“BBCA: Maintains Profitability Amid Rising Provision Expenses”

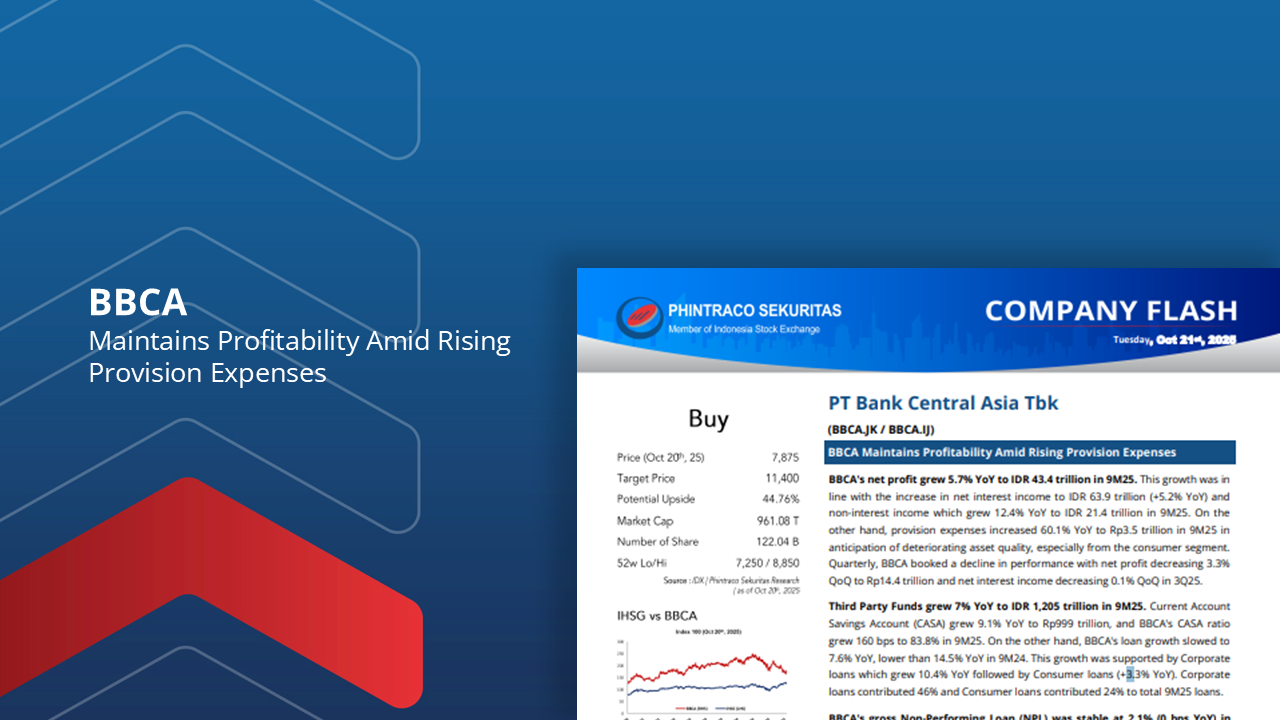

BBCA’s net profit grew 5.7% YoY to IDR 43.4 trillion in 9M25. This growth was in line with the increase in net interest income to IDR 63.9 trillion (+5.2% YoY) and non-interest income which grew 12.4% YoY to IDR 21.4 trillion in 9M25.

Quarterly, BBCA booked a decline in performance with net profit decreasing 3.3% QoQ to Rp14.4 trillion and net interest income decreasing 0.1% QoQ in 3Q25.

Third Party Funds grew 7% YoY to IDR 1,205 trillion in 9M25. Current Account Savings Account (CASA) grew 9.1% YoY to Rp999 trillion, and BBCA’s CASA ratio grew 160 bps to 83.8% in 9M25.

With BBCA’s relatively solid performance and strong customer relationships, we estimate BBCA can record revenue growth of around 10% YoY and net profit growth of 5% YoY to Rp57.5 trillion in 2025E.

Therefore, with BBCA’s current share price and performance, we maintain our Buy rating for BBCA with a fair value from the previous Company Update of Rp11,400 with a potential upside of 44.76%.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –