“CPIN : Feed and DOC Segments Maintain Revenue in 6M25”

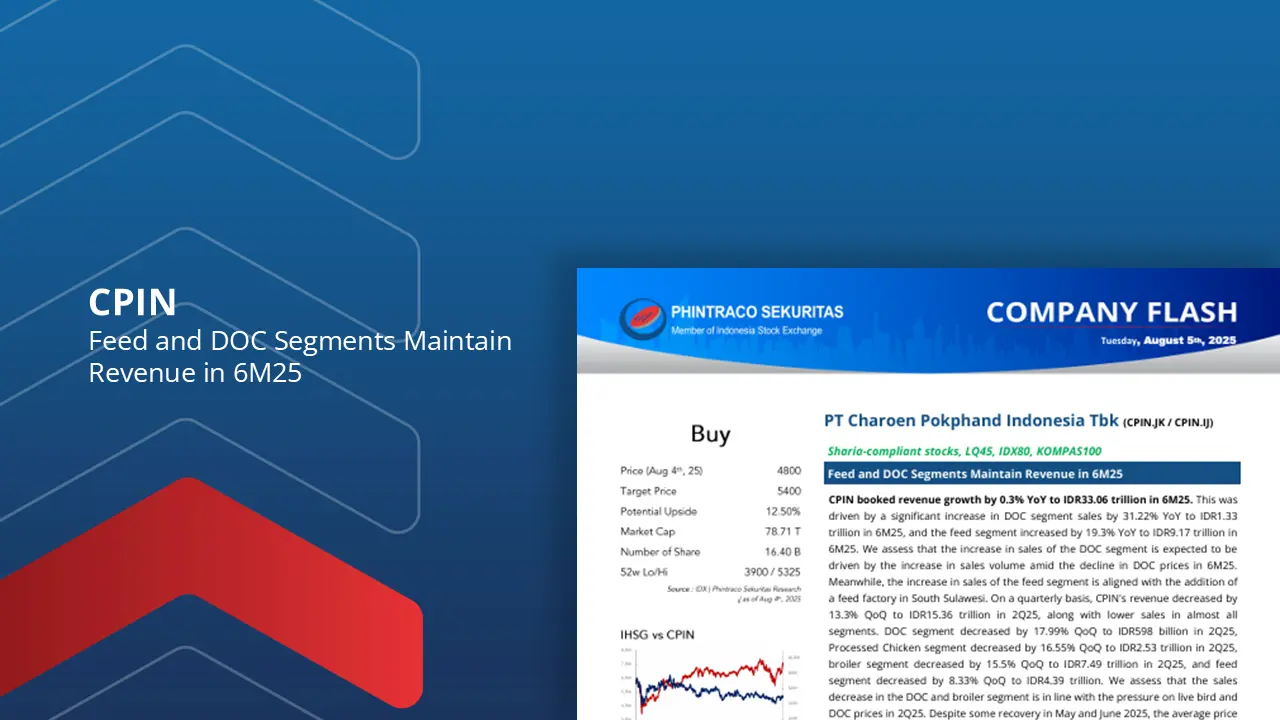

CPIN booked revenue growth by 0.3% YoY to IDR33.06 trillion in 6M25. This was driven by a significant increase in DOC segment sales by 31.22% YoY to IDR1.33 trillion in 6M25, and the feed segment increased by 19.3% YoY to IDR9.17 trillion in 6M25. On a quarterly basis, CPIN’s revenue decreased by 13.3% QoQ to IDR15.36 trillion in 2Q25, along with lower sales in almost all segments.

CPIN booked operating expenses of IDR1.96 trillion in 6M25. The expenses were stable compared to IDR1.95 trillion in 6M25. However, CPIN’s operating profit decreased by 8.3% YoY to IDR2.67 trillion in 6M25. This decrease was aligned with limited revenue growth.

CPIN’s net profit grew 7.7% YoY to IDR1.9 trillion in 6M25. This growth was driven by higher financial income from current account and deposit services and lower financial expenses, along with lower short-term bank debt. In addition, lower income tax expense also contributed to net profit growth in 6M25.

We maintain our Buy rating for CPIN with the same projection and fair value as CPIN’s previous company update at IDR5,400 per share, with a potential upside of 12.50%. This is in line with CPIN’s performance realization, which is still in line with our FY25F projection. In addition, the ongoing Free Nutritious Meal program in phases has the potential to drive demand in the medium-long term. Meanwhile, the continued recovery of live bird and DOC prices going forward is expected to improve revenue.

By PHINTRACO SEKURITAS | Research

– Disclaimer On –