“BNGA: BNGA Maintains Healthy Asset Quality Amid Modest Profit Growth”

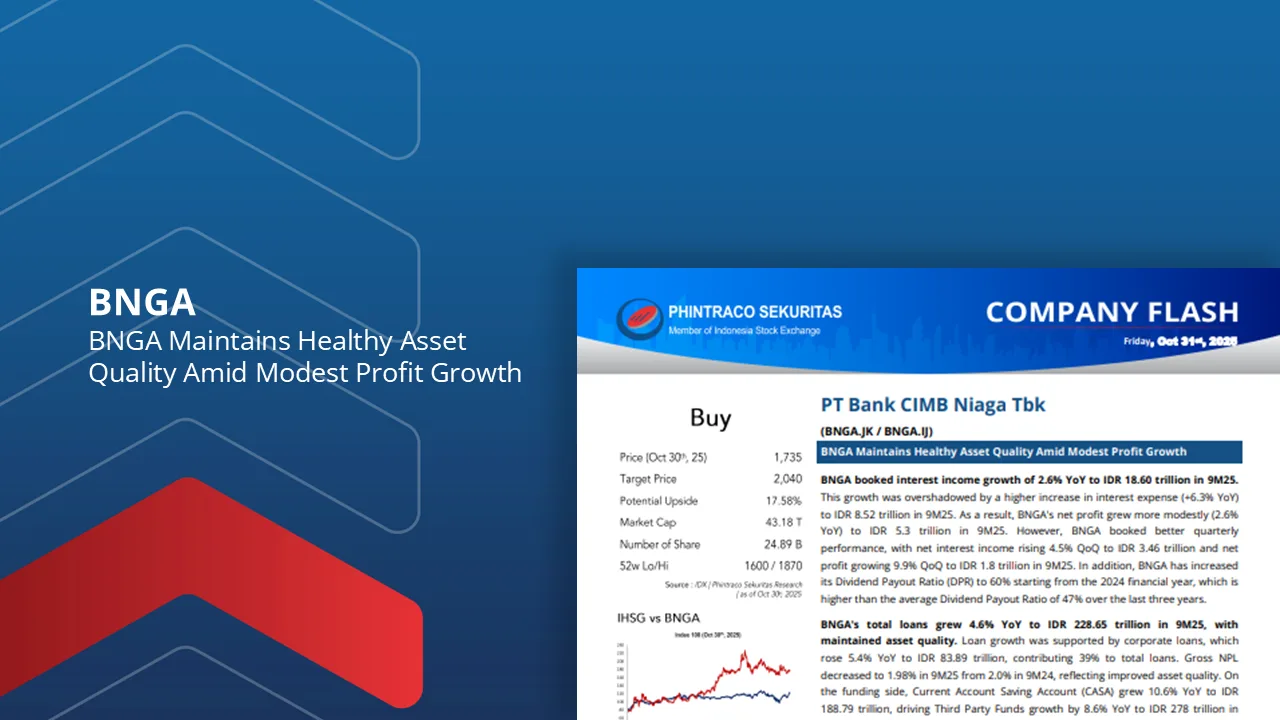

BNGA booked interest income growth of 2.6% YoY to IDR 18.60 trillion in 9M25. This growth was overshadowed by a higher increase in interest expense (+6.3% YoY) to IDR 8.52 trillion in 9M25.

BNGA booked better quarterly performance, with net interest income rising 4.5% QoQ to IDR 3.46 trillion and net profit growing 9.9% QoQ to IDR 1.8 trillion in 3Q25.

BNGA has increased its Dividend Payout Ratio (DPR) to 60% starting from the 2024 financial year, which is higher than the average Dividend Payout Ratio of 47% over the last three years.

BNGA aims to optimize retail loan growth by focusing on larger revenue streams. This effort is being taken to offset the impact of slower macroeconomic conditions.

Therefore, we maintain our Buy rating for BNGA, projected at the same fair value as in the previous BNGA company update, at IDR 2,040/share.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –