“BDMN : Net Profit Growth Driven by Asset Quality”

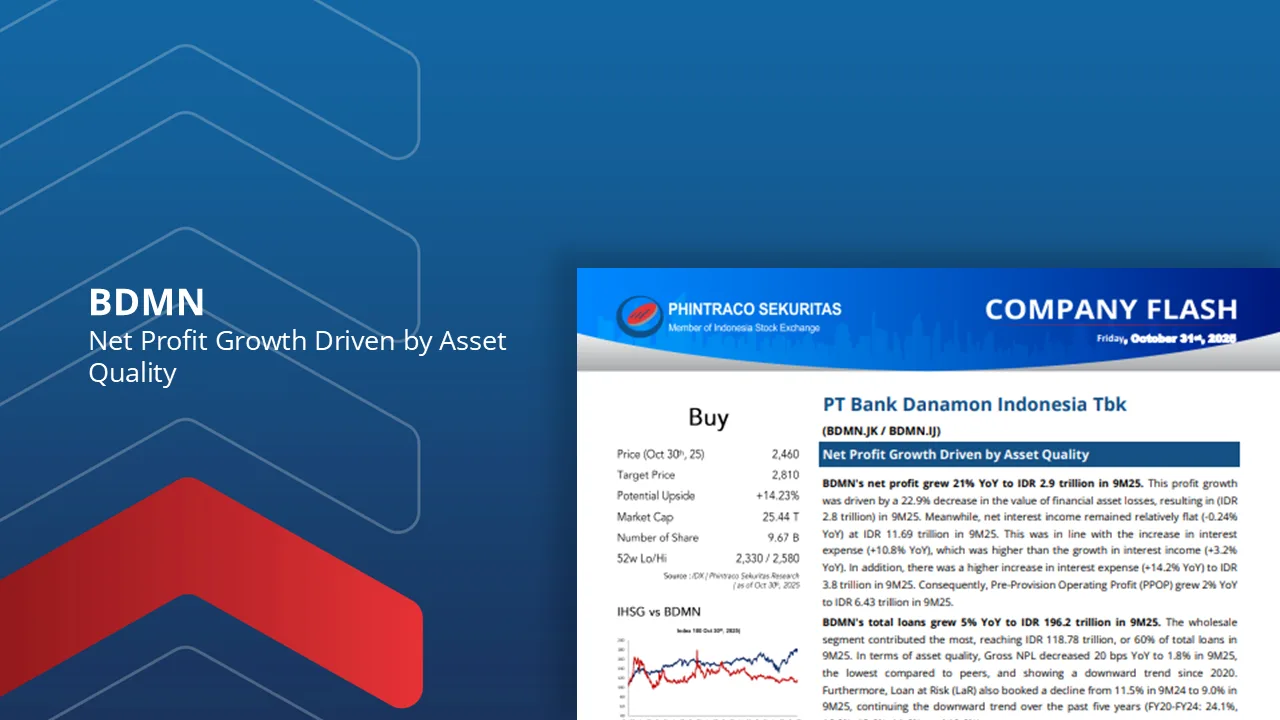

BDMN’s net profit grew 21% YoY to IDR 2.9 trillion in 9M25. This profit growth was driven by a 22.9% decrease in the value of financial asset losses, resulting in (IDR 2.8 trillion) in 9M25.

Meanwhile, net interest income remained relatively flat (-0.24% YoY) at IDR 11.69 trillion in 9M25. This was in line with the increase in interest expense (+10.8% YoY), which was higher than the growth in interest income (+3.2% YoY).

BDMN’s total loans grew 5% YoY to IDR 196.2 trillion in 9M25. The wholesale segment contributed the most, reaching IDR 118.78 trillion, or 60% of total loans in 9M25.

Interest income is estimated to grow by around 11% YoY to IDR 3.7 trillion in FY25F. BDMN remains focused on its integration strategy as a financial group. Auto retail financing (synergy loans with ADMF) grew 57% YoY to IDR 1.5 trillion.

Therefore, we maintain our Buy rating for BDMN with the same projection and fair value as in the previous BDMN company update, IDR 2,810/share.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –