AALI : Strong Revenue Momentum, Profitability Remains Capped

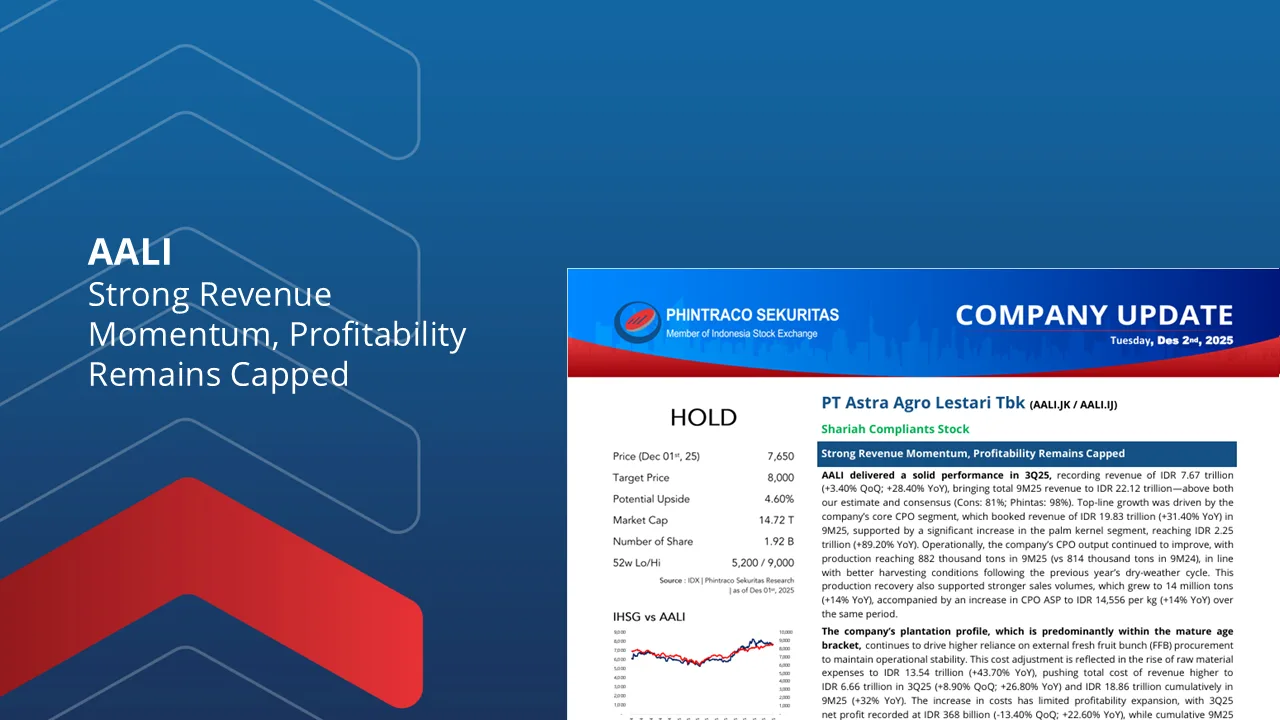

AALI posted a solid 3Q25 performance with revenue of IDR 7.67tn (+3.4% QoQ; +28.4% YoY), bringing 9M25 revenue to IDR 22.12tn, above both our estimate and consensus. Growth was supported by stronger CPO (+31.4% YoY) and palm kernel (+89.2% YoY) revenues, alongside improving CPO output (882k tons) and higher sales volume (+14% YoY) and ASP (+14% YoY).

However, the mature plantation profile continues to drive higher external FFB sourcing, pushing raw material costs to IDR 13.54tn (+43.7% YoY) and total cost of revenue to IDR 18.86tn (+32% YoY). Net profit reached IDR 368bn in 3Q25 (-13.4% QoQ) and IDR 1.07tn in 9M25 (+33.6% YoY), broadly in line with consensus, with NPM slightly softer at 4.84%.

While operational results were more resilient than initially expected—supported by firmer global CPO prices (avg MYR 4,294/MT)—margin expansion remains constrained by elevated raw material costs. We revise FY26F/27F revenue to IDR 29.03tn/30.88tn and net profit to IDR 1.43tn/1.50tn.

We downgrade our recommendation from BUY to HOLD, while raising our target price to IDR 8,000 (Prev: IDR 7,000) as we roll forward our valuation to FY26F. The higher target price reflects adjustments to revenue and earnings assumptions; however, limited visibility on margin expansion—driven by structurally higher raw material costs—restricts the potential for a meaningful re-rating.

Upside risks include: (1) CPO prices outperforming our base-case projections, (2) faster-than-expected normalization of raw material costs in line with estate productivity improvements, and (3) production outturn exceeding our FY26F baseline assumptions.

By PHINTRACO SEKURITAS | Research

— Disclaimer On —

Contact Us:

WA: 08119055611

IG: phintracosekuritasofficial

YT: Phintraco Sekuritas Official

TELE: phintasprofits

www.phintracosekuritas.com

www.profits.co.id