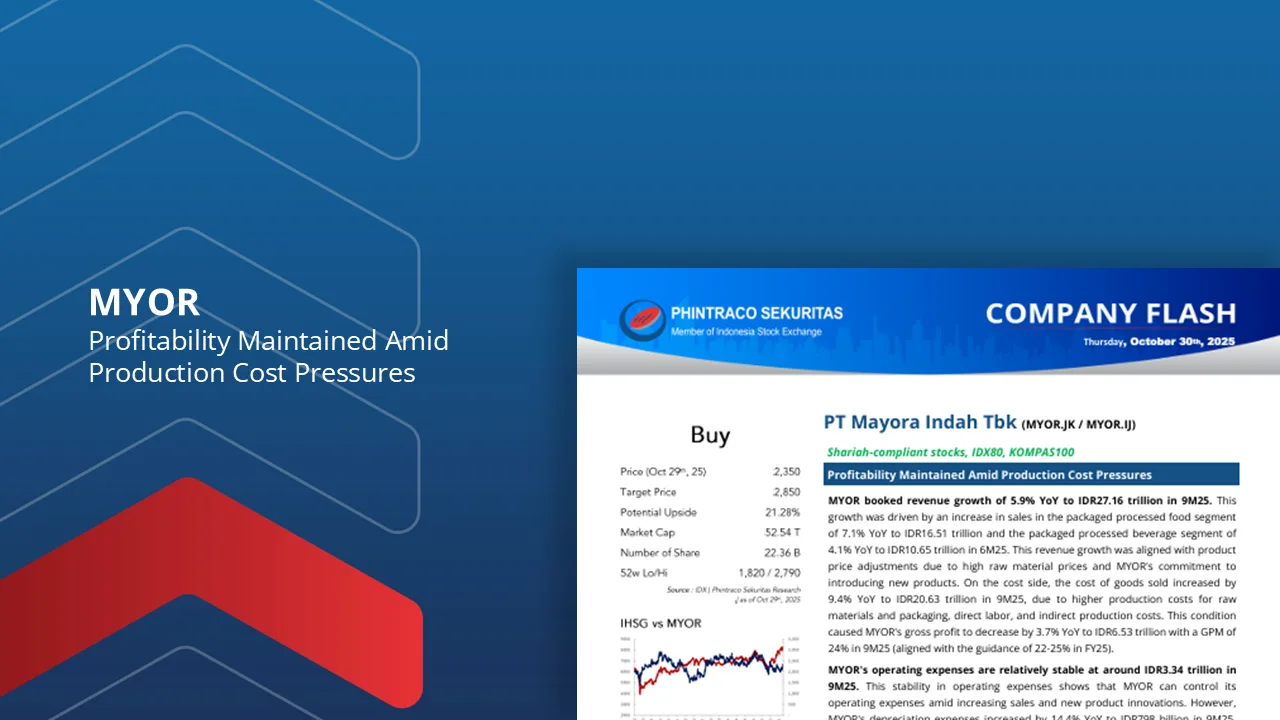

MYOR booked revenue growth of 5.9% YoY to IDR27.16 trillion in 9M25. This growth was driven by an increase in sales in the packaged processed food segment of 7.1% YoY to IDR16.51 trillion and the packaged processed beverage segment of 4.1% YoY to IDR10.65 trillion in 6M25.

On the cost side, the cost of goods sold increased by 9.4% YoY to IDR20.63 trillion in 9M25, due to higher production costs for raw materials and packaging, direct labor, and indirect production costs. This condition caused MYOR’s gross profit to decrease by 3.7% YoY to IDR6.53 trillion with a GPM of 24% in 9M25 (aligned with the guidance of 22-25% in FY25).

MYOR’s operating expenses are relatively stable at around IDR3.34 trillion in 9M25. This stability in operating expenses shows that MYOR can control its operating expenses amid increasing sales and new product innovations.

MYOR’s net profit decreased by 8.6% YoY to IDR1.88 trillion in 9M25. This decrease was relatively low compared to the decrease in operating profit, aligned with better non-operating performance, mainly due to higher foreign exchange gains and other income.

We maintain our Buy rating for MYOR with the same projections and fair value as in our previous company update at IDR2,850/share.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –