“BRIS: Profit Growth Moderates, But Supported by Robust Gold Business”

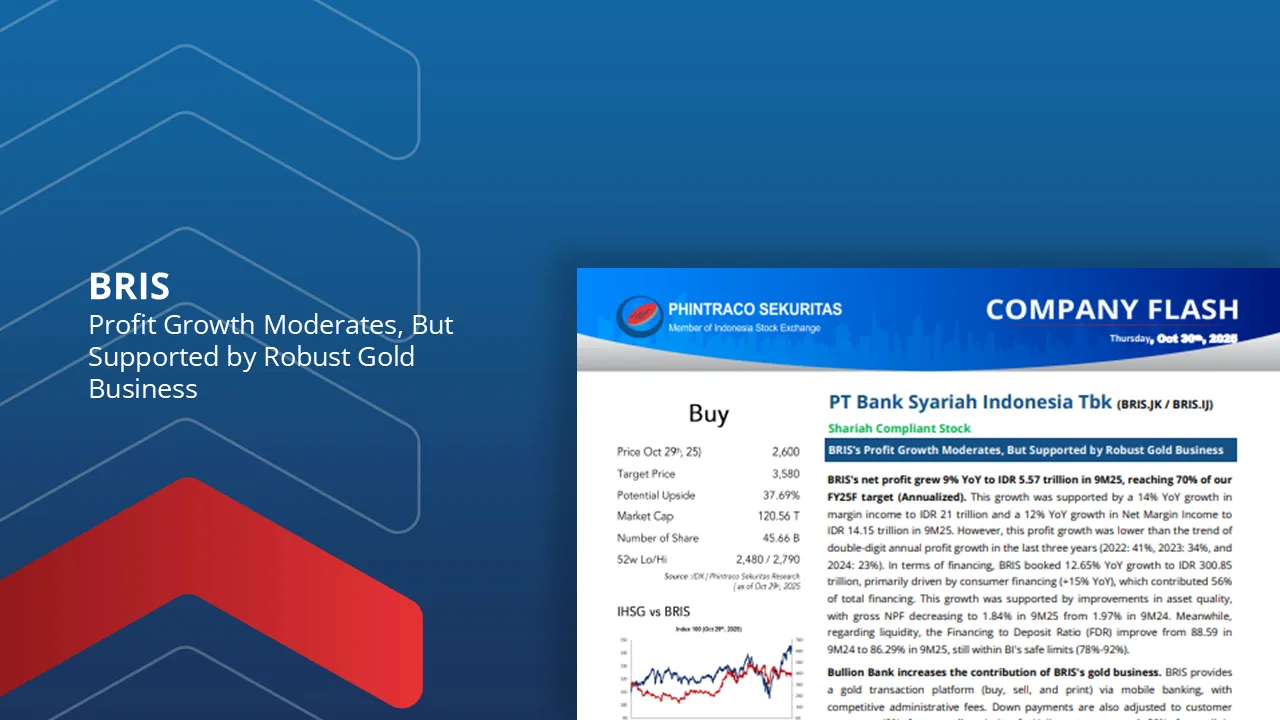

BRIS’s net profit grew 9% YoY to IDR 5.57 trillion in 9M25, reaching 70% of our FY25F target (Annualized). This growth was supported by a 14% YoY growth in margin income to IDR 21 trillion and a 12% YoY growth in Net Margin Income to IDR 14.15 trillion in 9M25.

In terms of financing, BRIS booked 12.65% YoY growth to IDR 300.85 trillion, primarily driven by consumer financing (+15% YoY), which contributed 56% of total financing.

This growth was supported by improvements in asset quality, with gross NPF decreasing to 1.84% in 9M25 from 1.97% in 9M24.

Bullion Bank increases the contribution of BRIS’s gold business. Where BRIS’s gold business was able to book significant growth, the number of customers increased by 824 thousand, and revenue from the gold business grew 73% YoY to IDR 18.8 trillion in 9M25.

With BRIS’s performance in line with our expectations, we maintain our Buy rating for BRIS with the same projections and fair value as in the previous BRIS company update, namely IDR 3,580/share.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –