“ERAA: Solid Performance Potential Towards the End of the Year”

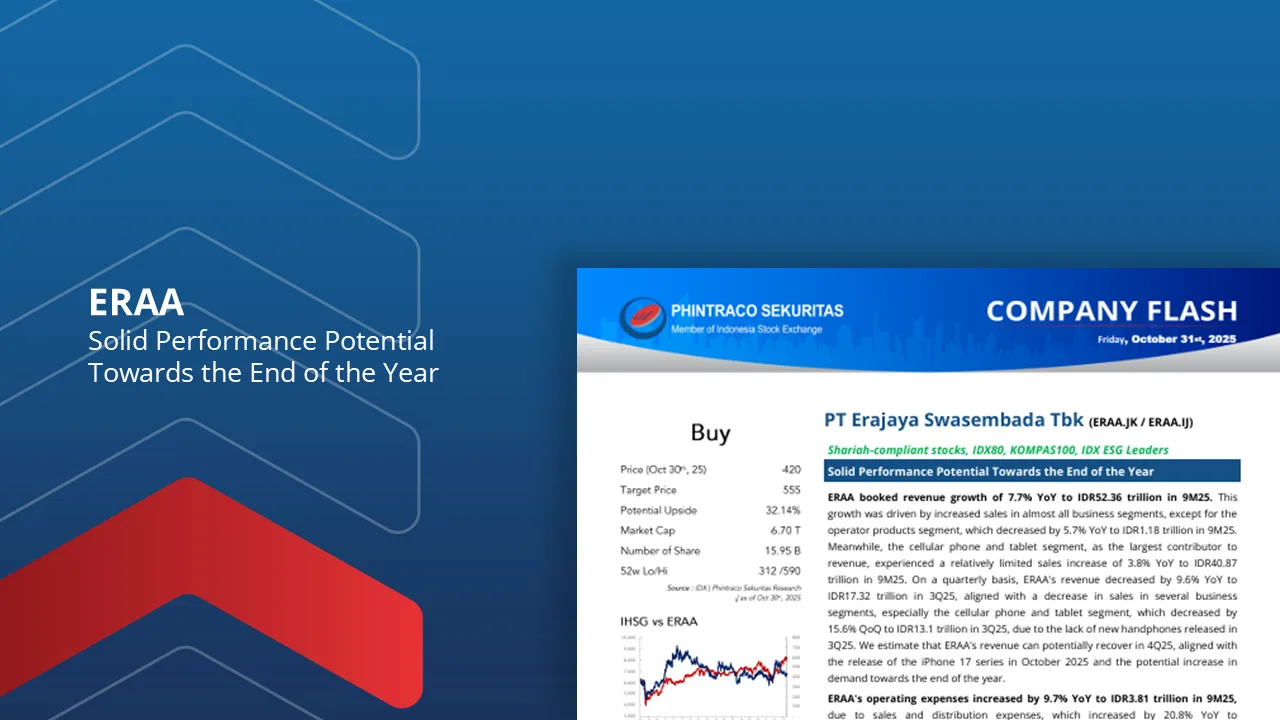

ERAA booked revenue growth of 7.7% YoY to IDR52.36 trillion in 9M25. This growth was driven by increased sales in almost all business segments, except for the operator products segment, which decreased by 5.7% YoY to IDR1.18 trillion in 9M25.

We estimate that ERAA’s revenue can potentially recover in 4Q25, aligned with the release of the iPhone 17 series in October 2025 and the potential increase in demand towards the end of the year.

ERAA’s operating expenses increased by 9.7% YoY to IDR3.81 trillion in 9M25, due to sales and distribution expenses, which increased by 20.8% YoY to IDR2.65 trillion in 9M25, mainly due to higher advertising and promotion costs and other expenses.

ERAA’s net profit decreased slightly by 0.5% YoY to IDR849 billion in 9M25. This decrease was relatively lower than the decrease in operating profit. ERAA’s net profit is still in line with our estimates (69% of FY25F).

We maintain our Buy rating for ERAA with the same projections and fair value in the initiate report at Rp555/share.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –