“MTEL : Margins Steady, Fiber Growth Offsets Tower Pressure “

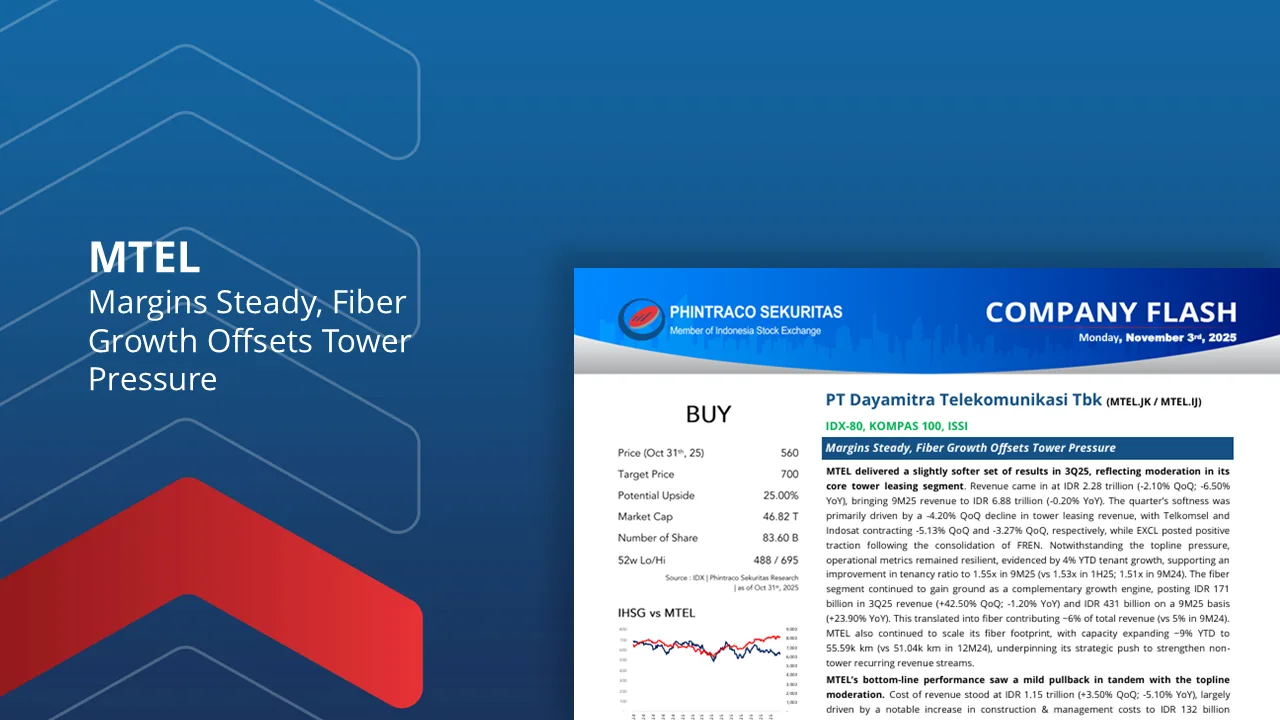

MTEL delivered a slightly softer set of results in 3Q25, reflecting moderation in its core tower leasing segment. Revenue reached IDR2.28tn (-2.10% QoQ; -6.50% YoY), bringing 9M25 revenue to IDR6.88tn (-0.20% YoY), broadly in line with expectations. The softness primarily stemmed from a -4.20% QoQ decline in tower leasing revenue, led by Telkomsel (-5.13% QoQ) and Indosat (-3.27% QoQ), while EXCL booked positive momentum following its consolidation of FREN. Despite topline pressure, operational metrics remained resilient with tenant growth of +4% YTD, supporting a higher tenancy ratio of 1.55x in 9M25 (vs. 1.53x in 1H25; 1.51x in 9M24). The fiber segment continued to show solid traction, posting IDR171bn in 3Q25 (+42.50% QoQ; -1.20% YoY) and IDR431bn in 9M25 (+23.90% YoY), lifting contribution to ~6% of revenue (vs. 5% in 9M24). Fiber capacity also expanded ~9% YTD to 55.59k km, strengthening MTEL’s recurring non-tower revenue base.

Costs saw an uptick, with Cost of Revenue rising to IDR1.15tn (+3.50% QoQ; -5.10% YoY), mainly driven by higher construction & management costs at IDR132bn (+45.90% QoQ; +7.60% YoY), while other cost items remained relatively stable. EBITDA came in at IDR1.91tn (-3.70% QoQ; -5.50% YoY), driving 9M25 EBITDA to IDR5.77tn (+0.90% YoY), with margins holding firm at 83.84% (vs. 82.93% in 9M24). Net profit softened to IDR447bn (-21.20% QoQ; -6.20% YoY), resulting in 9M25 net profit of IDR1.54tn (+0.10% YoY) and a stable net margin of 22.41% (vs. 22.36% in 9M24).

Strategic execution remains on track, with tenant additions progressing in line with management’s FY25F target of ~2.5k tenants, supporting structural tenancy gains. While the EXCL contribution is relatively modest (~10–12% of revenue), potential churn from ongoing site rationalization warrants close monitoring. That said, MTEL’s vast tower footprint provides flexibility for site relocation to mitigate churn. Fiber momentum also remains promising, supported by infrastructure expansion and rising service uptake. Looking ahead, site rationalization may continue to weigh on near-term growth; however, medium-term catalysts include further fiber scaling and potential incremental tenancy upside from the adoption of Fixed Wireless Access (FWA).

We reiterate our BUY call on MTEL with a TP of IDR700 (see our previous report), as performance remains broadly in line with expectations. Valuation remains attractive with MTEL trading at 7.6x EV/EBITDA, implying a ~19.2% discount to its 3-year average of 9.41x. We continue to favor MTEL for its strong asset base, resilience in operational metrics, and healthy balance sheet (DER <1x; Net Debt/EBITDA: 2.3x), which provides room for disciplined expansion through internal funding or bank financing.

Downside risks include: (1) higher-than-expected churn from EXCL–FREN rationalization, (2) slower-than-expected tenant additions, and (3) softer-than-anticipated colocation demand.

By PHINTRACO SEKURITAS | Research

— Disclaimer On —

Contact Us:

WA: 08119055611

IG: phintracosekuritasofficial

YT: Phintraco Sekuritas Official

TELE: phintasprofits

www.phintracosekuritas.com

www.profits.co.id