“CTRA: Solid performance in 6M25, maintain buy rating for CTRA”

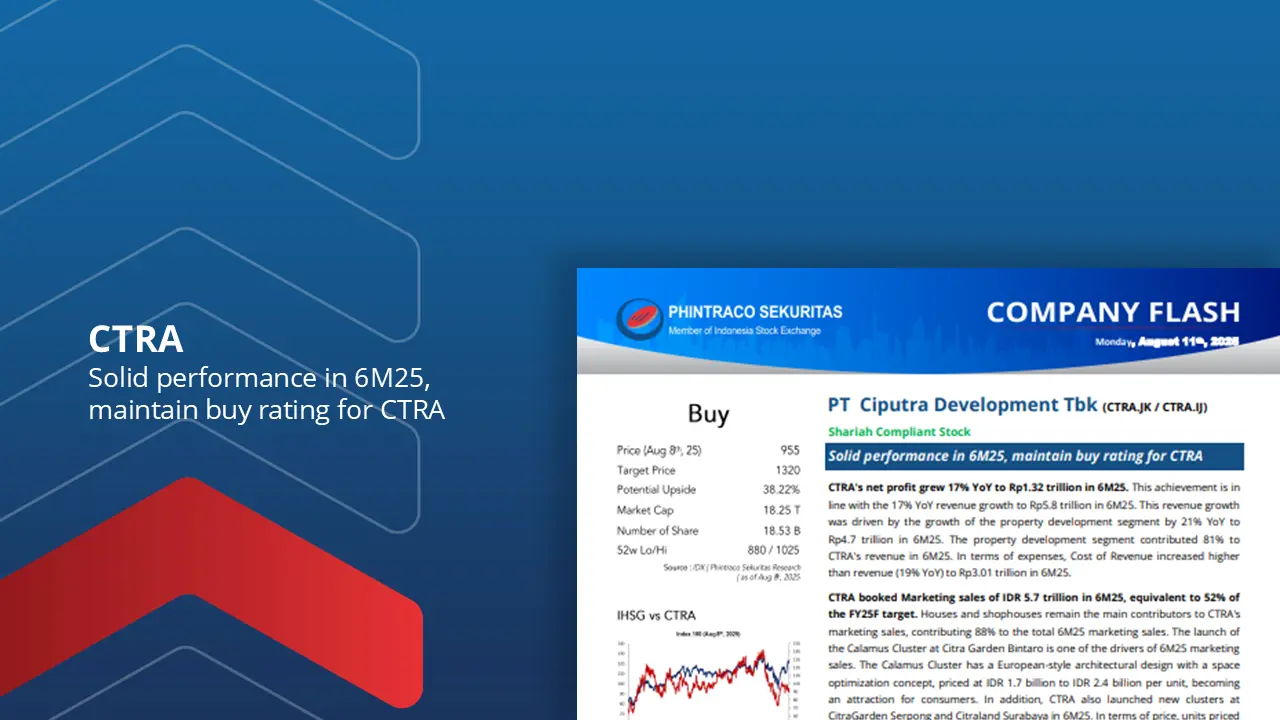

CTRA’s net profit grew 17% YoY to Rp1.32 trillion in 6M25. This achievement is in line with the 17% YoY revenue growth to Rp5.8 trillion in 6M25. The property development segment contributed 81% to CTRA’s revenue in 6M25.

CTRA booked Marketing sales of IDR 5.7 trillion in 6M25, equivalent to 52% of the FY25F target. Houses and shophouses remain the main contributors to CTRA’s marketing sales, contributing 88% to the total 6M25 marketing sales.

In terms of price, units priced at IDR 2 billion to IDR 5 billion dominated 6M25 marketing sales, contributing 45% to the total. Meanwhile, VAT incentive contributed 33% to total 6M25 marketing sales.

Therefore, with CTRA’s achievements in 6M25, coupled with the BI rate cut and the extension of the DTP VAT incentive and Loan-to-Value (LTV) discount, we estimate CTRA can post profit growth of around 8% for FY25F.

We maintain our buy rating for CTRA with the same fair value as in CTRA’s previous company update of Rp1,320 (+38.22%).

By PHINTRACO SEKURITAS | Research

– Disclaimer On –