“ISAT: Gradual Recovery with Strengthening Revenue Quality”

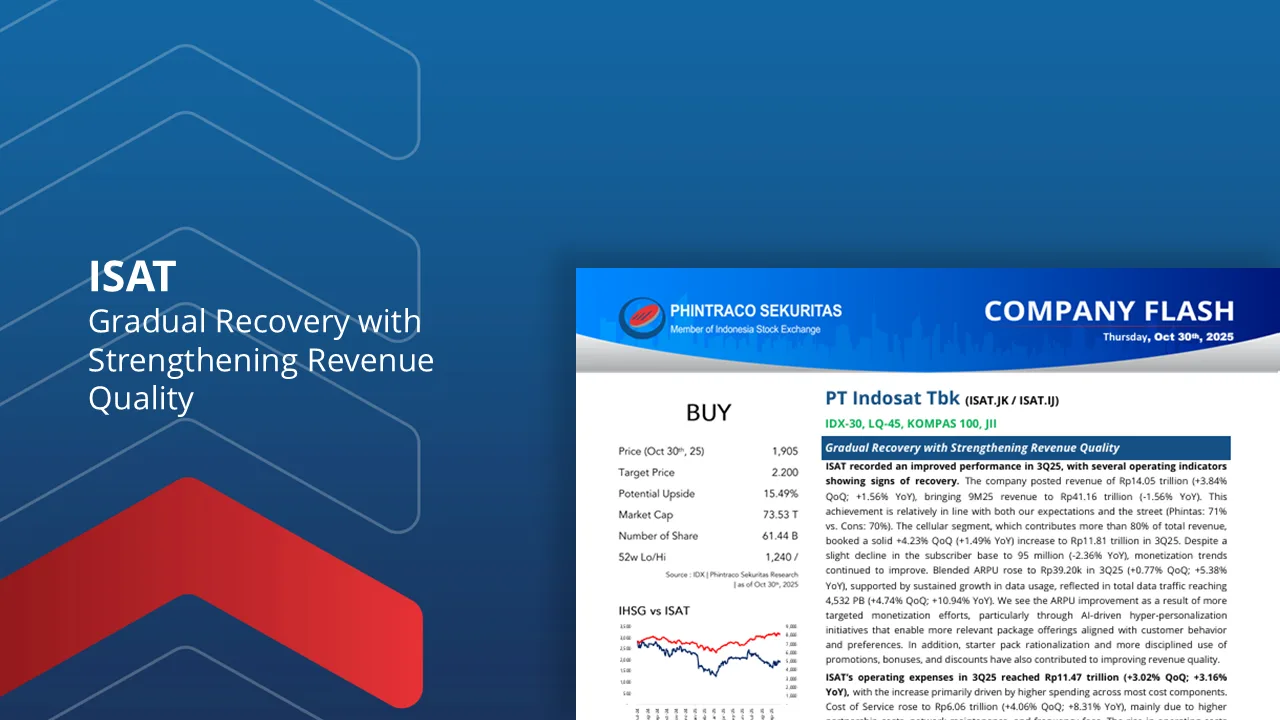

ISAT delivered an improving set of results in 3Q25, with early signs of recovery reflected in key operating trends. Revenue reached Rp14.05tn (+3.84% QoQ; +1.56% YoY), bringing 9M25 revenue to Rp41.16tn (-1.56% YoY), broadly in line with expectations (Phintas: 71%; Cons: 70%). The cellular segment, contributing >80% of revenue, rose to Rp11.81tn (+4.23% QoQ; +1.49% YoY), supported by sustained monetization despite a softer subscriber base of 95mn (-2.36% YoY). Blended ARPU improved to Rp39.2k (+0.77% QoQ; +5.38% YoY), underpinned by AI-driven hyper-personalization, growing data traffic (+4.74% QoQ; +10.94% YoY), and more disciplined starter pack and promo rationalization, which collectively strengthened revenue quality.

OPEX increased to Rp11.47tn (+3.02% QoQ; +3.16% YoY), led by higher Cost of Service at Rp6.06tn (+4.06% QoQ; +8.31% YoY), mainly from partnership fees, network maintenance, and frequency expenses — reflecting ISAT’s strategy to enhance network capacity and quality. Network expansion remained aggressive, with total BTS reaching 266k sites (+7.66% YTD), driven by 4G BTS growth of +7.81% YTD and a strong rollout of 5G BTS (+1,212% YTD). Despite cost pressures, ISAT recorded a stronger bottom line with net profit rising to Rp1.25tn (+22.25% QoQ; +9.50% YoY), lifting NPM to 18.36% (vs. 17.71% in 2Q25).

Strategic initiatives continue to show progress, particularly around technology transformation and early AI monetization. ISAT has begun operating IOH GB200 servers, which are fully contracted, signaling initial monetization traction and offering a runway for AI-driven revenue opportunities. Growth also remained intact in the Home Broadband (HBB) segment, with subscribers increasing to 369k (+4.90% QoQ). With Indonesia’s fixed broadband penetration still low, expansion potential remains wide. Fixed-Mobile Convergence (FMC) will be a key execution priority, as a more integrated ecosystem is expected to strengthen customer stickiness and household-level monetization through deeper bundling penetration.

Looking ahead, we see ISAT’s earnings trajectory supported by improving revenue quality, AI-enabled monetization levers, and HBB-FMC growth opportunities, although cost discipline remains essential to balance network expansion and profitability. While recovery remains gradual, the improving ARPU trend, scalable AI initiatives, and ecosystem-driven strategy provide structural support for medium-term momentum.

We maintain our BUY call on ISAT with a TP of Rp2,200 (see our previous report), as performance remains broadly in line with our expectations. Our positive stance is supported by improving monetization, on-track AI initiatives, and the HBB/FMC growth runway. Downside risks include: (1) slower-than-expected convergence monetization, and (2) higher-than-anticipated capex requirements.

By PHINTRACO SEKURITAS | Research

— Disclaimer On —

Contact Us:

WA: 08119055611

IG: phintracosekuritasofficial

YT: Phintraco Sekuritas Official

TELE: phintasprofits

www.phintracosekuritas.com

www.profits.co.id