“CTRA: Solid performance in 9M25, maintain buy rating for CTRA”

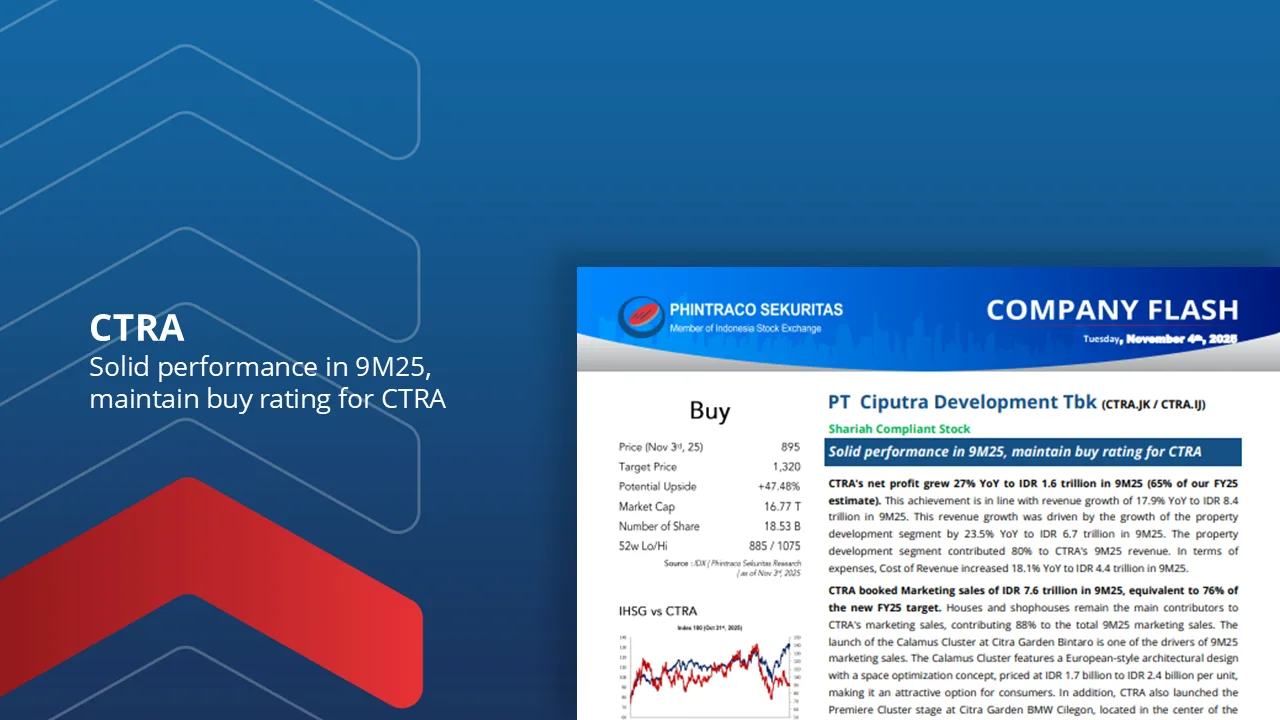

CTRA’s net profit grew 27% YoY to IDR 1.6 trillion in 9M25 (65% of our FY25 estimate). This achievement is in line with revenue growth of 17.9% YoY to IDR 8.4 trillion in 9M25.

CTRA booked Marketing sales of IDR 7.6 trillion in 9M25, equivalent to 76% of the new FY25 target. Houses and shophouses remain the main contributors to CTRA’s marketing sales, contributing 88% to the total 9M25 marketing sales.

CTRA’s geographically diversified product portfolio is a key advantage in the residential segment. As of 6M25, CTRA had 89 projects across 34 cities in Indonesia.

Therefore, with CTRA’s achievements in 9M25, coupled with the BI rate cut and the extension of the DTP VAT incentive and Loan-to-Value (LTV) discount, we estimate CTRA can post profit growth of around 8% for FY25F.

We maintain our buy rating for CTRA with the same fair value as in CTRA’s previous company update of IDR 1,320/Share (+49.15%).

By PHINTRACO SEKURITAS | Research

* Disclaimer On –